by Todd Shaver | Feb 5, 2023 | Instant News Flash

Don't Believe The "Uninspiring" Part

Retail giant Amazon ($103) suffered after reporting its fourth quarter results last week even though $150 billion in revenues came in up 9% YoY compared to $137 billion a year ago. Even so, the company only posted a profit of $300 million or $0.03 per share, a sharp decline from the $14.3 billion or $1.39 per share it posted a year ago. This was a mixed quarter, with a beat on the top line, and a huge miss on consensus estimates at the bottom.

The company’s slowest ever quarterly growth in its 25-year history, coupled with a weak guidance for the upcoming quarters led the stock down by over 8%. Amazon was faced with a broad range of headwinds during the quarter, taking a $5 billion hit to the top-line from unfavorable foreign exchange rates, followed by supply-side issues owing to persistent lockdowns in China that have since come to an end.

Amazon’s full year figures were interpreted as equally "uninspiring," with revenues at $514 billion, up 9% YoY, and a loss of $2.7 billion, or $0.27 per share, against a profit of $33 billion, or $3.24 per share during the same period last year. This was mostly the result of a $12.7 billion valuation loss from its stake in Rivian Automotive during the year, along with the excess capacity the Online Commerce side of the company acquired during the pandemic and is now winding down.

During the quarter, Amazon Web Services once again led the way when it comes to sales growth and profit contribution. Revenues from the segment stood at $21.4 billion, up 20% YoY, with a profit of $5.3 billion, flat from the year before. This, however, marked a substantial deceleration from previous years, and came in below analyst estimates of 28% YoY growth.

AWS growth has been slowing down since 2015, in the face of saturation and rising competition, but things fared worse than expected during the quarter, as most enterprises across the world have started to cut back on cloud and tech spending in the face of broader uncertainties. This trend is expected to continue this new year, as the global economy sits firmly on the precipice of a recession.

Amazon had a few bright spots in its quarterly results that still anchor its broader, long-term growth story. This mainly pertains to its burgeoning advertising business which posted 19% growth YoY, while Google’s and Meta’s platforms struggle with a slowdown. This relatively new service already makes up 7% of the global digital advertising market, with a long multibillion-dollar runway ahead.

The stock has witnessed a pullback of almost 50% since its peak of $185 in November 2021, and trades at a perfectly reasonable two times sales. The company is yet to deliver value in the form of repurchases or dividends, but this will change as the economy continues to grow and its high margin services business continues to flourish. With nearly $60 billion in cash, $165 billion in debt, and $40 billion in cash flow, this company is a force to reckon with.

Our Target is $205 and we would never sell the stock. Amazon has continued to deliver exceptional value to consumers across many fronts, with its Prime streaming service continuing to gain traction, plus new partnerships commenced with HBO and Discovery during the quarter. Yes, the company had a rough time last year, but the company is a leader in retail and groceries, as well as the Cloud, and they continue to launch newer, high margin businesses such as healthcare, financial services, and supply-chain management, among others. Management will do everything in its power to remain at the top of its game and thrive in the future of world commerce. We believe in this company.

by Todd Shaver | May 13, 2022 | Aggressive Portfolio, Research Report

Asana (ASAN: $24)

Coverage initiated May 13, 2022 at $24 in the Aggressive portfolio

Note: Current Target and Sell Prices are displayed in the Portfolio. Type the TICKER SYMBOL or COMPANY NAME into the search box (top of page) for all Bull Market Report coverage of any given stock.

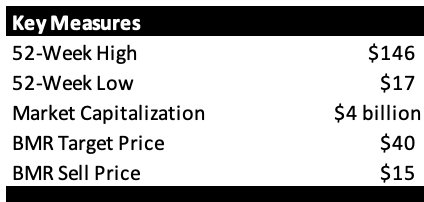

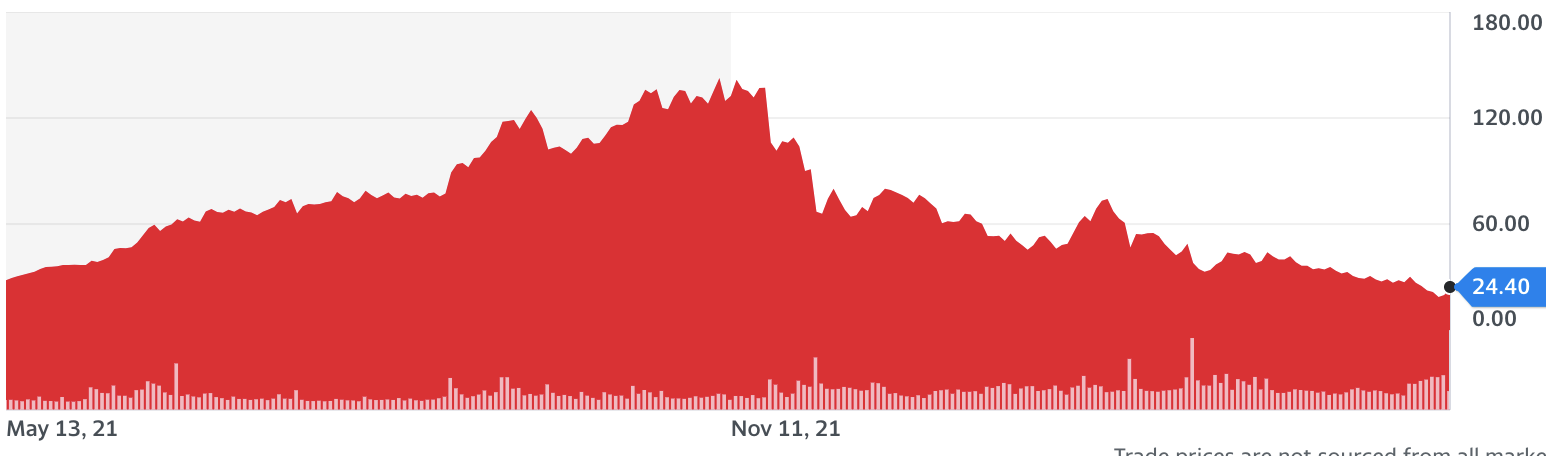

Asana is becoming increasingly popular as an enterprise-level work collaboration solution. The company's platform enables teams to orchestrate daily tasks and strategic initiatives, and manages product launches, marketing campaigns, and organization-wide goal settings. The stock has had a rough couple of months, dropping 85% from its peak of $146 in November. It is trading at its IPO price of $21 during its direct listing in late 2020 and as you know, investors have fallen out of love with fairy tale tech growth stocks that so far haven’t turned a profit. And note that Asana is not planning on being profitable this year.

Over the course of its six quarters as a publicly traded company, Asana has consistently delivered impressive growth rates and operational metrics, producing YoY revenue growth in excess of 50% each quarter. While the company still loses money, its losses as a percentage of revenue continue to decline, from 125% of revenue in 3Q21, to 35% in its most recent quarter. Their next earnings date is June 2.

We expect the company to be turning corners in 2023, driven by strong revenue growth and improving profitability margins, coupled with substantial insider buying in recent weeks. Given the increasingly distributed nature of work at organizations across the world, Asana helps provide a semblance of normalcy, which explains its growing popularity in the workplace.

Business Overview

Founded in 2008 by Mark Zuckerberg’s famed Harvard roommate and Facebook co-founder Dustin Moskovitz, Asana is an SaaS* tool for workplace collaboration, communication, and project management. Even though it was hardly a groundbreaking innovation at the time, Asana quickly gained traction among small teams, freelancers and startups owing to its intuitive interface.

*Software as a Service

Asana’s core premise was that an average knowledge worker spends nearly 60% their time “on work about work”; that is planning for meetings, communicating about work, and dealing with context switching*, without actually accomplishing any meaningful work. The platform enhances productivity by integrating all aspects of work and communications at one place.

*the tendency to shift from one unrelated task to another

Over the years, Asana has packed its platform with powerful features such as forms, workflow builders, the Work Graph data model, and approval systems, along with a robust admin system, APIs, and third-party integrations, effectively making its way from a niche tool for small teams and startups to an enterprise workflow solution used by Fortune 500 companies. What started off as a simple project and task management solution, is now a full-fledged solution to orchestrate work across an enterprise. With a relentless focus on optimizing workflows, reducing friction and boosting productivity, the company is employing machine learning, along with the Graph Workspace that allows searches, filters, and algorithms to help organizations unlock value in their processes.

Asana has successfully executed the “land and expand” business model, with its freemium pricing helping sign up 35 million registered users, out of which 2 million have been converted into paying customers. Not only does this large user base provide the company with crucial data on challenges faced by teams and organizations, it also represents significant untapped monetization capabilities.

The company has witnessed stratospheric growth over the past two years, driven by strong structural tailwinds arising from the pandemic and the resulting shift towards hybrid and remote work. At the time of its listing in 2020, the company had just 82,000 paying customers; now that figure stands at 114,000, including marquee logos such as Vodafone, Google, NASA and Uber.

Over 83% of customers surveyed in recent months agree that Asana improves job performance, with 77% agreeing that it saves time. The overall dollar-based net retention rate stands at 120% in its latest quarter, with the retention rates for customers with annual spends exceeding $5,000 and $50,000 at 130% and 145%, respectively, which speaks volumes on the platform’s value proposition.

Asana’s platform and products have received a series of honors and recognitions over the past few months, being named a leader in the IDC Marketscape Worldwide Collaboration and Community Applications vendor assessment. It was also recognized by Fast Magazine’s list of Brands That Matter, followed by Inc. Magazine’s list of Best-Led Companies 2021.

As the company continues to build on its work management capabilities, it will increasingly become a mainstay for organizations around the world. As it ingrains itself in the digitalized workflows of organizations, the resulting network effects will propel its next round of growth, all the while keeping competitive forces at bay.

Financial Analysis

In its most recent 3Q22 earnings, the company reported another quarter of stellar revenue growth at $110 million, up 70% YoY, compared to $70 million a year ago. Despite posting a loss of $43 million, or $0.23 per share, against a loss of $38 million, or $0.34, it beat estimates across the board, with plenty of strength on other key metrics.

The total number of paying customers grew by 7,000 during the quarter, to reach a total of 114,000; the number of customers with annual spend exceeding $5,000 grew 58% YoY to 14,000; and the number of customers with annual spending exceeding $50,000 grew to 740, up by a mammoth 130% YoY. The total number of paid users on the platform reached 2 million for the first time. Asana has a sizable RPO or remaining performance obligation to the tune of $190 million, up 87% YoY, which should be realized over the next few months.

Asana witnessed significant improvements in gross margins, which stood at an impressive 90% during the quarter. The bulk of the company’s expenses arise out of research and development, followed by marketing, and general administrative expenses, amounting to a total of $160 million during the quarter. Considering the rate of revenue growth in recent quarters, the company remains on the cusp of operating profitability.

The company ended the quarter with $340 million in cash, and $250 million in debt. It projects revenues for 4Q22 at $105 million, representing YoY growth of 54%. It is projecting a loss of $52 million, or $0.28 per share. Even with the negative cash flow at $30 million during the quarter, the company has a sizable runway of cash reserves to keep it afloat, with plenty of options to raise additional funds if needed.

Competitive Analysis

A key concern among investors is the fierce competition in this space, which includes the likes of Monday, Atlassian, Trello, and even industry bellwethers such as Salesforce.

The biggest trump card on Asana’s side, however, is its massive user base, the envy of its existing competitors and newer entrants. The company is capable of tracking and maintaining heaps of user data to guide its future developments and capabilities, all the while tapping new trends and opportunities, and deploying solutions to its captive user base before competing firms can gain traction.

Asana is no longer in the project management space - it is a leader among work management platforms. Given the company’s obsession with design, user experience, and intuitive interfaces, it has a significantly lower learning curve compared to other platforms, while still offering similar levels of customization and sophistication as required.

BMR Take

Given Asana’s growing traction in this niche, and the massive addressable market, comprised of 1.2 billion knowledge workers throughout the world, expected to be worth $32 billion by 2023, this company’s growth story is just beginning. Even with the pandemic receding, there are strong secular trends pointing towards long term remote and hybrid work becoming the norm.

While there are many companies working to address this segment, Asana is clearly the winner when it comes to reach. The pecking order in the long run ultimately comes down to which company does the best in keeping up with the evolving market, and given Asana’s background of execution, we have plenty of reasons to favor it.

Asana currently trades at less than 10 times sales. It is relatively cheaper compared to competitors like Monday, trading at 12-15 times sales. These valuations are not at all expensive when you consider the extraordinary YoY growth rates experienced by these companies.

Taking all of this into consideration, Asana clearly shows a lot of promise, and given its market cap of just $3.8 billion, it has plenty of runway ahead to generate value for investors. The company’s shares are seeing plenty of activity in recent weeks, triggered by insider buying, namely the founder and CEO, Dustin Moskovitz, buying $1.1 billion worth of his company’s stock in the last year. As Peter Lynch said, “Insiders might sell their shares for any number of reasons, but they buy them for only one: they think the price will rise.” Moskovitz’s aggressive buying in recent months, and his current holding estimated at 17% of the company, means his interests are perfectly aligned with shareholders. We expect plenty of fireworks in the future of this company, and we are excited to be a part of the ride.

by Todd Shaver | May 12, 2022 | Instant News Flash

Time To Exit

Online consumer finances platform Sofi (SOFI: $5.30) released its first quarter results early this week, reporting $330 million in revenues, up 68% YoY, compared to $196 million a year ago. The company posted a loss of $110 million, or $0.14 per share, against a loss of $178 million, or $1.61.

Despite beating analyst estimates on top and bottom lines, and a raise in guidance figures for the second quarter and the full year, the stock tanked following the results. This can mainly be attributed to the accidental early release of the figures due to a human error, which caused the stock to halt trading for nearly three hours; an unpardonable offense in light of recent market conditions.

Sofi’s business and fundamentals remain as robust as ever, adding 408,000 new members during the quarter alone, up 70% on a YoY basis, bringing the total to 3.9 million, followed by 690,000 in new product, ending with nearly 5.9 million total products across its massive catalog of financial products, an increase of 84% YoY.

Apart from this, the company continues to lose money, and as we’ve seen over the course of the past few weeks, the market has lost all patience when it comes to companies that are losing money. With even profitable peers like PayPal and Upstart being obliterated due to a slowdown in growth, we expect Sofi Technologies to be a lot more fragile, especially with the steady rise in macro headwinds in recent months.

We love the company but can't fight the market mood. It truly takes results that are better than "better than perfection" to get any kind of traction on Wall Street right now. These are staggering numbers and extremely cheap at barely 2X 2023 sales targets, but mean nothing right now. It would take something monumental for Sofi to get out of this rut. Until that happens, there's no urgency in buying or even holding on.

Of course, one could make the argument of adding more at this level. But that's for investors with real conviction and an eye on the future. For now, the Sofi balance sheet looks a little stressed ($500 million in cash against $4.2 billion of debt) and it's time to look toward our own cash reserves. With this in mind, we are removing this stock from our portfolio. The company has great potential and is doing great things. The stock, sadly, is not.

by Todd Shaver | Mar 31, 2022 | Instant News Flash

The Mood Is Improving

Global payments platform PayPal (PYPL: $118) and its shareholders have endured a rough couple of months. Triggered by poor fourth quarter results in early February and persistent worries about too much competition in Electronic Payments dooming the stock in a rising rate environment, shares fell to a 52-week low a few weeks ago and are now "only" up 27% from that deeply depressed level.

While several analysts have downgraded the stock for nebulous reasons, Goldman Sachs has initiated coverage with a “Buy” rating and a $144 price target, representing an upside of 21% from here. The analyst expects PayPal to return to earnings growth in excess of 20% after 2022, fueled by substantial tailwinds in the form of eCommerce growth, digitalization and more. That's historically all this company has ever needed to keep the stock climbing at a healthy rate, year after year.

PayPal has significantly upped its game when it comes to eCommerce, especially with its acquisition of HappyReturns, a solution that allows merchants who use PayPal Checkout to seamlessly handle returns. The company has further partnered with Ulta Beauty and a number of other firms to expand its return bar locations to over 5,000, offering a critical network for online retailers, especially at a time when average return rates are in excess of 20%.

On a fundamental level, PayPal remains as sturdy as ever. What it went through in recent months is an amalgamation of various factors, mainly the post-COVID overhang, that many of its peers continue to deal with, followed by the loss of eBay payment volumes (anticipated for years) and the lack of any visible growth catalysts in the medium term as the company enters into a “transition year.”

But this is a giant company, at $140 billion of market cap. The all time high is $310 less than a year ago. It WILL get back there – it’s just a matter of time. Last four years of revenues: $15 billion in 2018, followed by $18 billion, $21 billion and then $25 billion last year. Last quarter revenues: $7 billion. And the company is quite profitable too.

The market’s narrow-minded view has resulted in a strong opportunity for value investors to pick up this beaten-down Fintech giant and ride the indomitable growth of digital payments. Trading at just under 6 times sales, the stock is oversold and undervalued. We continue to maintain our Price Target at $305, and reiterate our pledge to never sell this company.

by Todd Shaver | Mar 29, 2022 | Instant News Flash

Fed Dread Evaporates As Management Steps Up

Leading “Buy Now, Pay Later” service provider Affirm (AFRM: $44) has had a rough couple of months, with the stock down over 70% since November. The once piping hot trailblazer has lost over $35 billion in market cap, and now trades below its January 2021 IPO price of $49, despite witnessing a multifold growth in active consumers, GMVs, and revenues during this period.

While most fintech stocks have taken a hit since late 2021, Affirm’s drop is far worse even relative to this broad-based correction. This is all the more perplexing, considering the company’s recent quarterly figures, with a 77% YoY increase in revenues, a 150% increase in active customers, gross merchandise value (GMVs) up by 115%, followed by a mammoth 1,900% YoY jump in active merchants - absolutely crazy strong numbers!

Affirm has remained under pressure since mid-November, when multiple rate hikes seemed increasingly plausible in the face of sky-high inflation. With rising rates, the cost of capital would make BNPL services less profitable on a per unit basis. Management addressed this directly during the recent quarter, with the outlook already reflecting a 180 basis point rate increase.

That's right. An aggressive Fed is built into the business model. And we suspect that's part of the reason Affirm has rebounded a healthy 68% from its recent low now that the Fed has finally started stepping up. There's still ground left to recover but this is a stock that's back on the bull trail.

What else have people found to complain about? The company also faces higher risk premiums with its asset-backed security auctions, with major investors pulling out citing higher market volatility. Finally, the jury is still out when it comes to delinquencies, with data still quite sparse and further clarity only possible as loan books grow bigger and pick up a bigger share of the overall credit market.

While these are all genuine concerns, the stock's recent move to the upside demonstrates the fact behind all the dread, speculation and empty chatter: the risks have been blown out of proportion, and the market response is an overreaction. That's the real important thing anyone looking at Affirm today needs to digest. It was well known that the company would post higher losses as it scales, while collecting valuable data to optimize its offerings. Losses were further enhanced owing to an increase in credit provisioning during the quarter, at $53 million, compared to $13 million a year ago.

Investors also seem to have misconstrued the shift in Affirm’s loan mix in recent months from high-fee instant loans where revenues were paid upfront to longer-term interest-bearing loans with potential to generate higher returns. The second model incurs credit expenses upfront, while generating steady revenues over a period of time, which hasn’t been well received by the markets so far.

Given the large-scale adoption of BNPL among consumers and the substantial benefits it stands to add for merchants, we can safely say that we’ve barely scratched the surface of a potential trillion dollar market. With exclusive partnerships with Amazon and Shopify providing a strong anchor to the company, it has a significant leg-up against competitors.

In hindsight, a $50 billion valuation may have been a little ambitious, but with the stock currently trading at 11 times sales and the business growing at triple digits we believe Affirm to be undervalued. This is a perfect opportunity for investors who missed out on Affirm’s dream run last year to get in on this new, disruptive business. Our Price Target of $200 is currently too high, so we are lowering it to $95, with the Sell Price of $110 lowered to $31.