by Scott Martin | Mar 23, 2025 | Weekly Newsletter 7pm Sunday

The Bull Market Report

Probably the Best Financial Newsletter in the Country

IN THIS ISSUE

Market Summary

The Big Picture

Netflix

C3.ai

VanEck Semiconductor ETF

Zscaler

Dexcom

iShares Oil & Gas Exploration & Production ETF

Range Resources

Ally Financial

Welltower

The Bull Market High Yield Investor

- Invesco Municipal Trust

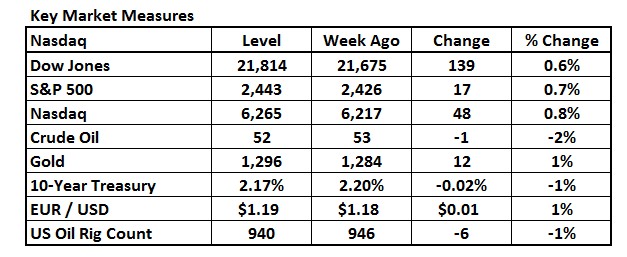

Market Summary

We'll count this as a win. While our stocks still have a little ground to recover before we wipe out the last YTD losses and start moving forward again, at least we've started moving fast in the right direction. Broad market benchmarks, on the other hand, still look more than a little stalled, with the S&P 500, Nasdaq and Dow Industrials down 2-3% from where they were two weeks ago. What's changed in the world? Not much at all. Trade policy remains unsettled, the Fed is still on hold and earnings season is effectively over until the next cycle gets underway in mid-April.

However, the recent "flash correction" (seventh-fastest in history, we're told) managed to attract buyers back to a market that felt slightly overpriced relative to the amount of uncertainty out there. A few months ago, investors seemed confident holding onto stocks valued at 22X earnings. Now, while the outlook has weakened a little, investors seem willing to accept roughly 20X as a viable entry point. If that proposition holds in the longer term, this will go down in history as a bottom and not a hard ceiling on the market's ability to keep rallying despite all apparent threats.

After all, the collective corporate bottom line is not going down. It's only going up a little less fast than we hoped a few months ago. We'll talk about this in greater detail in The Big Picture but the executive summary really boils down to the fact that all the apparent threats haven't triggered any kind of earnings recession. All they've done is curbed the most enthusiastic growth forecasts. We're in more realistic territory now. And if investors will pull cash off the sidelines and pour it into stocks with the market at 20X, then that's the world we find ourselves in.

There are at least two key lessons here for BMR subscribers. First, our approach to diversification may superficially hurt us when the bulls are running at full froth, but the minute the market mood turns sour, a little extra exposure to income-oriented stocks and funds goes a long way. These investments rarely have a lot of growth on their side. The underlying businesses are steady cash generators but management is more focused on returning cash to shareholders than pouring it back into corporate expansion initiatives. As a result, while they're rarely sexy, they have a lot of staying power. Our Healthcare portfolio is up YTD. So are most of our REITs, most of our Financials and, in a shock to some, Energy. Yes, the Energy portfolio is up 5% YTD despite all the nattering about the world economy and falling oil prices. Never forget that in a true economic upheaval, it's strategically useful to have a stake in the companies that collectively keep the world's lights on and the trucks running. (We've been loving our SPDR Gold Shares for similar strategic reasons: up 15% so far this year!)

The second lesson is that over time the most dynamic companies will outperform. They rally harder in the good phases and while they might correct almost as hard in the downswings, you just can't keep a good stock down. The rebounds are more robust than the retreats. In some cases, you can't even see the retreat. We're pleased to have names like Netflix (up 8% YTD), Meta Platforms (up 11%, beating everything else in the "Magnificent 7") and Zscaler (up 16%) to both buoy our overall results and demonstrate our expertise. From cycle to cycle, having stocks like this on our list is how we keep outperforming.

Do the allocation math. We currently cover 55 stocks and funds. Unlike top-down passive portfolios, our "BMR Index" is equally weighted to allow smaller names the same shot at the spotlight as the giants. Otherwise, small stocks like Recursion Pharmaceuticals (market cap $2 billion) would vanish in the face of a single Apple ($3.8 trillion). They'd lose all their impact. Netflix accounts for about 1.4% of our equal-weight universe so its strength this year shows up a lot more clearly than it does in index funds that track the S&P 500, for example, which weight the stock at barely half that level. Zscaler, with a relatively lofty $31 billion valuation, doesn't show up in the index fund at all. Those investors are locked out of success stories like this until the stocks have already succeeded. Even then, it takes trillions to add up to more than the percentage point or so of attention we give every single recommendation.

Granted, the last few weeks haven't been kind to a lot of these companies and the rest of our recommendations have taken a significant step back. But we've always said that while Wall Street's moods come and go, the fundamentals always assert themselves as the ultimate arbiter of shareholder value. Or as Warren Buffett's mentor Benjamin Graham once said: "In the short run, the market is a voting machine, but in the long run, it is a weighing machine." The fundamentals remain robust. As long as that situation doesn't change, the votes should ultimately swing back in our direction.

That's how we outperform, with a strong defensive line against the storms and a stronger offense when the skies clear. Let the Fed do whatever it wants. Let Washington swirl. One way or the other, we're in position to ride the wave. And this week in particular, that edge shows up in our tangible results, both recent and YTD.

There's always a bull market here at The Bull Market Report. We've spent a lot of time looking back at trailing earnings reports lately, so it's past time we opened up The Big Picture to what investors actually need to know: our take on the future and whether that projection is bright enough to justify buying (and holding) stocks at this point. Since the Fed met, you can guess what The Bull Market High Yield Investor is all about. And as always, we need to update you on stocks in our favorite sectors.

Key Market Indicators

The Big Picture: Substance Over Shock

A packed news cycle has a lot of investors on edge. We get it. But in our experience, flinching from every hypothetical shock practically ensures that you'll miss out on a lot of opportunities, even if you're not a "trader" looking to sell out ahead of periods when stocks underperform or go down. After all, most of the nightmare scenarios we can imagine simply don't come true, and the ones that happen are rarely as bad as the worst projections suggest. Unless you can't roll with a few rumors, you'll find it challenging to reach for the upside.

And we're in luck because there's one news cycle we can always anticipate and the next one starts in a few weeks when the big Banks start to release their quarterly numbers. Unlike all the speculation about trade policy or taxes, for example, earnings season is a scheduled event. We can all see it coming. Most of the bigger companies let us know weeks in advance when exactly to expect the numbers. They also provide some sense of what to expect from the numbers, which is all "guidance" really means. Of course this advance glimpse at how the cash is flowing is not official or perfectly accurate, but it's the best sense the executives running the operation have of where the trends point.

While that logic might seem intuitive and even basic on the surface, it's worth letting it sink in through all the anxious chatter currently choking the market. Guidance gives us a pretty good sense of earnings, revenue and other key metrics for the current quarter and often the full year as well. At the very least, it's as good as the numbers the executives see every day as they guide the business around short-term threats and toward long-term goals. When something emerges as a real risk factor, they'll mention that they're watching it. If they don't volunteer that information, odds are extremely good that one or more of the analysts on the conference call will raise the question.

Those risk factors are built into every company's projections. When emergent threats have a material negative impact on those projections, a smart management team will acknowledge the pain early and warn Wall Street that the corporate sky has gotten cloudy. Normally somewhere between 55 and 65 members of the S&P 500 will issue this kind of warning at this phase of the quarterly cycle. We're currently tracking 66, which is only a fraction above average. Needless to say, "average" means normal. It isn't elevated. It isn't extreme.

Don't get us wrong: those warnings have a cumulative chilling effect. Our sense of earnings growth across the S&P 500 for the full year (2025) has come down about 3 percentage points in the last two months, which is roughly when the warnings started stacking up. Revenue growth is coming on 1/2 percentage point lower. This does not suggest that either the top or bottom line for America's corporate giants is going down, only that it is rising a little less fast than we hoped. All in all, we are still looking for 11% more profit this year than last and well above 5% higher sales numbers as well. Does that look like a looming crash to you? Remember, executives play a challenging game: when they guide our expectations lower, their stocks go down in the short term, but if they don't warn us at all, the stocks drop hard when we get the results. That's when the real "shocks" that matter happen.

We don't buy the S&P 500 as a whole, so all these numbers are really only relevant when it comes to gauging the overall market's mood. So who is feeling the chill? Materials producers are hurting hard. We don't recommend them. Tesla is hurting hard, with growth forecasts dropping as sales and sentiment falter. We don't recommend them right now either. The Industrials are reeling. Not a lot of that in our portfolios. Walmart warns? We don't cover it.

What we like (and what we overweight) is growth at the right price. That means a lot of Technology, a handful of Finance and Communications companies that effectively double as Tech and a surprising amount of Healthcare. Healthcare is booming, with earnings across the sector on track to expand 18% this year, right in line with traditional Tech. Some of these stocks have rallied so hard that they've gotten ahead of their realistic growth curves, but others have the dynamism to validate their valuations.

Here's the basic barometer: the S&P 500 might give us 11% growth this year and trades at 20X forward earnings. While that's not great by historical standards, it gives you a sense of what a vanilla "stock investor" would get in an index fund right now. Across the Tech sector, that growth rate might come in around 19% and Wall Street is paying 25X for that accelerated trajectory. Again, not great calculations by historical standards (back in the E.F. Hutton era, Tech would need to drop another 25% or so to qualify as a screaming buy) but not exactly bad enough to dump existing positions and start over. We'd call it a "hold" at worst. Healthcare looks much better at 18% growth and 17X forward earnings. Yes, that is that E.F. Hutton era "screaming buy," and it's why we are so happy with so many of our Big Pharma names.

Growth isn't everything, either. We have always preferred some sectors and industries (Real Estate, high-yield Financials and lately Energy) because they satisfy different investment criteria, the main one being the ability to lock in decent current income as the dividends accrue. Energy, as you know, is a boom-and-bust cycle. Right now these stocks are far out of favor with earnings stalled this year, but management feels comfortable forecasting 17% growth next year and we find no reason to disagree. At that point, Energy will be expanding faster than Tech. Investors who buy that story now at barely 14X current earnings will feel pretty smug in that scenario. That's exactly how all of this works. Buy clarity, don't flinch until it's clear that the bad headlines are actually headed into your lane.

BMR Companies and Commentary

Netflix (NFLX: $960, up 5% last week)

LONG TERM GROWTH PORTFOLIO

Streaming giant Netflix is riding high on the blockbuster success of its new tiers, content, and initiatives, and Wall Street, too, is taking notice with a string of bullish price targets in recent weeks. The most prominent take comes from MoffettNathanson which states rather definitively that ‘Netflix has won the streaming wars, case closed’ as its content and engagement metrics are miles ahead of competitors.

The stock released its fourth quarter results recently, reporting $10.3 billion in revenue, up 16% YoY, compared to $8.8 billion a year ago. Profits came in at $1.9 billion, or $4.27 per share, doubling from $940 million, or $2.11. We believe that the streaming giant’s profits are only just beginning to scale as it begins to unlock value from its massive worldwide landed base of 300 million paid subscribers.

The platform now reaches an audience of over 700 million viewers, or a little under a tenth of the world’s population, putting it right alongside the world’s top media conglomerates. The company’s much-publicized foray into advertising and its new powerful ad suite are all aimed at unlocking the billions in untapped value that comes from having so many eyeballs on you each evening.

The company’s relentless focus on engagement and customer satisfaction is paying off and is not slowing down. There was a time when its original content was hit-or-miss, but the company has finally cracked the content game and is now on par with the big studios such as Disney and Paramount. The move into live sports has flourished similarly in recent months, driving millions of fresh sign-ups.

Since the beginning of streaming play, Netflix's goal has been to have as many people spend as much time on the platform as possible. Having attained this goal, gears are shifting toward monetization. We expect advertising to become a major contributor to profits over the following months and years, in addition to several new content and pricing tiers.

In 2024, Netflix had more shows ranked #1 in the ‘Top 10 Streaming’ charts than the other streaming platforms combined. The Jake Paul vs. Mike Tyson boxing match last year was the most-streamed sporting event in history, and with the Christmas Day NFL Game, WWE Raw Pro, and the Screen Actors Guild Awards, it is now an entertainment powerhouse. Talk about streaming—Netflix’s profits will keep flowing in, and they’re already impressive, with $1.9 billion in profit on $10.3 billion in revenue.

Our Target for Netflix is a hefty $1300, and We Would Not Sell Netflix. We believe we have one of the highest targets on The Street. We can see a 10-1 stock split in the company’s future. Wouldn’t that be nice?

C3.ai (AI: $23, up 5%)

EARLY STAGE PORTFOLIO

Enterprise AI company C3.ai released its third quarter results recently, reporting $100 million in revenue, up 26% YoY, compared to $78 million a year ago. The loss during the quarter stood at $16 million, or $0.12 per share, against $16 million, or $0.13. Still, the company had a spectacular beat on consensus estimates at the top and bottom lines, giving investors renewed confidence in its future performance.

Subscriptions led the way at $86 million, up 22% YoY, followed by professional services at $13 million, a big 62% over the prior year. This was an eventful quarter for the company, with 66 new agreements, up 72% from the preceding year, made possible by its expanding global distribution network comprising several heavy-hitters in the cloud, AI, and professional services.

C3.ai signed 28 agreements spanning 9 industries via its partnership with Microsoft alone. It is now entering into similar partnerships with Amazon’s AWS and McKinsey QuantumBlack, which is focused on spearheading digital and AI transformation across large enterprises. The company realizes that such partnerships are key for seamless reach and execution at the leading edge of enterprise AI and tech.

We saw several new and expanded agreements from well-known brands during the quarter, including Sanofi, Nucor, ExxonMobil, and Coca-Cola. C3’s federal business continues to scale with similar agreements with the Department of Defense, US Air Force, the CAE USA, and the Missile Defense Agency, alongside 21 different state and local government wins during this period.

While investors remain concerned about the company’s persistent losses, profitability is approaching. Management aims to be profitable towards the end of 2026. In the meantime, we cannot ignore that this is one of the few companies to have succeeded with productized AI for large enterprises, which is bound to accrue value.

The markets, however, have been unable to look past the losses, with CEO Tom Siebel’s health issues* also weighing on their concerns. The stock is down 35% YTD, but we believe in this beaten-down speculative stock and its underlying tech platform. It has the resources to stay afloat till it turns profitable, with $720 million in cash and just under $5 million in debt.

*Siebel has been diagnosed with an autoimmune disease that is impairing his vision. The company has made specific accommodations, and he remains in charge of the day-to-day operations; however, when traveling for treatments, Jim Snabe, the former co-CEO of SAP and chairman of Maersk, Allianz, and Siemens, will be in charge. So, we know that things remain on course even as he battles this unfortunate condition.

Our Target is $50, and our SP is $30. The stock is way below our Sell Price. Perhaps it is time for you to get out, especially with the government cutback going on in Washington. We will hang in here for a few weeks and watch events unfold.

VanEck Semiconductor ETF (SMH: $225, down 1%)

HIGH TECHNOLOGY PORTFOLIO

As the name suggests, the VanEck Semiconductor ETF allocates its assets to the various high-fliers of the burgeoning semiconductor and AI industries. The well-known heavy-hitters in the Fund include Nvidia (NVDA), Taiwan Semiconductor Manufacturing (TSM), Broadcom (AVGO), and ASML Holding (ASML), along with several under-the-radar picks such as Lam Research (LRCX) and KLA (KLAC), among 20 other stocks that it deems crucial for this computing revolution that is upon us.

The Fund hasn’t had a great start to the year, with most of its holdings struggling with high valuations and uncertainties regarding the trade wars. We’ve seen an 8% pullback YTD, and while this pales in comparison to the 120% rally since 2022, investors are perplexed about the future of this Fund and industry, particularly in the near term. We, however, have no such qualms, and neither should you.

Leaving aside all the hue and cry surrounding geopolitics, trade wars, tariffs, technicals, and valuations, what truly matters is the underlying demand for chips and the growing use cases for AI across sectors and businesses, which show no signs of slowing down. We’re trying to say that the secular trends of AI, cloud computing, 5G, and electric vehicles are here to stay and will continue to grow dramatically.

A key feature of the Fund is its concentration across many stocks, but as we’ve discussed in the Newsletter, it’s a double-edged sword. With nearly 40% of its assets allocated to just three stocks, Nvidia, Taiwan Semiconductor, and Broadcom, it captured the phenomenal upside in these stocks during the AI frenzy in 2023 and 2024. But now, as the market has pulled back a little, it is facing the downside, with no diversification to come to its aid.

A recent earthquake in Taiwan caused a pullback in Taiwan Semiconductor, though the company claims it had minimal impact on production. However, the VanEck Semiconductor ETF took a hit, as smaller holdings like Lam Research and Applied Materials—due to their limited allocations and long sales cycles—were unable to offset the losses from larger stocks.

During its recent earnings release, Nvidia CEO Jensen Huang claimed that advanced reasoning AI models require 100 times more computing power than the current models. This matters to us, as it means that we’ve barely scratched the surface so far. The VanEck Semiconductor ETF is one of the best vehicles to ride this trend, with a robust track record and a low expense ratio of just 0.35%.

Our Target is $300, and our Sell Price is $230; as you can see, the stock is below this. We added the stock at $270 last summer, so we are undoubtedly underwater. Should we sell and move on, or hold and hope? Good question. No one knows if the overall market will move higher from here, but if it moves lower, we can be sure that the Fund will fall even more. We’re going to stick with it for the next few weeks.

Zscaler (ZS: $205, up 4%)

HIGH TECHNOLOGY PORTFOLIO

Cloud security giant Zscaler released its second-quarter results two weeks ago, reporting $650 million in revenue, up 23% YoY, compared to $520 million a year ago. Profits during the quarter stood at $130 million, or $0.78 per share, against $100 million, or $0.63, beating estimates at the top and bottom lines, coupled with strong guidance for the third quarter and full-year, lifting the stock following the results.

The company’s calculated billings - contractual revenue yet to be realized - stood at $740 million, up 18% YoY, followed by deferred revenue at $1.9 billion, up 25% YoY. Zscaler continues to ride the rising demand for Zero-Trust architecture and security solutions in an increasingly digitalized world. It fulfilled the promise of simplified enterprise security, which has long been the dream of this industry.

Zscaler now sports a customer retention rate of 115%, which is impressive for a SAAS company of this size. It has nearly 3,300 customers with annual contract values over $100,000 and 620 with ACVs greater than $1 million. During the quarter, we saw several new marquee logo adds, including a Fortune 50 energy company, a Global 2000 manufacturing giant, and a nation-state.

The big story is its new Zero Trust Everywhere Initiative, which bundles its security solutions, helping consolidate tools and services while transferring enormous savings to enterprise customers. This gives it a powerful competitive moat, leaving newer entrants and even a few established players at a disadvantage, unable to match Zscaler’s scale and pricing in enterprise security.

The company is making strides by combining Zero Trust with AI, which many companies are scrambling to access, given the risk of data loss when using AI tools such as ChatGPT and Microsoft Copilot. Zscaler checks data streams going to and from tools like ChatGPT, ensuring no leakage in between. This is a critical solution for enterprises looking to fast-track their AI adoption and workflows.

The stock is up 13% YTD and shows no signs of slowing as the company outperforms and outwits peers. Over the years, it has built remarkable moats that the industry is just starting to notice. With the amount of data it tracks and trains its models on, no new entrant can offer similar solutions at scale. It ended the quarter with $2.9 billion in cash, $1.2 billion in debt, and $900 million in cash flow. Our Target is $280, and the SP is $170. We added the stock at $85 in 2019, so we’d like to see it return to its peak in 2021 at $375.

Dexcom (DXCM: $74, up 4%)

HEALTHCARE PORTFOLIO

Medical devices company Dexcom released its fourth quarter results recently, reporting $1.1 billion in revenue, up 8% YoY, compared to $1.0 billion a year ago. It posted a profit of $180 million, or $0.45 per share, down from $200 million, or $0.50 the prior year. For the full year, the company reported $4.0 billion in revenue, up 11% YoY, with a profit of $670 million, or $1.64, against $620 million, or $1.52.

The decline in profits during the quarter was primarily due to a one-time charge of $21 million due to certain mistakes by Dexcom’s shipping partner. Besides this, the company’s new build configurations took a toll on its production yield and gross margins, which stood at 59%, down from 64% a year ago. Management is taking all necessary steps to get production and margins back on track.

Dexcom’s global user base now stands at an impressive 2.8 million, up 25% YoY, with its newly launched over-the-counter solution, Stelo, already adding 150,000 users within four months of launch. This comes amid growing concerns about competitive and substitutive headwinds among investors. Starting with the popularity of GLP-1 drugs, followed by the entry of Abbott and Medtronic in this segment.

As we’ve covered before, the entire premise of GLP-1 drugs reducing demand for continuous glucose monitoring (CGM) devices is flawed. Regarding the competition, Dexcom is addressing this head-on by rehauling its sales and distribution strategy. It has dedicated enormous resources to training sales reps while expanding existing relationships with medical equipment distributors, which are key to this business.

In addition, it is vying for deeper penetration in existing markets while executing aggressive expansions overseas. During the quarter, the company got three of the largest pharmacy benefit managers (PBMs) to cover its products and is now working to onboard other PBMs. It gained similar coverage in New Zealand and France and is set for more wins across Canada, Germany, and others.

In 2025, the company projects $4.6 billion in revenue and 14% YoY growth. The stock didn’t have a great year last year and is down 50% from its all-time high in 2021, but we expect things to turn around soon. The company has barely scratched the surface of the multi-billion-dollar diabetes industry and ended the quarter with $2.6 billion in cash, $2.6 billion in debt, and $1.0 billion in cash flow.

Our Target is $90, and our SP is $70. We have faith in this company and believe that, given a few more months, it will come out on top in its quest to be the best in its class in this great business of continuous glucose monitoring (CGM) technology. Dexcom has built a reputation for accuracy, ease of use, and innovation, making it the gold standard in CGM technology. With expanding adoption beyond Type 1 diabetes and strong financial growth, Dexcom remains the leading player in the space.

iShares Oil & Gas Exploration & Production ETF (IEO: $93, up 2%)

ENERGY PORTFOLIO

As the name suggests, the iShares Oil and Gas ETF is a fund that provides exposure to the high-fliers of the energy industry. However, note that the fund steers clear of the industry's diversified, vertically integrated giants, such as ExxonMobil and Chevron. It allocates most of its assets to pure-play oil and gas producers, allowing it to track commodity prices more closely.

The fund holds a basket of 51 different securities in the energy space, with its top three holdings, ConocoPhillips, EOG Resources, and Phillips 66, constituting 35% of total assets. So far, this year looks to be a mixed mag for the industry, with supply tightening in key regions of the world such as Iran and Venezuela, but things looking up in the US with a new fossil-friendly White House administration.

However, several geopolitical factors are at play, the most prominent of which are tariffs and trade wars by the US government. Most recently, India agreed to buy more oil and gas from the US instead of Russia, Iraq, and Saudi Arabia. This has sent ripples across the industry and bodes well for the US domestic players and, by extension, the IEO fund.

The US government will likely try to reach a similar deal with Europe. With Russian supply still under sanctions, the path is clear for American companies to dominate the global energy industry. US LNG supplies to Europe have already risen over 3,700% since 2017 and will go higher with Russian gas transit through Ukraine now blocked and Europe looking to wean itself off Russian energy entirely.

Asian markets have been out of reach, mainly due to the distances involved and partly the high fees levied by the Panama Canal. The Trump administration is now dealing with the latter, which would be a win for US oil and gas giants. Of course, in the long run, how the industry fares depends a lot on whether the US keeps sanctions on Russia.

The iShares Oil and Gas ETF didn’t have a great year in 2024 and is flat YTD, but things are looking up for its constituents, at least in the mid-term. There are several reasons to love this fund, with a few prominent ones being its low expense ratio of just 0.40%, annualized yield of 2.5%, and an illustrious track record going back nearly two decades. Over the past five years, the fund has returned 320%.

Our Target is $120, and our Sell Price is $95.

Range Resources (RRC: $40, up 4%)

ENERGY PORTFOLIO

This company is one of the largest natural gas producers in the world and released its fourth quarter results recently, reporting $630 million in revenue, down 34% YoY, compared to $940 million a year ago. It posted a profit of $160 million, or $0.68 per share, against $150 million, or $0.63, performing admirably despite bottom-tier gas prices, with results hinting at strong cost controls and execution excellence.

For the full year, the company reported $2.4 billion in sales, down 28% YoY, compared to $3.4 billion a year ago, with a profit of $560 million, or $2.30, down marginally from $570 million, or $2.40. Production averaged 2.18 billion cubic feet equivalent of natural gas per day, coming in ahead of estimates, with 68% being natural gas and the rest comprising natural gas liquids and crude oil.

The company took a hit at the top and bottom lines during the quarter, owing to comparatively lower realized prices. Natural gas realizations stood at $2.36 per million cubic feet equivalent, down from $2.40 last year. Natural gas liquids, however, saw an uptick to $26.43, compared to $24.91, while its negligible crude oil output saw a decline in realizations at $59 per barrel, down from $68 last year.

However, realizations were well ahead of Henry Hub averages, owing to the company’s efforts in marketing and exposure to better-priced markets in the Midwestern and Gulf regions. Even as domestic prices remain under pressure, Range has executed well enough to benefit from prevailing dock constraints and global demand tightness, which we expect to persist.

Range Resources is known for its operational efficiencies that allow it to keep its head comfortably above water even during harsh conditions. Throughout the year, it ran a 2-rig, 1-frac crew operation, which means only two rigs were operational at any given time, with one completion crew digging 800,000 lateral feet across 59 wells, with an average of 14,000 lateral feet per well, thus maximizing efficiencies.

The company is also renowned for its capital allocation. During the quarter, it used its $450 million cash flow to pare down its debt by $170 million while returning $140 million to investors through buybacks and dividends. All-in capital expenditures for the year stood at $650 million, and its balance sheet continues to grow more robust, with $300 million in cash and just $1.8 billion in debt.

The stock has been a solid investment for us - we added it at $28 in 2022. It would be nice to see it at $90 like it was in 2014. Our Target is $41, and our Sell Price is $27, which are moving today to $50 and $33, respectively. It’s a relatively small firm, clocking in at just under $10 billion in market cap, and it is certainly a buyout candidate. With higher crude prices later this year or early next, we can see this stock back up to the $50+ level.

Ally Financial (ALLY: $36, up 7%)

FINANCIAL PORTFOLIO

Banking and auto finance giant Ally Financial released its fourth quarter results recently, reporting $2.1 billion in revenue, up 5% YoY, compared to $2.0 billion a year ago. It posted a profit of $250 million, or $0.78 per share, against $120 million, or $0.40 the prior year. Despite bearing the brunt of a $560 million credit provisioning against bad loans, this also hints at a phenomenal year ahead.

The company originated $10.3 billion of auto loans during the quarter, up 7% YoY, with a weighted average yield of 9.6% and 49% of originations in the higher credit quality tiers. This is down a bit from their yearly average of 10.4% in response to falling interest rates. Still, the company’s net interest rate margins hold steady at 3.3%, leaving plenty of cushion to deal with uncertainties.

Ally’s insurance business continues to grow, with $370 million in written premiums during the quarter, up from $330 million a year ago. Retail deposits stood at $143 billion, up from $142 billion across 3.3 million customers, and an average retention rate of 95%. During the fourth quarter alone, the company saw retail deposit growth of over $2.0 billion. The company is a top-tier banking services provider.

The big story during the quarter concerns the sale of its credit card business, which, despite being a good business, allows Ally to focus all of its efforts and resources on its core offerings, banking and auto financing. It called to cease mortgage originations, which only offer 3% yields, so this move is expected to free up capital for other high-yielding loans and investment opportunities.

Ally has been restructuring its operations, which involve extensive workforce reductions, resulting in savings worth over $60 million annually. The sale of its credit card business is expected to dampen net interest margins in the medium term, as the segment yields over 20% annually. Still, it will minimize future credit costs and operating expenses, and this restructuring should help offset the loss of revenue.

The stock was flat last year and continues to be range-bound so far this year, but things are turning around for the company as all of its restructuring efforts start to pay off. The company did not buy back any stock during the year, but its dividend yield has increased to 3.3%. It ended the quarter with $10.3 billion in cash, $18.3 billion in debt, and $4.5 billion in cash flow.

Our Target is $52, and our Sell Price is $35.

Welltower (WELL: $147, down 1%)

HEALTHCARE PORTFOLIO

Leading healthcare REIT Welltower released its fourth quarter results recently, reporting $2.3 billion in revenue, up 29% YoY, compared to $1.7 billion a year ago. It posted a profit, or FFO, of $720 million, or $1.13 per share, against $530 million, or $0.96. For the year, the company reported $8.0 billion in sales, up 20% YoY, with a profit of $2.6 billion, or $4.32 per share, against $1.9 billion, or $3.64.

Welltower had a strong quarter on the operations front, with same-store operating income growing 24% YoY, marking its ninth consecutive quarter of 20-plus percentage gains. The occupancy rate stood at 87%, rising by an impressive 310 bps YoY and 120 bps sequentially, which management noted was during the time of year when move-ins often moderate, hinting at a growing broad-based momentum.

The company has over 750 healthcare facilities in the U.S., Canada, and the U.K.

During the quarter, Welltower deployed $2.4 billion across 21 different transactions, with $2.2 billion in acquisitions and loan funding and $230 million in development funding. This is a 20% decline YoY from $3.0 billion a year ago, but it marks an end to a tremendous year of investment activity, with YTD acquisitions totaling $7.0 billion, up 19% YoY, compared to $5.9 billion during the same period last year.

The company is also off to a great start this year, with $2 billion in gross commitments under contract within the first six weeks. Management attributes this to favorable market dynamics, with the over-80 population rising quickly and limited new supply owing to high interest rates and rising material costs, coupled with a new immigration policy making it harder for competitors.

Welltower is pursuing a renewed approach to capital allocation, focusing on ‘Local Clustering,’ which involves ‘going deep, not broad.’ Thus, the company will allocate more capital in each region, aiming for more properties and density instead of diversifying across many areas. This allows for plenty of cost synergies, which can be beneficial as the new RIDEA structure gains steam.

The RIDEA structure allows Welltower to participate in the operating profits of its facilities, as opposed to merely earning rent. This can be a game-changer for the entire industry, particularly senior housing. The stock is off to a great start, rallying 17% YTD, and the firm maintains a robust balance sheet as it enters a lucrative period, with $3.5 billion in cash, $16.8 billion in debt, and $2.3 billion in cash flow.

Our Target is $155, and our Sell Price is $115. It hit $157 a few weeks ago and has pulled back an inch. We’re raising our SP to $130 and can’t wait to raise the Target to $180 in another few weeks as it passes $150.

-----------------------------------------------------------------------------

The Bull Market Report High Yield Investor

Fed meetings has gotten shorter and sweeter lately: no change in interest rates, thus minimal reaction from the market. Once again, Powell and company hit "pause" while they wait to see what trade policy does to consumer prices. If inflation edges up a bit, that pause will lengthen or force the Fed to tighten again in response.

But if the economy takes a sharp enough downturn to shake the job market, you can bet that the rate cuts will start up again fast and furiously. That's never been far from Powell's mind or commentary in recent years. He's willing to tolerate a mild recession in order to kill inflation but anything that aspires to the catastrophic levels of 2008 or 2020 will trigger massive retaliation.

As it is, the now-notorious "dot plot" that telegraphs the Fed's sense of its next moves remains clear. Three months ago, Powell and company thought the economy would expand at a healthy 2.1% rate this year. Now that GDP growth number has come down to 1.7%, which is not "better" but still a long way from the apocalypse. The Fed doesn't really think that growth will get much lower or much higher than this in the long run, so this is roughly as good AND as bad as it gets. This is normal.

Likewise, the Fed doesn't see unemployment rising or falling much from here. Again, in their view this is normal. Remember, they get all the macro data the government produces. When they make a forecast, it's usually pretty good. And they see inflation going down on its own, which gives them leverage to make as many as two rate cuts this year and then another two next year. Not a quick race back to the zero-rate world, but guess what? That world, created in the long shadow of the 2008 crash, was never normal. From here, rates may edge up and down but barring an extreme economic surprise, this is the world we live in now.

In this world, cash is unlikely to pay more than 4% and even long-term Treasury yields may have peaked. To earn a higher rate of return, you need to reach beyond the federal bond market into areas that have been neglected or even actively shunned. Muni bonds, for example, have been under serious pressure as some regions of the country teeter closer to recession and maybe even default, but that's an opportunity if you know how to pick the people who can pick the best bets in the field. Here's one of our favorites:

Invesco Municipal Trust (VKQ: $9.73, down 1%. Yield=7.3%, the equivalent of 10.3% taxable)

HIGH YIELD PORTFOLIO

The Invesco Municipal Trust is a closed-end fund that primarily invests in tax-free municipal bonds, making it very appealing to conservative, income-seeking investors. The fund still goes the extra mile in the relatively risk-free muni space. Further, it diversifies its holdings while actively managing and rebalancing them to drive additional value for investors, making it perfect for risk-averse investors.

Muni bonds had a modest year in 2024, with total returns of just 1.05%. It was an election year with major consequences for the debt markets and started with relatively high interest rates. We saw a jump in late 2024, right after the election, in anticipation of pro-growth policies by the incoming administration, with high-yielding munis ending the year with over 6% in gains.

In 2025, the year has been a mixed bag for the segment, starting with yields dipping in January in response to cooler inflation readings. However, this was followed by rising yields in February and March, with new issuances pressuring muni prices. Right now, yields are at their highest in over 2 years, with the Fed’s ‘higher-for-longer’ policy bias keeping volatility in the segment elevated.

Last year, we saw record new issuances worth over $500 billion, which marks a YoY increase of 36%, and most analysts expect the market to surpass these figures in 2025. The good thing is that there is plenty of demand for muni bonds to soak up these new issues, with the asset class now being deemed the most attractive among its fixed-income peers when weighing it on an absolute yield basis after tax.

With plenty of uncertainties surrounding global equity markets and the potential implications of a trade war and other geopolitical tensions, munis are a much-needed safe haven that will see billions of dollars in new inflows over the next few months. As long as their tax-exempt status remains, we expect the asset class to continue going strong with plenty of new issuances and inflows.

One of the reasons for the uptick in activity is the ongoing talks of altering the tax-exempt status of munis in Washington. This has led to the front-loading of issuances before any such policy changes. However, we firmly believe that any such changes will be fairly limited, such as capping the deductions for wealthy investors. None of this should matter for long-term investors, especially with a fund such as the Invesco Municipal Trust, given its illustrious track record for several decades.

Our Target is $13, and our Sell Price is $9.

Good Investing,

Todd Shaver, Founder and CEO

The Bull Market Report

Since 1998

by Todd Shaver | Aug 27, 2017 | Weekly Newsletter 7pm Sunday

The Weekly Summary

What a week. So much for a quiet end to the summer. Yellen made perhaps her final speech in Jackson Hole. Trump is battling a debt ceiling to fund The Wall. And the markets are partying like it’s 1999!

Federal Reserve Chair Janet Yellen, speaking in Jackson Hole, Wyoming, on Friday, issued her broadest defense so far of the government’s response to the 2008 financial-market meltdown while outlining some areas that regulators could review to improve efficiency in the financial system. “Any adjustments to the regulatory framework should be modest and preserve the increase in resilience at large dealers and banks associated with the reforms put in place in recent years,” Yellen said, in what could be her final speech as Fed chair at the annual gathering of central bankers. Her term expires in February.

President Donald Trump is spoiling for a fight with Congress over funding a border wall with Mexico, but he’ll have a hard time waging that battle because of a looming deadline to avert a U.S. debt default. Some of the president’s advisers consider a tough stand on border wall funding crucial to Trump’s credibility, two White House officials said. Some say that failure to make progress on the border wall -- or at least go to the mat on the issue -- may fracture what has been a solid political base for the president.

In 1999, then-Federal Reserve Chairman Alan Greenspan kicked off the central bank’s annual Jackson Hole symposium by highlighting the impact of rising stock prices on an economy that was then enjoying low inflation and low unemployment. Now today, eerily similar, buoyant asset prices and low unemployment argue for Yellen to press ahead with interest-rate increases -- or even accelerate them. Weak inflation suggests she might even want to consider providing more stimulus, not less. That would mimic the tack Greenspan took 18 years ago, when, faced with a frothy stock market, he continued to hike rates until May 2000. The result was a disaster for the stock market -- the technology-heavy Nasdaq Composite Index plunged by 78% over a 2.5 year period from its peak as the dotcom bubble deflated -- but was not all that bad for the economy. Gross domestic product did contract during 2001, but the fall was so small that former Fed Vice Chairman Alan Blinder has called it a “recessionette.” And inflation remained contained. “There are a lot of similarities,” between the late 1990s and today, said Laurence Meyer, who was a Fed governor from 1996 to 2002.

No matter what is happening out there, there is always a bull market here at The Bull Market Report! This week we highlight some of our favorite stocks/funds where we think you can still make good money, including: high yield equities like Annaly or larger caps like Amazon, Facebook, First Solar, Google, Microsoft, and Netflix, as well as small caps like Nutanix.

BMR Companies & Commentary

Amazon (AMZN: $945, down 1%, (for the week))

Amazon Announces New Online Teaching curriculum TenMarks Writing. TenMarks Writing is a new online curriculum designed for teachers to help their students improve their writing skills by using scaffolding, an instructional technique in which students learn step-by-step how the writing process builds.

TenMarks Writing incorporates natural language processing technology to provide students with automatic, personalized feedback and helps teachers deliver differentiated comments as students work through their compositions. It is available for $4 per student for an entire year.

BMR Take: This is just the latest example of another new innovative effort by Amazon. We call Amazon the innovation machine for a reason. Hardly a week goes by without something new and creative coming out from the company. We all know about their entry into food (Whole Foods is part of Amazon as of Monday) and now education. Will this be a major push by the firm? We shall see.

Facebook (FB: $166, flat)

Facebook Usage Growth May Slip among Teens, Young Adults. According to eMarketer's latest forecasts, usage rates for Facebook, Instagram and Snapchat are running roughly in parallel between the US and UK, with Instagram and Snapchat expected to rise by double digits. However, Facebook will see its user growth continue to slow in both countries as lessening usage among teens and young adults drags down overall user growth. Monthly Instagram usage in the US will grow 24% in 2017 to 85 million, also higher than previously forecast.

BMR Take: Do not be alarmed. We repeat. Do not worry. This news of “lowered estimates” and all the talk on TV of slowing engagement for Facebook means very little. It sounds bad. But the reality is engagement is healthy and the bigger factor is new user growth, which remains robust.

First Solar (FSLR: $47, down 1%)

First Solar Sells California Project. This week First Solar announced it completed the sale of the 280 Megawatt (MW) California Flats Solar Project in Monterey County to global private asset manager Capital Dynamics. Terms of the deal were not disclosed.

Located on approximately 2,900 acres of ranch land within the Jack Ranch owned by the Hearst Corporation near the San Luis Obispo and Monterey County borders, California Flats comprises two phases. The 130 MW first phase is expected to be commissioned in 4Q17, and is fully contracted under a long-term Power Purchase Agreement (PPA). The 150 MW second phase, which is currently under construction, is expected to be commissioned by the end of 2018, and is fully contracted under a long-term PPA.

BMR Take: We like this. We understand the cash is going to be reinvested in part of the business with much greater growth prospects. This is just want we want to see from the management teams running the companies we follow.

Google (GOOG: $915, up 1%)

Google and Walmart partner on Voice Shopping. Now people who own a Google Home will be able to order things by voice from Walmart. Cool! But this is copying Amazon Alexa, to be frank. If you can’t beat them join them.

The companies will also participate in the Google Express shopping marketplace, for which Google will eliminate the $95 annual membership fee. Shipping for orders through Google Home or Google Express will be $5 per order, or free if the order reaches a certain level. Costco, Walgreens, and PetSmart already sell via Google Home.

BMR Take: Good news for Google. Amazon is trailblazing the way forward with new innovations by spending tons of money. But there are competitive factors and various stakeholder conflicts, which creates room for companies like Google to jump in with little upfront capital investment, creating great investment opportunities. This could be the start of something big.

We've noticed that Google is lagging the rest of the market. After hitting $980 a month ago, the stock has faded a bit. It seems like a lot, but it's like a $98 stock dropping to $92, not really a big deal. So what do you do from here. You sit back and realize that the market is giving you a huge buying opportunity. Repeat after us: The market is giving you an opportunity to buy the stock a lot cheaper than its all-time high of $988 in June.

Microsoft (MSFT: $73, flat)

Microsoft Acquires Cycle Computing to Accelerate Big Computing in the Cloud. From finding a cure for cancer to making vehicles safer to fulfilling the promises of artificial intelligence, today’s complex problems require the ability to harness massive amounts of computing power. For too long, Big Computing has been accessible only to the most well-funded organizations. Microsoft believes that access to Big Computing capabilities in the cloud has the power to transform many businesses and will be at the forefront of breakthrough experimentation and innovation in the decades to come. Thus far, Microsoft has made significant investments across infrastructure, services and partner ecosystems to realize this vision.

As a further step in this direction, Microsoft recently acquired Cycle Computing, (no price details given), a startup specializing in helping companies perform heavy-duty computing. That includes crunching data for developing new drugs and analyzing risk in the financial services industry. This will make it easier than ever for customers to use High-Performance Computing and other Big Computing capabilities in the cloud. The cloud is quickly changing the world of Big Compute, giving customers the on-demand power and infrastructure necessary to run massive workloads at scale without the overhead. Your compute power is no longer measured or limited by the square footage of your data center.

BMR Take: We’ve already seen explosive growth on Microsoft Azure in the areas of artificial intelligence, the Internet of Things and deep learning. As customers continue to look for faster, more efficient ways to run their workloads, Cycle Computing’s depth and expertise around massively scalable applications make them a great fit for customers. We expect big growth ahead and see Microsoft’s business in a very healthy place.

Netflix (NFLX: $166, flat)

We are not afraid to tell you the good, bad, and the ugly. We know you count on it. We unfortunately have to report that Netflix will lose Disney content in 2019. Disney will end Netflix's film distribution deal as it launches its own streaming services starting with an ESPN service in 2018 and a Disney/Pixar service in 2019. Netflix had inked a deal with Disney to stream films and content just a year ago.

Netflix's stock traded lower on the news as investors see the premature end of the distribution deal as a loss of popular exclusive content. Some have compared the deal termination to the Starz (another Disney property) refusal to renew with Netflix in 2011 and see the move as another example of increasing license renewal risk and streaming competition.

BMR Take: The future of content creation is the holy grail of the media business. While Netflix can survive this one lost deal, the question is how much more of this will we see in the future. There is a long way to go until it is a big problem. But we are worried. Our Target is and has been $165. The stock was higher in July as it rocketed from $146 to $189 but it has fallen since. With a market cap of $72 billion and a PE of a ridiculous 215, we believe it is time for us to put this one to bed. We hereby remove the stock from our Stocks for Success portfolio with a gain of 65% since early 2016. There are lots of better places for your money at this time.

Have you taken the time to go onto the BullMarket.com website? Check out the six portfolios – you’ll find some interesting ideas here for the profits from Netflix.

Nutanix (NTNX: $22, flat)

Cisco Systems announced its intent to acquire Springpath, a leader in hyperconvergence software, for $320 million in cash, with the transaction expected to close in 1Q18. Springpath has developed a distributed file system purpose-built for hyperconvergence that enables server-based storage systems, and Cisco believes the acquisition will allow it to continue to deliver next-generation data center innovation to its customers.

In terms of Cisco, the acquisition was not a surprise, as the two companies have a relationship that goes back to Springpath's 2012 founding and Cisco previously making an investment in the company with an option to acquire it. That said, it is still a bummer for Nutanix. Analysts believed Cisco was a potential acquirer of Nutanix.

BMR Take: Hyperconvergence software is an exploding market. We expect Nutanix to do great things and generate big growth. The stock is hovering our Sell Price and we have had tons of calls and letters about whether we would “sell” the stock. First of all, we don’t own the stock. We don’t buy any of our recommendations as we want to remain clear of any conflict of interests. Secondly, the Target and Sell Prices are there for YOU to decide what to do with your investment. All of you are different. Some have multiple millions and some of you are just getting started. So you have to weigh every investment as it affects you and your family.

With that said, we believe Nutanix will be a big, big winner. Revenues are strong with last quarter coming in at $192 million vs. $115 million the year before. This is HUGE. But remember, this is a small cap stock – tiny in comparison to a Facebook or Google. The market cap is just $3.3 billion. So watch and wait and make a decision for yourself and your family. We think the company is a potential great one, but the market is stretching our patience.

We found this interesting too:

Firsthand Technology Value Fund, a publicly traded venture capital fund that invests in technology and cleantech companies, disclosed that its top five holdings as of July 31, 2017, included Nutanix. The fund’s investment in Nutanix consisted of 460,000 shares of common stock and represented approximately 7% of the fund’s total.

Upcoming Economic News

Consumer Confidence

Tuesday, August 29th, 10:00 AM ET

Period: August

Consensus: 120.0

Prior: 121.1

ADP Employment Survey

Wednesday, August 30th, 8:15 AM ET

Period: August

Consensus: 180,000

Prior: 177,700

Personal Consumption Expenditure

August 31th, 8:30 AM ET

Period: July

Consensus: 0.40%

Prior: 0.10%

Apple Has Debt Too

A few of you have written us and given us grief because we only report Apple’s cash position and don’t report the debt levels. Our internal excuse has always been that Apple’s debt is at very low interest rates. Here are some examples of Apple’s debt:

Apple 2.4% 5/03/2023 $5.5 billion

Apple 1.0% 5/03/2018 $4.0 billion

Apple 4.65% 2/23/2046 $4.0 billion

Apple 3.25% 2/23/2026 $3.25 billion

Apple 2.85% 5/06/2021 $3.0 billion

Apple 3.85% 5/04/2043 $3.0 billion

Apple 2.25% 2/23/2021 $3.0 billion

Apple 3.45% 5/06/2024 $2.5 billion

Here is some more detail:

From their latest financial reports, the last three yearly balance sheets ended September have shown that debt has risen from $29 million in 2014 to $53 million in 2015 and to $75 billion in 2016. At the same time cash has risen from $154 billion to $206 billion to $236 billion, reaching $260 billion in their last quarterly report on July 1st.

So: Big cash. And big debt. The NET CASH position at year-end September 2016 was approximately $160 billion. (And much higher now.)

We’ll take it.

Opko Health (OPK: $6.13, flat) Two weeks ago, the company reported earnings for 2Q17. Total revenues of $314 million were down 12% year over year from $357 million. Revenues included a $10 million payment associated with the commercial launch of Varuby in Europe in comparison to the $50 million payment related to a Rayaldee license in the same quarter in 2016.

Research and development expenses totaled $33 million, up 4%, while selling, general and administrative expenses amounted to $128 million, up 9% year over year. Consequently, loss from operations came in at $4 million, highlighting a significant decline from an operating income of $55 million in the prior-year quarter. The decline can be attributed to a rise in operating expenses owing to the company’s significant investments associated with the commercial launch of Rayaldee along with consistent investments in the pharmaceutical pipeline.

The company has $130 million in cash, unchanged from the quarter before.

This is a biotech company in an industry that is known for companies with years and years of little or no progress (and revenues) and then a big announcement of great success. Luckily Opko isn’t in the camp of no revenues. Revenues as you know are over $1 billion.

Chairman and CEO Frost On the Impact of Opko’s 4Kscore

Released in 2014, the 4Kscore Test is the only blood test that can accurately identify a patient's risk for aggressive prostate cancer, Opko claims. As calls to reduce health care costs across the United States grow louder, 4KScore is as a cost-effective alternative to biopsies, Frost said.

About 30 million tests are done each year to measure men’s prostate-specific antigens, or PSA. Of those, 4 million identify elevated PSA levels and typically would require biopsies.

“If you do the test after the elevated PSAs, you can avoid 50% of all biopsies,” Frost said. “This is the type of thing that if you wanted to be able to cut healthcare costs in this country, this has to be the easiest thing in the world to do.”

On why he continues to buy thousands of OPKO shares

“I always believe in investing in things that I know about rather than things I don’t,” Frost said.

BMR Take: Opko Health is a relatively small biotech firm with great potential. Many times “great potential” results in “no results.” This $3.4 billion market cap company is poised for success, but remains the most speculative stock in our six portfolios.

Splunk (SPLK: $65, up 10%)

Splunk had a great week. They reported earnings on Thursday after the close and they were stellar. This is what we have been waiting for. Revenue rose to $280 million from $213 million a year ago, for a percentage gain of 31%. Huge quarter. Adjusted earnings were $11 million or 8 cents a share.

Guidance is solid with next quarter revenue of $308 million. Operating margins are projected to be approximately 8%.. Growth in yearly revenues has been spectacular. For the last three years we have seen $450,000,000, $670,000,000 and $950,000,000. For fiscal year 2018, ending this coming January, revenue is now expected around $1.21 billion.

Billings in the quarter grew 32% year over year to $303 million. They again increased full fiscal-year 2018 guidance to call for billings of $1.45 billion.

Splunk has been ranked number one in worldwide IT Operations Analytics (ITOA), as well as Event and Log Management software market shares for 2016 by International Data Corporation. Splunk said that these two markets have witnessed the highest growth rates within the overall IT market, with ITOA seeing an increase of 33%, and Event and Log Management growing 23%. This is the third consecutive year that Splunk took the top spot in the ITOA software market, beating the competition of IBM, Microsoft, Hewlett Packard Enterprise and VMware.

More than 500 new customers were added during the quarter, including Athenahealth, Carnival Cruise Lines, the Department of Homeland Security, Harvard Business School, Shutterfly, Uber, and Verizon.

Splunk appears quite dominant in its machine data analytics niche. And the company's market opportunity is growing as its software, traditionally used for IT operational intelligence, gets adopted for security, fraud-detection, app analytics and other use cases.

BMR Take: Great quarter. Looking for continued growth for years to come. Our Target is $75 and our Sell Price remains $60. Note that Splunk has exceeded guidance for 11 straight quarters.

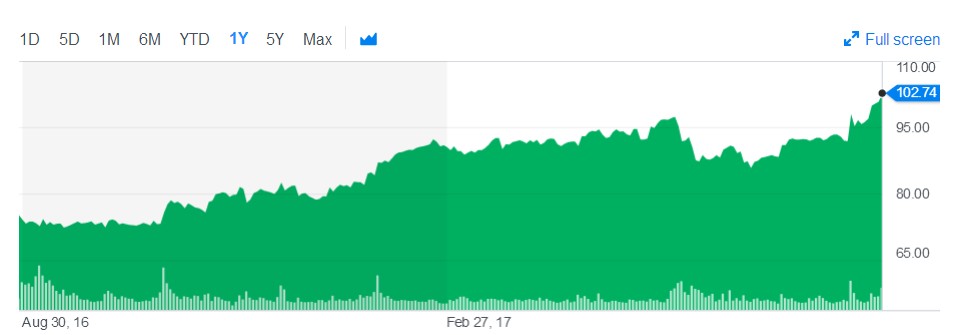

VMware Has a Strong Quarter

VMware ($103, up 7%) had a great week after reporting $1.9 billion in revenues up from $1.7 billion last year with net income of $335 million up from $265 million, $1.19 a share up from $0.97. Huge. Total cloud management bookings rose by a 13% year over year, and the company closed 10 deals valued at over $10 million. Network Virtualization (NVX) revenues were again strong, at over a 40% increase.

The company guided for the year: Revenue of $7.83 billion, EPS of $5.06, and free cash flow of $2.7 billion. These are big numbers.

VMware raised $4 billion earlier this month in a debt offering, mostly overseas, with coupons of 2.3% to 3.9%. Note that Dell Technologies owns 82% of VMware.

Take a look at this chart:

BMR Take: We think you get the drift!

A Word from Gary Jefferson

Jefferson Financial Group

First Vice-President, Investments

UBS Financial Services, Inc.

As Alfred E. Neuman might say, "What – me worry?" ……as in why care about things such as 1) When will the Fed hike rates again and how many hikes can we expect? 2) Has the 2nd quarter economic rebound already been priced into stocks? 3) Are tax cuts still possible or has the pro-growth agenda been totally derailed by swamp politics? 4) Will we have a trade war with China? 5) Will we go to war with North Korea? 6) Are we headed into a recession?

Sure, we care and everyone else should care about getting tax relief. We have the worst tax system in the world if you don't count dictatorships. But we've lived in the current system for decades and so, while it would be a whole lot better if we got tax reform, investors and the stock market will survive if we don't. We also admit that of course we would care if we had a war. That is highly unlikely however, because none of the large powers has any desire to start WW III. Otherwise, worrying about all of the above is not a good idea - or, as Mom used to say, "If you worry too much, you'll worry yourself to death." So, we are adding a little bit of Alfred's advice to our medicine cabinet and are just going to go on about our business and not worry too much.

Business as usual with all these worries hanging around (stocks love to climb a wall of worry) generally means an investor should expect more volatility. We expect just that. We know stocks tumble way faster than they go up. Thus, we know not to panic - and that is a huge plus for every investor. Or, we might have a little cash to buy into any sale that may come along. Or, we have dividend stocks that will reinvest into more shares whenever they go on sale. And finally, we aren't going to worry about a recession now because the facts simply don't support it. We've looked at inflation, housing starts, retail sales, industrial production, oil prices -- there just isn't any "big trouble" in the economy today.

Not only that, it wasn't that long ago when the US economy seemed like the only regional power heading in the right direction. Europe had record joblessness and was teetering on the edge of recession. Japan was in its 20th year of malaise and China was headed for a hard landing if not a total crash.

Today, all of these regions are showing signs of renewed strength. European markets are doing better than expected. Japan also recently impressed with a +4% GDP growth rate - well above estimates - and China has emerged from a soft patch with a string of positive economic readings. With 40% of US corporate profits coming from abroad, all of the above is then a simple equation pointing to more earnings growth and share price appreciation ahead.

T. Rowe Price once said, "No one can see ahead three years, let alone five or ten." So, we aren't forecasting that conditions won't change in the immediate or distant future. But for the time being, we still see the glass as half full.

A Little Unsettling News

We follow the trends in cash flows into and out of mutual funds. We remember well, back in the 2004-2007 time frame the cash inflows into the stock market were consistent, month after month as cash poured into the market. But we noticed recently that cash outflows are continuing these past few months. U.S. equity funds suffered their longest streak of outflows in 13 years as growing signs of political deadlock in Washington cast doubt on a rally that has taken the S&P 500 Index to record highs.

Investors pulled $2.6 billion from U.S. stock funds in a 10th consecutive week of outflows. That takes total outflows since late June to $30 billion, which covered the week to Aug. 23.

BMR Take: This is serious stuff in our book. We’ve watched these stats for over 30 years and we have found it to be a strong indicator of future prices. We’re watching this one closely.

The High Yield Report

By Michael Foster

Senior Writer

The Bull Market Report

This week could best be described as dull. High yield investments neither enjoyed the euphoria that some assets enjoyed earlier this year, nor continued the panic that we saw in recent weeks due to political noise.

This is not terribly surprising; as we’ve said repeatedly in this column, the fundamentals are strong and there’s little reason to expect a selloff anytime soon. At the same time, however, there is little reason to believe the strong bull run of previous months is going to continue - a lot of the upside is already priced in. That puts us in the rather boring “hold and collect income” position, but when that income is 8% or more on high yield assets, that dullness is quite enriching.

So let’s get specific on a few of our high yield investments in this dull week. A number of Bull Market Report recommendations moved through the week quietly, including several REITs. Omega Healthcare Investors (OHI: $31, up 1%), Apollo Commercial Real Estate (ARI: $17.84, flat), and Ventas (VTR: $68, up 3%). These REITs suffered some volatility earlier this year but have had a much better long-term performance. Much more importantly for us, their dividends remain safe as ever - the recent market turmoil and even more recent market calm have not impacted the income streams of these funds.

Omega in particular is worth a close look because of its high yield and aggressive dividend growth policy. Its 8.2% dividend yield implies a lot of risk, but its dividend coverage ratio over the last twelve months is 134% - far higher than many comparable REITs, and even higher than a lot of lower-yielding REITs. We’ve pounded the table on Omega several times this year for this reason, and with good reason. There os just too much safety in this dividend relative to its yield; if you don’t already own Omega, ask yourself why you aren’t enjoying a growing 8.2% dividend that is more covered by FFO than several 3-4% yielding REITs? And if you have a good answer to that question, let us know, because we can’t imagine there is one.

Elsewhere, municipal bond funds had a quiet week, with both Nuveen AMT-Free Municipal Credit (NVG: $15.49) and Invesco Municipal Trust (VKQ: $12.94) ending the week flat. To understand this, let’s talk a bit about Treasury yields. A big reason why muni bonds fell so heavily in mid-2016 (which is why we waited to recommend them until the end of the year) is that the market was pricing in steep interest rate increases throughout 2017. While we’ve had two rate hikes so far and a third expected in December, (although the probability of even that is declining), that’s less than the Fed had hinted at in 2016. That’s good for municipal bonds, which is why muni bonds have had a strong showing in 2017. For instance, the Nuveen fund we’ve recommended is up 7.2% year-to-date on price alone - that’s less than 200 basis points less than the S&P 500, despite muni bonds’ much lower risk profile and the fund’s 5.6% dividend yield!

The reason for this strong run up in muni bonds - and their relative quiet last week - has to do with interest rates. The market priced into munis a fast pace of rate hikes in 2017, but the reality is that the rate hike schedule is getting longer and longer - meaning the value of munis isn’t going to go down as much as was previously expected. Since the downside was 100% priced in, the lesser downside means these assets were priced too cheaply. And so they’re going up in 2017. It’s also partly why muni bonds have seen relative volatile price movements both up and down in the last couple of years.

Is it still a good time to buy munis? Maybe - it isn’t as clear of a good buy as, say, Omega Healthcare, but holding these funds and collecting their tax-free income stream right now makes a lot of sense.

And there are other interesting options out there, such as the strong performing Digital Realty Trust (DLR: $118, up 3%) and AstraZeneca (AZN: $29, flat). Both of these names are riding a strong wave of momentum thanks to growth in the companies’ fundamental businesses. AstraZeneca was far underpriced last year due to fears of regulations that obviously are not coming anytime soon. Additionally, the drug pipeline is as strong as ever. Similarly, endless demand for server space has made Digital Realty Trust a no-brainer at almost any price. The only problem is that the price growth has lowered their yields - Digital Realty is yielding 3.2% and AstraZeneca is down to 4.8%. It’s becoming clearer and clearer that these two names really should be considered growth or value investments rather than high yield investments. If your goal is to secure a high rate of current income, these names aren’t exactly for you. However, if you appreciate companies with growth potential that haven’t had their future growth fully priced in, but have decent dividends, both names are definitely worth serious consideration.

In any case, the last few weeks have given us a very clear lesson again: Short-term panics based on political headlines are not reasons to sell investments, while fundamental trends in terms of economic demand and dividend coverage are. Financial considerations tell us there’s really nothing to worry about right now.

Good Investing,

Todd Shaver, CEO, Founder and Editor

The Bull Market Report

Founded 1998