THE FREE BULL MARKET REPORT for December 30, 2019

The Weekly Summary

As the year winds up, the only question left for 2019 to answer is how far back you need to go to get a stronger year. The market this year is close to what we saw in 1998, and we would settle for matching that ultra-bullish dot-com boom. Beyond that, it only takes a few extra percentage points of victory lap before we need to pull out 1975 and even 1958 to find a comparable rally on the books.

Of course BMR stocks are up 41% so far this year, so we're rolling in outperformance either way. A full four of our recommendations doubled, tripled or quadrupled in 2019 and a wide range of others (including mighty Apple itself) are in the 80-95% zone. Only six BMR stocks went down. We're confident that they'll come back strong in 2020.

But then 2020 is the real question Wall Street needs to answer. In our view, the new year will start a lot like the last one, with stocks moving strong to the upside. All we need is a little relief on trade or some sunshine in the coming 4Q19 earnings season to carry the bulls into the summer, at which point the political landscape will undoubtedly get too hot for many investors to handle. That's all right. As long as we stick to our game plan, the election shouldn't hurt us one way or the other . . . and in any event, it's nearly a year down the road, so there isn't a lot of sense in worrying about the results at this stage.

There’s always a bull market here at The Bull Market Report! Gary Jefferson is back with a powerful look at what 2020 is likely to bring us, while The Big Picture focuses on the way markets can swing from dread to exuberance. The rally we're enjoying now isn't any more "irrational" than normal. As such, The High Yield Investor discusses some avenues if you're looking to lock in a little added income before the old year ends. We suggest taking a fresh look at Office Properties Income Trust and Omega Healthcare Investors.

The rest of our paid subscription newsletter is devoted to a few of our biggest winners of 2019 like Anaplan and Alphabet, along with some BMR stocks that fell hard in recent months but are already rebounding fast: Okta, Alteryx and Twitter.

Remember, the last day you can buy or sell stocks this year is Tuesday. Wednesday will be a market holiday and then we start fresh in 2020 on Thursday. As usual, our News Flashes will be a little light this week . . . if there's nothing to say, we won't bore you with filler. Instead, we'll be working behind the scenes to get you ahead of the new year.

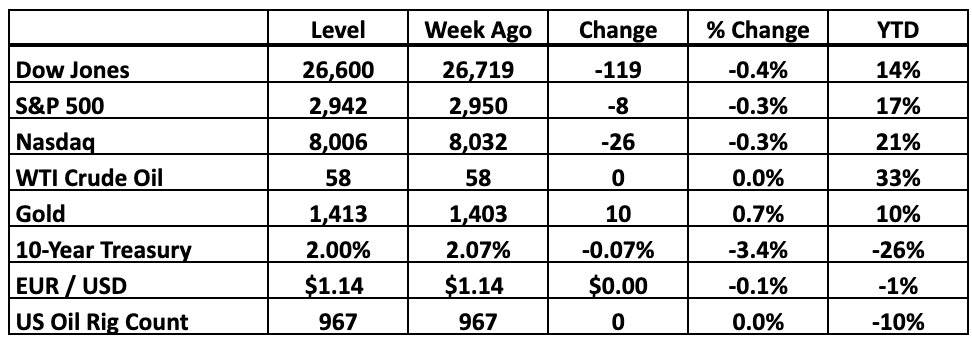

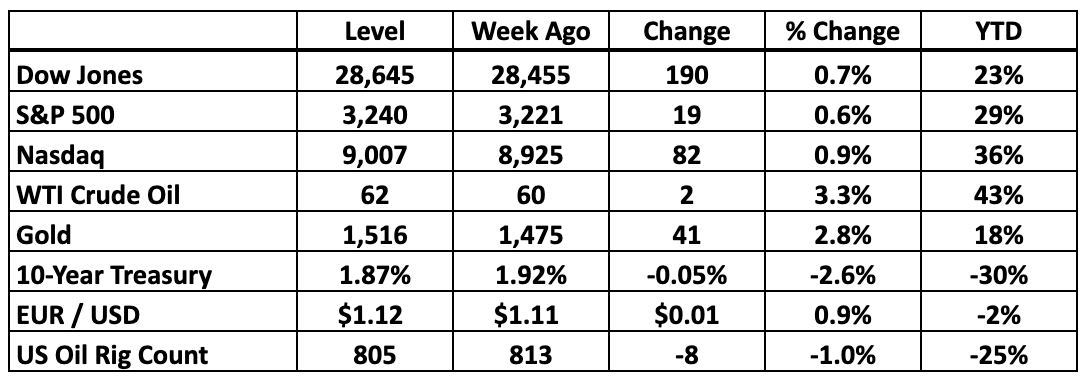

Key Market Indicators

-----------------------------------------------------------------------------

BMR Companies and Commentary

The Big Picture: Animal Spirits In Control

Part of what won Yale economist Robert Shiller the Nobel Prize was his 2005 warning that the housing market was getting unsustainably overheated. Since then, people have come to him to tell the bulls they’ve gone too far. That’s why his recent admission that this record-breaking year on Wall Street is built on irrational factors is so illuminating. Shiller now sees “animal spirits” as the main factor driving what could easily become the best year since the 1950s.

He knows this isn’t logical. And he doesn’t mind. After all, the market isn’t always rational, but when something gets it moving away from the fundamentals, there’s no point in fighting the flow. You’ve simply got to know your own nature. If you aren’t confident enough to run with the bulls, stay on the sidelines and keep cashing 2% Treasury bond coupons. But there’s a lot of money to be made even in a frothy market. Once you let the bulls loose, they’ll run until they’re completely exhausted. Needless to say, we're excited. Even Bob Shiller seems relatively sanguine about how far this rally can continue in 2020 and beyond.

He’s far from alone. Sprawling trillion-dollar asset management complexes are sharing their 2020 outlooks now and they’re convinced bullish conditions will prevail for the foreseeable future. All we need is a mood strong enough to cut through the shocks. Wall Street isn’t climbing a wall of worry any more. We’re riding a wave of exuberance.

It really amounts to market physics. A stock in motion will remain in motion until an obstacle forces a course correction. At this point, there’s nothing big enough looming on the horizon to break the bulls’ stride. We’ve already lived through a year of trade war and earnings deterioration. That’s the status quo now, part of the background noise.

More importantly, it’s already built into the trailing year-over-year comparisons. We don’t need a big external stimulus like tax cuts or even the Fed to get the 2020 numbers going in the right direction. All we need is a little organic growth. That’s been building up behind the scenes as the Fed keeps interest rates low.

Builder confidence is at its highest level since 1999. New home sales are tracking at 2007 levels once again and there’s no ceiling in sight. This is just getting started. And even Bob Shiller, the housing bubble guy himself, has stopped fighting the mood. A year ago, he warned that the housing market reminded him of 2006, right before the crash. Conditions now look hotter than ever.

Shiller says it’s contagious. The impeachment hasn’t stopped it. The trade war hasn’t stopped it. Under normal circumstances, the bulls would have run out of breath by now. But while these aren’t normal circumstances, history shows that they aren’t absolutely unprecedented either. On Shiller’s scale, stocks are “quite high” now at a 30X inflation-adjusted earnings multiple.

Back in 1999, his metrics stretched a full 50% beyond where they are now. History didn’t end. This time around, they can go at least as far before they snap. After all, as Shiller says, we have a motivational speaker in the White House now, someone who loves to talk the market up when everyone else tries to talk it down. That's huge.

-----------------------------------------------------------------------------

Anaplan (PLAN: $53, down 1% last week )

While Anaplan was down a bit over the past week, it has doubled in the past year and BMR subscribers have captured a healthy 42% of that gain after we added it to the Aggressive portfolio back in March. The company still has significant upside since growth prospects for its decision making software remain bright.

At the forefront of “Connected Planning,” a category that it has created and is a part of the cloud computing category, the technology allows companies to make faster, and, it believes better decisions. Anaplan’s technology, which it calls Hyperblock, connects data through various company’s departments rather than centralizing decision making within the finance department. Currently aimed at large enterprises, there is still plenty of room for growth. At the start of 2019, the company had 1,100 customers and only 250 were part of the Global 2000.

Recent results demonstrate the company’s growth prospects. In the fiscal third quarter (ended October 31), Anaplan’s rapid top-line growth continues, with revenue increasing 44%, from $62 million to $89 million. Although the company has a history of expanding losses, management has slowed down the rate of expense growth. For the most recent period, Anaplan’s operating loss narrowed to $32 million compared to third-quarter 2018’s $50 million operating loss. Management boosted its fiscal 2020 guidance, including raising their revenue expectation to a 44% top-line increase ($347 million) versus their prior 42% expectation, up from $240 million in 2019.

BMR Take: With its pristine balance sheet ($50 million in debt and $310 million in cash), this major disrupter still offers exciting growth prospects as large companies continue to adopt its technology, which includes machine learning and other artificial intelligence. Our Target is $75 and our Sell Price is $45 and we would expect the stock to reach new all-time highs above $60 in the first part of 2020.

-----------------------------------------------------------------------------

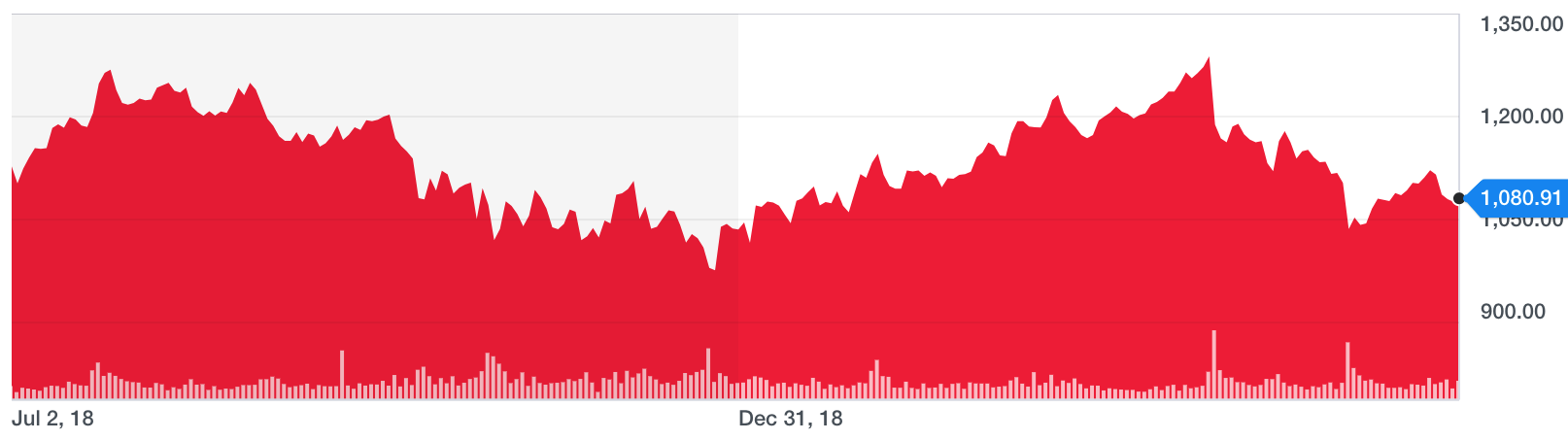

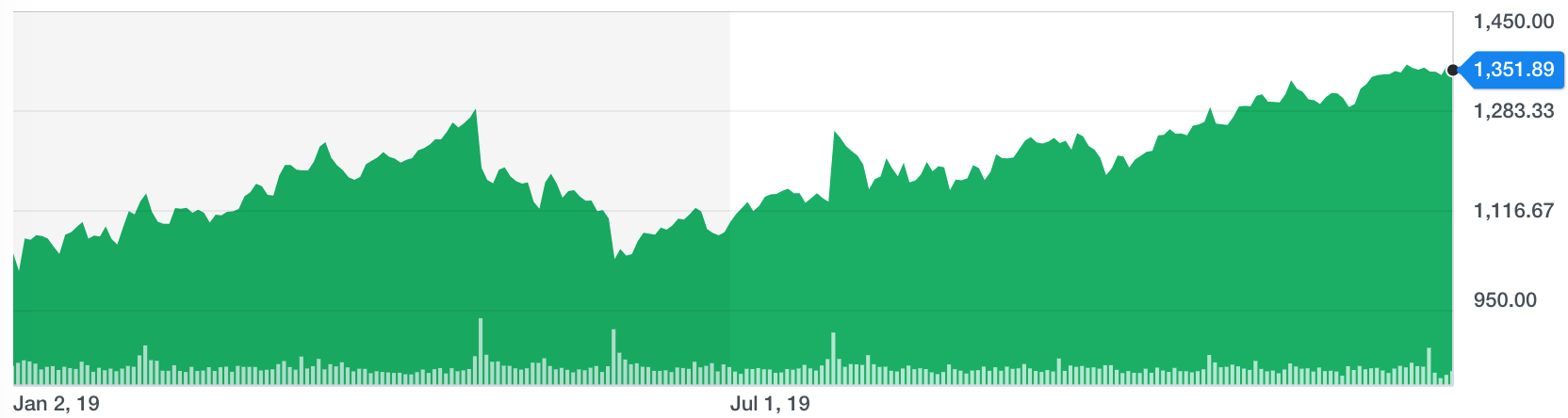

Alphabet (GOOG: $1,352, flat)

The Search giant is up 30% for the year and is within 1% of an all-time record. Not bad for a company with a near-trillion-dollar market cap ($933 billion). The big news recently is that the founders have stepped back and turned over the running of the firm to Sundar Pichai. He’s been running the core Google business since 2015 but this latest promotion gives him a clear line of authority over the entire enterprise.

The search business is solid and obscenely profitable but is not growing terribly fast. Their cloud platform business however rose more than 80% last year, albeit still small at $4.4 billion in revenues. But give this two more years at this growth rate and you have a huge business generating big cash numbers. With revenue tracking near $160 billion in 2019, up from $137 billion in 2018 and $110 billion in 2017, there is nothing but more green ahead for the company.

They are also buying stock back like no tomorrow, with almost $6 billion being spent on shares in just the 3rd quarter. With $120 billion in cash on the books, and generating over $2 billion a month, this type of buying could continue for months if not years into the future. After all, nobody talks about the M-word on the Street, but you have to admit, with 88% of the search market, this company is a monopoly. Is there a risk of the governments of the world getting involved in Google’s business? Yes, of course.

But we think this is highly unlikely and if we didn’t already own stock in the company, we would be happy to acquire shares of this fabulous firm as soon as the market opens for trading on Monday morning. Trading at its all-time high, this concerns us not a bit. After all, why oh why do you think this company is trading at an all-time high? Because it is a cash machine, now and in the future. Our Target is $1450 and our Sell Price is: We would not sell Google.

-----------------------------------------------------------------------------

Twitter (TWTR: $32.50, up 1%)

What do you do when some of your favorites are down 20-50% from their highs? We go back to the basics.

We continue to love Twitter but the stock has been flat for months now, since October when it was trading in the low 40s. But many times the stock doesn’t tell the whole story. Revenues are good, not spectacular, growing from $2.4 billion in 2017 to $3.0 billion in 2018. This year looks like they will hit the $3.5 billion level, with profits of $1.60 per share in 2018 and what looks like $2.40 in 2019. Compared to a lot of other high-tech companies with virtually no earnings, it’s a nice breath of fresh air to see Twitter actually producing profits.

They still have a ton of cash at $5.8 billion, balancing $2.6 billion of debt. The exposure the company gets from our current president and from the world-changing events that it has been involved in (Arab Spring, Hong Kong) we expect good things from the company in the coming 5-10 years. We see the upside much greater than the downside risk. Our Target of $47 is Aggressive for this $25 billion company and our Sell Price of $25 will protect you on the downside.

-----------------------------------------------------------------------------

A Word From Gary Jefferson

Jefferson Financial Group

First Vice-President, Investments

UBS Financial Services, Inc.

After digesting dozens of 2020 forecasts from leading Wall Street firms and other outside resources, we want to give you our take on what WE see for the coming year.

First, we don't expect a bear market or a recession. The economy is doing great and it simply is not going to stop on a dime. The things that matter such as consumer confidence, consumer spending, wages, full employment, low interest rates and inflation are at some of the best levels we have seen in our lifetimes.

And the strong economy, of course, is what has and we believe is what will continue to energize the market in 2020. Just look at GDP. The final Q3 GDP estimate of 2.1% puts 2019's annual growth rate on pace to beat the average annual growth rate since this bull market began. Consumer Sentiment was up as well, rising to 99.3 from last month's 96.8.

Even though we key on earnings, if all one did was monitor the following four items, you could accurately forecast the strength of the economy with uncanny precision: GDP, employment, consumer sentiment and interest rates. All are really, really doing well.

Earnings are expected to slow down the first two quarters, but the positive impact from all of the prior rate cuts should hit bottom lines around the midpoint of next year. We anticipate positive growth in the first two quarters and up to 10% earnings growth across S&P 500 stocks for the full year. Thus, if there is going to be a sell-off or "correction," we expect it might be in January or February, triggered more by political consternation than lowered earnings estimates.

If we don't see a pullback early next year, we may have a period of volatility in the June area as politics heats up again with conventions and selections of final candidates. We expect these downswings, if they occur, will be headline-driven events and will therefore result in "buy-the-dip" opportunities for investors wanting to put extra cash to work.

What worked last year: Technology was the clear outperformer in 2019 while Energy was the largest underperformer. As we move in to 2020, we favor Communication Services and Consumer Discretionary stocks (including Amazon) and are not looking for much from either Technology or Energy. However, if Big Oil bounces back, it will come roaring back . . . in that scenario, we'll add to our coverage there.

Either way, as we view the entirety of the economy, tariffs, politics and the Fed, we believe all major sectors are capable of achieving low double-digit returns in 2020, while Consumer Staples, REITs, Utilities and Financials may still be capable of somewhat lower returns.

What we don't expect is smooth sailing throughout 2020. We expect plenty of volatility because of global trade tensions, Brexit and of course politics right here at home. We don't expect the Fed to raise or lower rates next year, but in case the economy needs a safety net, they will lower rates. Oil prices, of course, have always been a wild card, but we see plenty of supply to keep markets stable. We don't expect the president to be removed from office, but rather expect his pro-business policies (less government, fewer regulations and lower taxes) will continue to foster business growth and entrepreneurism.

As a comparison to what we expect, here is the case made by the Stock Trader's Almanac for 2020:

- Worst Case: Correction but no bear in 2020. Flat to single digit loss for full year due to on-going unresolved trade deals, no improvement in earnings and growth weakens further. Trump is removed from office by the Senate, resigns or does not run and political uncertainty spikes.

- Base Case: Average election year gains. Incumbent victory, trade and growth remain muddled, modest improvement in corporate earnings and Fed stays neutral to accommodative. 5-10% gains for DJIA, S&P 500 and NASDAQ.

- Best Case: Above average gains. Incumbent victory, trade resolved, growth improves, earnings improve and Fed stays neutral and accommodative. 7-12% for DJIA, 12-17% for S&P 500 and 17-25% for NASDAQ.

We lean toward the upside.

-----------------------------------------------------------------------------

The High Yield Investor

As we look toward 2020, most investors have flipped from indulging their grimmest recession fears to a posture closer to our own bullish bias. That's ultimately a good thing. However, it also sets up volatility ahead when expectations get too far ahead of reality, even for a brief period of time. We are looking for good things from the coming year. We just know that the route is going to be far from smooth.

Our top High Yield priority for the coming year is simple: hold defensive positions and wait for money to flow out of these stocks before you expand your holdings. You should have locked in a reasonable quarter-to-quarter income stream to cushion the downswings, so chasing these stocks while yields are relatively low doesn't make a whole lot of strategic sense. The goal is to lock in the highest yields possible, which means waiting until these stocks are out of favor.

It will happen. For now, as long as the rest of the market is rallying, there isn't a whole lot of urgency in building up your defense. And if you're feeling nervous, we suggest capturing the biggest yields you can to offset the impact of negative real interest rates around the world. Remember, the Fed won't raise interest rates again before annual inflation reaches 2%, so locking in anything less for the long term means you're locking in at least a little purchasing power deterioration . . . you are guaranteed to lose money at the end of the road. Who wants that?

Most of our recommendations pay well above 5% and some carry much higher yields as the market pivots from defense to enthusiasm. We'd like to discuss two of our favorites here. The first is ............ AND THIS IS WHERE YOU WILL GET THE BEST VALUE FROM BEING A PAID SUBSCRIBER. GO HERE TO SUBSCRIBE. YOU WILL BE HAPPY YOU DID: www.BullMarket.com/subscribe

Good Investing,

Todd Shaver, Founder and CEO

The Bull Market Report

Since 1998