October 30, 2024

by Todd Shaver | Oct 30, 2024 | Instant News Flash

Shares of biopharmaceuticals giant Eli Lilly (LLY: $830) took a tumble following its third-quarter results this morning, with sales coming in below estimates at $11.4 billion, up 20% YoY, compared to $9.5 billion a year ago. It posted a profit of $1.1 billion, or $1.18 per share, against $100 million, or $0.10, resulting from a $3 billion charge related to an acquired in-process research and development project. Profits during the current year quarter were weighed down by $2.8 billion in charges from acquired in-process research and development. These are the result of its various acquisitions in recent years; without them, the company’s profits would have hit an impressive $3.9 billion. This led the company to lower its outlook for the full year.

The top-line miss was the consequence of lower-than-expected sales of its diabetes and obesity drugs, Mounjaro and Zepbound, at $3.1 billion and $1.3 billion, respectively, roughly flat compared to the prior quarter. Eli’s miss was owing to its inability to meet the demand for its GLP-1 drugs, leading to shortages and empty shelves. We can all agree that consumers not getting enough of Eli’s products is a good problem, especially as the company works to ramp up production, with as much as $18 billion invested in new capacity since 2020.

In the whole scheme of things, this is a $800 billion giant growing at 20% YoY, with a robust drug pipeline and a string of blockbuster products. The market has overreacted here. The low for the day is $769, so you can see that it has bounced back with strength.

Eli Lilly had a strong showing across most other products during the quarter, with Verzanio, its metastatic breast cancer drug, reaching $1.4 billion in sales, up 32% YoY, followed by Taltz for autoimmune diseases at $880 million, up 18% YoY, and Humalog at $530 million, an increase of 35% from the prior year. The only laggards were its type 2 diabetes drugs, Trulicity and Jardiance, down 22% and 2% YoY, respectively.

The company had several pipeline wins during the quarter, with FDA approval for its moderate-to-severe atopic dermatitis drug, Ebglyss, for children and adults 12 years and older. In addition, it won approval in Japan for Kisunla to treat early symptomatic Alzheimer's disease. These drugs are potentially worth multiple billions in sales each year once thoroughly commercialized.

The market for GLP-1 drugs will be worth $100 billion by the end of this decade, and Eli’s products are proven to be more effective than those of Novo Nordisk in this regard. The stock is up 42% YTD, and we firmly believe that buybacks and dividends are right around the corner, given Eli’s growing balance sheet with $3.4 billion in cash, $30 billion in debt, and $4.5 billion in cash flow. The stock hit $770 this morning but has bounced back strongly, with heavy buying from institutions and investors. Our Target is $1100, and We Would Not Sell Lilly. The stock reached $972 just last month. We fully expect to see new highs next year.

February 7, 2024

by Todd Shaver | Feb 7, 2024 | Instant News Flash

Pharmaceuticals giant Eli Lilly (LLY: $730) blew past estimates during its fourth quarter results Monday night after the close, posting $9.4 billion in revenues, up 28% YoY, compared to $7.3 billion a year ago. Profit was $2.2 billion, or $2.49 per share, against $1.9 billion, or $2.09, driven by the strong response to its new anti-obesity drug, Zepbound, coupled with price increases for its blockbuster diabetes treatment, Mounjaro.

For the full year, the company produced $34.1 billion in revenues, up 20% YoY, from $28.5 billion during the same period last year. Profits for the year, however, took a dip, dropping from $7.2 billion, or $7.94 per share, to $5.7 billion, or $6.32. This was largely the result of various in-process research and development charges, most of which were acquired by the company over the past few quarters.

During the quarter, the company’s incretins, or drugs that work by mimicking hormones led the way in terms of growth, with Mounjaro posting sales of $2.2 billion during the quarter, up 700% YoY, followed by its GLP-1 candidate, Zepbound, at $176 million which was just introduced in the quarter. Other key growth drivers include Verzenio, Jardiance, and Tyvyt*, up 42%, 30%, and 98%, respectively. Please re-read the first sentence of this paragraph.

* a medication used to treat Hodgkin's disease

A few detractors included the likes of Trulicity, Humalog, and Alimta, down 14%, 33%, and 81% YoY, respectively. This was largely owing to lower realized prices, coupled with persistent supply constraints in recent months. The lower prices weren’t that surprising, with the company announcing last year that it would be cutting the prices of Humalog, and its other insulin products by as much as 70% going forward

The big story about the company, however, is its new obesity play, Zepbound, which has gained strong momentum within just a few months after its launch, and is already threatening Novo Nordisk’s dominance in this space. Lilly expects demand for this drug to far outstrip supply for 2024, as it grapples to build capacity with a fresh $3 billion commitment to expand manufacturing.

Given the pace at which incretins are expanding within the US and internationally, with the entire market expected to hit $50 billion in 2030, the drug now has 90% insurance coverage and Medicare Part D. Sales are only going to heat up from here, with Morgan Stanley projecting sales for Zepbound for 2024 to be $2.2 billion. As noted above, Zepbound did just $176 million last quarter. Barclays forecasts $7.3 billion in 2024 sales for Wegovy, which as you know is made by Novo Nordisk (NVO).

In addition, Eli Lilly is working to unveil its oral weight loss drug, Orforglipron. This could be very important as all of the weight-loss drugs on the market are injectables. When you can just take a pill, this market will explode.*

* https://www.nejm.org/doi/full/10.1056/NEJMoa2302392 Read this report from September 2023. If this doesn’t get you excited about owning Eli Lilly, there is nothing we can ever say that will do so.

Following a 60% rally in 2023, the stock is already up 20% so far this year, starting at $592 on January 2nd, and is showing no signs of cooling down. The new all-time highs hit by the stock this week and all of this year, are perfectly justified. How can I buy this stock at such a high price, you are asking yourself? Very easy. Think 2025, 2028, 2030. Then sit down at your computer and buy the stock!

In addition to investing in R&D and expanding its productive capacity, Eli Lilly is increasingly generous in returning capital, with its sixth consecutive yearly dividend increase, doubling it since 2018. It ended the quarter with $2.6 billion in cash and $20 billion in debt. Our Target is $665 and we would not sell Eli Lilly. Whoops. We have to raise our Target again. It hit $742 during the day yesterday, and closed at $705, up $37 for the day. If the stock market continues its bull market run this month and on into the spring and summer, we wouldn’t be surprised to see the stock with a 9 in front of it. Our new Target is $825.

February 11, 2018

by Todd Shaver | Feb 11, 2018 | Weekly Newsletter 7pm Sunday

The Weekly Summary

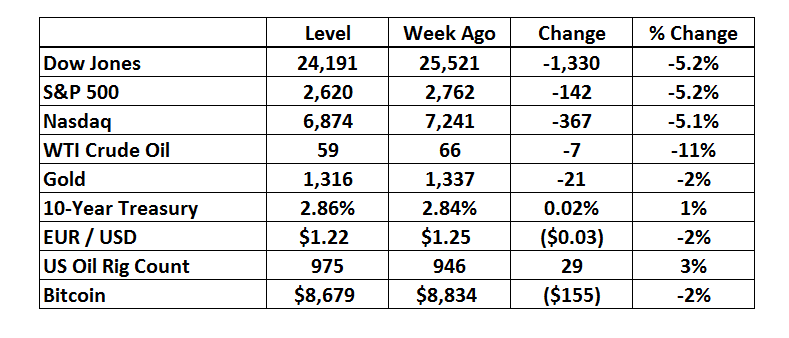

Volatility is back and in an uproar. We’ll run through what is happening in the markets below, but don’t lose sight that although the backdrop warrants caution, the bull market is alive and well. US equities ended their worst week in two years on a positive note with the Dow up 330 points on Friday, but rate-hike fears that pushed markets down remain in place as investors await inflation figures on Wednesday. The S&P 500 tumbled 5.2% in the week, its steepest slide since early 2016, jolting equity markets from an unprecedented stretch of calm. At one point, stocks were 12% below the highs set just two 11 days ago, before a strong rally Friday left the equity benchmark 1.5% higher on the day.

Still, the selloff has wiped out gains for the year. Signs are mounting that jitters spread to other assets, with measures of market unrest pushing higher junk bonds, emerging-market equities and treasuries. The CBOE Volatility Index ended at 29, almost 3x higher than its level January 26th. We at The Bull Market Report are staying calm. We believe stocks are on sale so we would suggest picking out one or two of your favorites and slowly buying more shares.

No matter what is happening out there, there is always a bull market here at The Bull Market Report! This week we highlight: Blackrock, The Carlyle Group, Synaptics, Tesla, CBRE Group, and Ventas.

Key Market Measures (Friday’s Close)

BMR Companies & Commentary

Blackrock (BLK: $522, down 5%)

BlackRock is trusted to manage more money than any other investment firm. Its business is investing on behalf of clients from large institutions, to parents and grandparents, teachers, nurses, doctors and people from all walks of life who entrust their savings to the firm. Well, the company is getting even bigger.

BlackRock is seeking to raise $10 billion for "BlackRock Long-Term Private Capital" to buy and hold $500 million to $2 billion minority stakes in companies for periods of up to more than a decade. The move establishes BlackRock as a potential competitor to Wall Street private-equity giants like Carlyle Group and Apollo Global Management. It is the first-ever attempt by the world's largest asset manager to make such direct investments.

BlackRock has praised Berkshire Hathaway as the best-known example of the strategy. Well, of course. No one has ever done it better. We all know this. BlackRock Long-Term Private Capital will operate differently from most private equity funds, taking full commitments up front and reinvesting as it exits investments. As compared with most investments that return capital to investors after one deal. This is great for Blackrock shareholders because there is no need for ongoing fundraising.

BMR Take: The rock of the investment management industry right now is Blackrock. The company is going to generate nearly $14 billion of revenue this year and produce about $28.60 of EPS. With revenue and EPS growing to over $15 billion and $32.00 next year, respectively, the stock is far from expensive leaving a lot of room for upside.

---------------------------------------------------------------------------------------

The Carlyle Group (CG: $23, down 10%)

Carlyle delivered a solid quarter. Revenue was $1.0 billion versus just $435 million a year ago. EPS hit $1.01 versus just $0.02 a year ago.

Management discussed how the business concluded 2017 with great momentum across all businesses. Carlyle had record activity deploying $22 billion into new investments and raising $43 billion of capital across the platform. Investment performance was exceptional with 20% appreciation across carry funds enabling realizations of $26 billion that went to investors as proceeds for their investments.

The company declared a quarterly distribution of $0.33 per share on February 21st. For full year 2017, they paid out $1.41. That is nearly a 6% yield at the current price.

BMR Take: In private equity The Carlyle Group is a top-notch franchise, known everywhere, the who’s who of business, doing deals in the top floor offices of every major city. The business is raising money like weeds and generating big returns. It is a very compelling opportunity. EPS should hit $3.00 next year leaving this stock dirt cheap.

---------------------------------------------------------------------------------------

Synaptics (SYNA: $44, up 7% - yes really!)

Synaptics reported revenue of $430 million versus $461 million last year. EPS was $1.11 versus $1.49 a year ago. Not terribly pretty, but Synaptics is starting to benefit from the transition encompassing a more diversified product portfolio and customer base, and expects to see strong momentum from investments in infinity displays and consumer IoT in the second half of this calendar year. They continue to make meaningful strides across core growth priorities within chip-on-film, OLED (organic light-emitting diode*), in-display fingerprint technology, and consumer IoT. This includes retail availability of flagship smartphone products, such as new fingerprint, display, and voice-enabled technologies.

* OLED panels are made from organic (carbon based) materials that emit light when electricity is applied through them. Since OLEDs do not require a backlight and filters (unlike LCD displays), they are more efficient, simpler to make, and much thinner - and in fact can be made flexible and even rollable.

BMR Take: With all of the growth investments happening, and the lucrative opportunity emerging for consumer IoT, the quarter’s results were less important than the outlook for attacking this major opportunity. And the outlook is bright. EPS is expected to ramp from around $4 this year to $5 next year and substantially more in the years ahead. We added the stock at $41 in December and our Price Target is $54 and we are hopeful of seeing this during the current year. It would be helpful in achieving this goal if the market calms down and resumes its bull run.

---------------------------------------------------------------------------------------

Tesla (TSLA: $310, down 9%)

Tesla reported revenue of $3.3 billion this quarter versus $2.3 billion last year. For the full year Tesla did $12 billion versus $7 billion a year ago. EPS this quarter was a loss of $3.04.

However, the big ramp in profitability is on the horizon. Revenue is expected to jump to $20 billion this year and $27 billion next year. EPS is expected to swing from a loss to a positive $3.25 in 24 months.

The stock traded about flat after the earnings release that included a fractional revenue miss, and narrower-than-consensus EPS loss. Gross margins came in 190 basis points below consensus, with the Model 3 production ramp weighing on the overall margin profile. But that didn’t really matter as management reiterated its target of 5,000 Model 3 production units per week by the end of Q2.

BMR Take: Most continue to see many moving parts to the Tesla story, with the guidance for sustainable positive operating profits sometime in 2018 garnering more of a show-me attitude, especially given the checkered track record of not hitting guidance milestones or production targets. However, most agree the healthy demand for the Model 3 continues to be a good problem to have, and are spectators on the pace of production execution.

We put a Sell Price of $335 on the stock a few weeks ago so we don’t lose the tremendous profits we have on the stock, but the market this week smashed most stocks down including Tesla. Our Sell Prices are for YOU to decide what to do.

--- We love the concept of the company.

--- We love Elon Musk (Space X with its new successful launch this week has had positive ramifications on Tesla).

--- We love the cars they make.

--- But the debt is crushing.

--- But they have been able to weather the storm through debt and equity sales.

As we’ve said before, this stock could go to $200 or $500. And we’re not sure which will come first? It is very speculative. Should you be in this stock for the wild ride ahead? Only you can decide.

Here’s a 5-year chart. Pretty impressive:

---------------------------------------------------------------------------------------

CBRE Group (CBG: $42, down 5%)

CBRE is crushing it. The company reported revenue of $4.4 billion versus $3.8 billion last year. EPS was $0.99 up from $0.93 a year ago. The consensus expects this year’s revenue to grow from $14.2 billion to $16.5 billion in 2019. EPS is similarly expected to grow from $2.70 this year to $3.20 in 2019.

Fourth-quarter results capped another excellent year for CBRE. Performance significantly exceeded the expectations discussed on the third-quarter earnings call as some concerns surfaced about occupier outsourcing and leasing fee revenue growth. But all that went to the wayside as revenue and earnings for 2017 ended up reaching all-time highs. 2017 marked the 8th consecutive year of double-digit EPS growth for CBRE.

BMR Take: The macro environment is a supportive backdrop for this business, and management continues to operate within an industry poised for long-term growth. This is due to the growing acceptance of outsourced commercial real estate services, the increasing capital allocation to commercial real estate as an institutional asset class, and the continuing consolidation of activity within the industry to the highest-quality, globally diversified market leaders. CBRE Group is a must-own holding in your portfolio in the real estate sector.

We’re up over 60% in two years on this wonderful firm. No dividend yet, but we can see that coming. Our target is $54 and there’s an outside chance it can hit that this year. We know what this company does first hand – they save big multi-national companies money. Big money as in millions and millions of dollars. And the firm gets rewarded in brokerage fees, fixed fees and more. And so few people know about this great firm.

This chart shows the value this stock offers here, after this rough week:

---------------------------------------------------------------------------------------

Ventas (VTR: $52, down 5%)

Ventas reported revenue for the quarter of $895 million versus $875 million a year ago. Revenue for 2017 ended at $3.6 billion versus $3.4 billion in 2016. EPS was $0.50 versus $0.58 a year ago. EPS for 2017 ended at $1.78 versus $1.86 in 2016. Consensus expects revenue to drift upward toward $3.7 billion over the next 2 years. EPS is expected remain stable around $1.75 although we see several sources of EPS upside that are likely to drive revisions closer to the highest Street forecast of $2.15.

All in all, 2017 was another excellent year for Ventas, as the business generated record cash flow from operations and delivered same-store property cash net operating income growth at the high end of internal expectations. To further enhance their diverse portfolio, the company made nearly $2 billion in value-creating investments, including significant expansion of their university-based life science business. And they profitably disposed of almost $1 billion in assets and completed innovative deals with leading operating partners.

BMR Take: Ventas has proven resilient through cycles for two decades. They remain one of the world's best REITs with a specialty in healthcare among other areas.

This success is founded on solid strategic vision, superior foresight and innovation, intelligent and timely capital allocation decisions, rigorous execution and a cohesive, expert team. As they enter 2018 – the company’s 20th anniversary year – management is confident that they can continue the long track record of superior consistent performance as the industry leader.

We added Ventas at $60 in last 2016, a little over a year ago. Until the last two weeks, it was hovering around $56, down a bit, but still paying a nice 6% dividend. It’s worth $18 billion, and has over 1200 properties across the US, Canada and the UK. And as you know, they are in the senior living business along with medical facilities as well. Yes, the stock is down, but this company is strong, and we can only see good things happening from here. If you bought at $60 now is the time to add to your position to bring your cost down. Two years from now we wouldn’t be surprised to see the stock in the 70s, as remember, 10,000 people a day turn 65 in the US. They have to live somewhere!

---------------------------------------------------------------------------------------

We got a letter from one of our readers about Ventas

From: Richard Reed [mailto:reed995@]

Sent: Wednesday, February 07, 2018 10:21 AM

To: The Bull Market Report <Info@bullmarket.com>

Subject: Re: EARNINGS PREVIEW FOR THE WEEK AHEAD

Hi Todd,

Ventas (VTR) is below your Sell Price. Are you lowering the sell price? Thanks.

Richard

Our answer:

Hi Richard –

Look – they own 1200 assets in the United States, Canada and the UK. The properties are senior living properties and more. Are they all going down the tubes? NO WAY. A $19 billion asset paying 6%. We would buy more.

Furthermore, our Sell Price on Ventas is $58. But at $52, we have to say that we like it even more. Nothing has changed for the company in the past two weeks. Yes, interest rates are a shade higher, but nothing out of the ordinary. When the economy is good, rates go out. This is just normal. So to answer your question above, yes, we are lowering our Sell Price to $48. Of course, YOU can make up your own mind on this one, as always, but we would take this opportunity to buy an amazing company at an even lower price.

---------------------------------------------------------------------------------------

---------------------------------------------------------------------------------------

Economic Calendar

CPI Ex-Food & Energy

Wednesday, February 14th, 8:30 AM

Period: January

Consensus: 1.7%

Prior: 1.8%

CPI

Wednesday, February 14th, 8:30 AM

Period: January

Consensus: 1.9%

Prior: 2.1%

PPI

Thursday, February 15th, 8:30 AM

Period: January

Consensus: 2.5%

Prior: 2.6%

Housing Starts

Friday, February 16th, 8:30 AM

Period: January

Consensus: 3.7%

Prior: -8.2%

---------------------------------------------------------------------------------------

---------------------------------------------------------------------------------------

Apple has $285 Billion in Cash

Can you believe this? Again – a record high for any company in history. Apple (AAPL: $156, flat for the week) has $285 billion in cash, or $56 a share. With the stock at $156, that’s 36% of each share of stock in cash. We’re not sure of the Wall St. record, but we are guessing this is twice as much than any other company in history. With the stock flat for the week (amazing) this just screams out at us to add more to the portfolio.

---------------------------------------------------------------------------------------

If the Market Heads Back Up

No one knows where the market is heading. Will it calm down and move higher this coming week and month? Or will it be heading for 23,000 and lower? Again, we don’t know. But if things simmer down and the volatility abates – AND IT WILL – there are a few stocks that we would want to add to our positions in. Here are just a few:

Microsoft

PayPal

Google

Facebook

Apple

Eli Lilly

Yes, many of these are the super Tech stocks that have been leading the market. But guess what? These stocks will continue to lead the market for many years to come.

And one more note. Did you see Annaly Capital Mortgage (NLY: $10.21, down 1%) this week? Solid as a rock. So if you are super worried about things, we believe Annaly can be a store of value for a month or two or 12, and you can enjoy the 11% dividend in this $12 billion market cap company.

---------------------------------------------------------------------------------------

---------------------------------------------------------------------------------------

A Word from Gary Jefferson

Jefferson Financial Group

First Vice-President, Investments

UBS Financial Services, Inc.

There was no comment Monday or Tuesday because everything I wrote was outdated and the numbers were obsolete within minutes of writing, rewriting and re-rewriting them. The dust may or may not have settled, but a few things are much clearer today.

In short, the seismic swings over the past few days have been based on three primary factors that we believe now form a consensus:

1. The threat of higher inflation (Rising bond yields)

2. The possibility of more Fed hikes

3. The long streak without a normal and healthy market shakeout.

How does that stack up against the best economy we've seen in over a decade? In other words, is it good news or bad news that economic growth is so strong the Fed may have to raise rates sooner than expected? Or, is it good news or bad news that nearly half the companies in the S&P 500 have reported fourth quarter results and more than 80% of them have beaten Wall Street's revenue expectations, the highest percentage since the third quarter of 2008? And, is it good news or bad news that the tax law will boost those profits further in the quarters ahead?

Let's put all this in perspective:

First, the market isn’t overbought anymore. We now know that. There was a "10% correction." Let’s get over it.

Second, earnings are robust.

Third, the rise in bond yields has been a headwind, but it’s not signaling a looming recession. Importantly, the 10-year vs. 2-year Treasury yield spread has widened out as yields have risen, implying the bond market is now discounting higher inflation and better economic growth, which over the medium term has almost always been positive for stocks.

While volatility has returned with a vengeance, the market fundamentals are now better and earnings growth prospects haven't looked better in years. Basically, all of the reasons why investors have been bullish on the market last week, last month and last year are still here.

---------------------------------------------------------------------------------------

The High Yield Report

by Michael Foster

VP High Yield

It should always be emphasized that much of a stock's action is not caused by only the underlying company, but also by the industry and the overall market. In a volatile environment, this emphasis is especially important. While our High Yield and REIT portfolios have shown lackluster performance over the past two weeks, the fundamental aspects of the companies that make up the portfolios have not changed.

The S&P 500 decreased 5.1% over the past week, leading to stocks officially being in correction territory. Much of the decline is being attributed to interest rate and liquidity fears, which is why much of the analysis on the portfolio below will focus on those aspects. It takes just one week to rattle bullish sentiment. As an investor, you should not put too much weight on what the general financial media is discussing. What should take priority is thinking about whether the fundamental aspects of the economy and market have changed. When this is the priority, our fear diminishes as we realize that earnings are still strong, nonfarm payrolls on February 2nd were above expectations, and a deregulatory environment is still present.

One metric, the yield curve, is worth looking at though. The spread between the 10-year Treasury yield and the 2-year Treasury yield has been constantly decreasing as a result of the Federal Reserve tightening policies and the lack of inflation. On a basic level, you can note that the presence of an inverted yield curve, if it were to happen, has been a common predictor of past recessions. Going deeper, the economic repercussions of the inversion are much more important. Consumers and banks are directly impacted. For consumers, the cost of credit increases, which leads to a larger portion of expendable income being dedicated to servicing debt. For banks, the spread between long-dated loans and deposits decreases, which leads to worse financial performance. We’re sharing this information so that you can keep the yield curve on your radar, but there’s no need to worry as of now. When the curve inverted in the past, it still took between 7 to 24 months to reach any sort of recessionary state.

AllianzGI Equity & Convertible Income Fund (NIE: $20.59, down 4%) fared slightly better than the S&P’s drop of over 5%. It moved from the weekly low of $19.50 to its current level after recovering about 2.5% in the last hour of trading on Friday. The performance of individual equities which it holds, including Microsoft, Alphabet, and Amazon, led to the recovery in the last hour. Given that the fund invests little in the bonds and the scenario of the inverted yield curve, we can expect the funds to be shifted from Equity to Bonds.

We still see Apollo Commercial RE Finance (ARI: $17.70, down 3%) as a cyclical play on the U.S. commercial real estate sector. Given that commercial real estate in the U.S. remains solid, with Apollo’s loan originations hitting $1.5 billion YTD and the economy of the US continuing to get stronger and stronger, Apollo is not a position to be worried about.

Digital Realty Trust (DLR: $102, down 5%) dropped almost by the same amount as the S&P. This was the opposite of the week prior, where the company maintained strength in the midst of widespread declines. While we noted the continued demand for data centers in the last summary, there are some other metrics to note. Digital Realty, owning many data centers in US and internationally, is affected by rising interest rates as the cost of borrowing rises. The company has a massive debt level of $5.8 billion with a Debt/EBITDA ratio of 22. Rising interest rates could cripple the company’s dividend payout and future prospects.

Invesco Municipal Trust (VKQ: $11.83, flat) ended up at the same level as the beginning of the week. With its investments primarily in investment grade U.S. municipal bond obligations (85%), the fund can expect to yield better returns amidst the current rising interest rates scenario. Also, a Fitch report stating that plans to cut federal funds to them won't impact the revenues of the municipal bond funds and ETFs, played a large part in keeping the fund’s price level stable. Nuveen Municipal (NVG: $14.43, flat), another high yield fund with major investments in U.S. investment grade municipal bonds, also maintained its price level.

Pimco Dynamic Fund (PDI: $30, down 1%) was less volatile. The firm, investing primarily in a range of debt securities, including mortgage-backed securities, high yield corporates, and emerging market bonds, could witness further issues with rising interest rates, changes in tax structure, and better yields.

The REIT sector has been partially impacted by the recent economic data, heightening fears of higher interest rates. Primarily, the sector is engaged in massive borrowings, and rising interest rates could increase the cost of the borrowings. With that said, rising interest rates often occur in a booming economy, which indicates higher demand by consumers.

Market corrections generally provide prudent investors with great buying opportunities. One way of going about this is finding relative strength in strong industries. Applying this analysis to REITs, the overall REIT sector was down only 3%. Within out portfolio, three of the five positions outperformed the sector. Annaly Capital Management (NLY: $10.21, down 1%), Government Properties (GOV: $16.37, down 1%), and Omega Healthcare Investors (OHI: $26, flat) composed that group.

As a company that primarily engages in buying mortgages and mortgage-backed securities (as well as other assets), Annaly could fare very well as interest rates go up and correspondingly coupon rates do as well. While this is not necessarily the reason for the less-than-average drop this week, going forward it is something we will keep in mind. Both Government Properties and Omega should not feel a significantly negative impact by rising rates either. The former gets offered attractive rates by the government as a result of its leases and the latter’s healthcare-related real estate is, for the most part, unaffected by the business cycles.

The other two positions, Ventas (VTR: $52, down 5%) and Welltower (HCN: $55, down 5%), ended up having declines that were in-line with the S&P 500 but larger than the move in the REIT sector.

Ventas reported positive 4th quarter earnings on Friday, which provided a minor boost to the stock. The reported income from continuing operations for 2017, $640,000, was a record for the company. In turn, the EPS and FFO per share numbers were also records. In a rising rate environment, this is a positive sign. With the earnings report occurring during a stock market decline, any overall S&P bounce should result in outperformance by Ventas.

The other relatively weak company, Welltower, did not have any news this week to explain the larger than average decline in the stock. As it is focused on owning senior living properties and funding real estate infrastructure, the large amount of debt maintained could pose an issue within the rising rate environment. Currently, though, the extensive track record of stock appreciation over the past 25 years leaves us unworried. Welltower is also at the lower end of its range for the past four years, so it is a good area to pick up more shares.

Good Investing,

Todd Shaver, Founder and CEO

The Bull Market Report

Since 1998

January 30, 2018

by Todd Shaver | Jan 30, 2018 | Earnings Preview 12 PM

Equity Residential (EQR: $61)

Bull Market Report Target Price: $85

Bull Market Report Sell Price: $55

Earnings Date: Tuesday, After market close

Consensus: 4Q17

Revenues: $625 million

EPS: $0.36

Year Ago Quarter Results

Revenues: $605 million

EPS: $0.75

Key Things to Watch For in the Quarter

Analysts expect Equity Residential to report a 3% increase in revenues with a 50% decrease in earnings per share. Despite having beat estimates in each of the past four quarters, the stock is only trading 2% above its price this time last year. Nearly all of the stock’s 15% gains for the year have been wiped out since November with the oversupply issues in the real estate market. We believe the stock is oversold at its current levels, and will see support in the $60 range.

---------------------------------------------------------------------

Eli Lilly (LLY: $86)

Bull Market Report Target Price: $96

Bull Market Report Sell Price: $82

Earnings Date: Wednesday, 9:00 AM ET

Consensus: 4Q17

Revenues: $6.0 billion

EPS: $1.07

Year Ago Quarter Results

Revenues: $5.8 billion

EPS: $0.95

Key Things to Watch For in the Quarter

Eli Lilly is expected to report a 3% increase in revenues and a 13% increase in earnings per share for 4Q17. The stock has beat estimates in three of the past four quarters, and is currently trading 17% above its price levels from this time last year. The stock saw a bit of resistance at $86 earlier this year, and it had recently broken through, but with the tough market of the last two days, the stock is back to $86. This pharmaceutical company invests heavily in its research and development, which will drive its future sales and earnings growth.

---------------------------------------------------------------------

Facebook (FB: $186)

Bull Market Report Target Price: $190

Bull Market Report Sell Price: $155

Earnings Date: Wednesday, 5:00 PM ET

Consensus: 4Q17

Revenues: $12.5 billion

EPS: $1.95

Year Ago Quarter Results

Revenues: $8.8 billion

EPS: $1.41

Key Things to Watch For in the Quarter

Analysts expect Facebook to report a 42% increase in revenues and a 38% increase in earnings per share for 4Q17. Facebook has beaten estimates in three of the past four quarters which has been reflected in the stock’s 42% appreciation over the past year. Facebook’s growth over the past years has been unprecedented for a company of its size. It truly is adhering to its mission of creating a more connected world. We look forward to seeing what kind of developments CEO Mark Zuckerberg has in store for the connected world in 2018. We know it will be good.

---------------------------------------------------------------------

PayPal Holdings (PYPL: $83)

Bull Market Report Target Price: $87

Bull Market Report Sell Price: We would not sell PayPal

Earnings Date: Wednesday, 5:00 PM ET

Consensus: 4Q17

Revenues: $3.6 billion

EPS: $0.52

Year Ago Quarter Results

Revenues: $3.0 billion

EPS: $0.42

Key Things to Watch For in the Quarter

We are looking for a 20% increase in its sales and a 24% increase in its earnings per share for the 4th quarter of 2017. The stock has been on a tear since last year, returning investors a 110% capital appreciation since this time last year. The stock has gone nowhere but up since posting earnings that have exceeded expectations in the past four quarters. PayPal’s market cap is just over $100 billion, making it the largest publicly traded electronic payments company in the world. We look forward to seeing what PayPal has to offer as they continue to lead this growing industry.

---------------------------------------------------------------------

Microsoft (MSFT: $93)

Bull Market Report Target Price: $92

Bull Market Report Sell Price: We would not sell Microsoft

Earnings Date: Wednesday, 5:30 PM ET

Consensus: 2Q18

Revenues: $28 billion

EPS: $0.86

Year Ago Quarter Results

Revenues: $26 billion

EPS: $0.80

Key Things to Watch For in the Quarter

Microsoft is expected to report an 8% increase in revenues and a 7.5% increase in earnings per share for 2Q18. Microsoft’s ability to beat analyst estimates has been reflected in the stock’s 44% increase over the past year. The firm continues to produce high quality hardware and software, and has a very good understanding of their customer base. Microsoft also allocates an incredible amount of capital to research and development, with its most recent announcement being a push into quantum computing, which some say could be similar to the internet revolution in the 1990s.

---------------------------------------------------------------------

Blackstone Group (BX: $36)

Bull Market Report Target Price: $36

Bull Market Report Sell Price: $31

Earnings Date: Thursday, 11:00 AM ET

Consensus: 4Q17

Revenues: $3.3 billion

EPS: $6.43

Year Ago Quarter Results

Revenues: $2.8 billion

EPS: $5.25

Key Things to Watch For in the Quarter

Blackstone is expected to report an 18% increase in revenue along with a 22% increase in its earnings per share for 4Q17. Blackstone has exceeded analyst estimates in three of the past four quarters, and has seen its stock appreciate 17% over the past year. Technically speaking, the stock has underperformed both the market and the sector, and we believe this is a huge mispricing by the market. Blackstone currently trades at a PE of 15 and yields 5%. At these price levels the stock looks like a steal compared to its competitors.

---------------------------------------------------------------------

United Parcel Service (UPS: $129)

Bull Market Report Target Price: $125

Bull Market Report Sell Price: $106

Earnings Date: Thursday, Exact Time not Available

Consensus: 4Q17

Revenues: $18 billion

EPS: $1.66

Year Ago Quarter Results

Revenues: $17 billion

EPS: $1.63

Key Things to Watch For in the Quarter

Analysts expect UPS to report a 6% increase in revenues and a 2% increase in earnings per share for 4Q17. Despite beating estimates in three of the past four quarters, the stock has slightly underperformed the overall market. The stock has appreciated 24% since this time last year, and we expect to see similar returns moving forward as the demand for logistical services increases. Although we remain bullish on the stock, we are keeping a close eye on Amazon as it begins to roll out its own logistics services, posing a potential threat to UPS.

The stock has passed our Target of $125, and we believe the stock will go higher, as long as the market holds here and moves higher in the coming months. We hereby raise our Target to $142 and our Sell Price to $118.

---------------------------------------------------------------------

Alphabet (GOOG: $1,170)

Bull Market Report Target Price: $1,450

Bull Market Report Sell Price: We would not sell Google

Earnings Date: Thursday, 4:30 PM ET

Consensus: 4Q17

Revenues: $32 billion

EPS: $10.00

Year Ago Quarter Results

Revenues: $26 billion

EPS: $9.36

Key Things to Watch For in the Quarter

We are looking for a 31% increase in revenues and a 7% increase in earnings per share for 1Q18. The company has beaten estimates in three of the past four quarters, which has been reflected in the stock’s 45% appreciation since this time last year. The stock currently boasts a market cap of $815 billion, making it one of the largest publicly traded companies in the world. Although Alphabet is best known for its Google Search Engine, the company touches all aspects of technology from cloud computing to its most recent Television Streaming service through YouTube.

---------------------------------------------------------------------

Apple (AAPL: $165)

Bull Market Report Target Price: $194

Bull Market Report Sell Price: We would not sell Apple

Earnings Date: Thursday, 5:00 PM ET

Consensus: 1Q18

Revenues: $87 billion

EPS: $3.81

Year Ago Quarter Results

Revenues: $78 billion

EPS: $3.36

Key Things to Watch For in the Quarter

We expect to see a 13% increase in earnings per share along with an 11% increase in sales for 1Q18, despite less than ideal results with the release of the iPhone X. The stock has beaten estimates in each of the past four quarters, and has appreciated 38% since this time last year. We also saw Warren Buffet add more stock to his portfolio, which should definitely not be overlooked. We expect to see growth in iPhone and iPad sale over the next year, and remain bullish on the stock. The cash repatriation should begin soon and that will produce some changes – in the dividend and in their outlook on buying new technology firms.

---------------------------------------------------------------------

Visa (V: $123)

Bull Market Report Target Price: $123

Bull Market Report Sell Price: We would not sell Visa

Earnings Date: Thursday, 5:30 PM ET

Consensus: 1Q18

Revenues: $4.8 billion

EPS: $0.99

Year Ago Quarter Results

Revenues: $4.4 billion

EPS: $0.86

Key Things to Watch For in the Quarter

Visa is expected to report a 9% increase in revenues and a 15% increase in earnings per share for 1Q18. Visa has beaten estimates in each of the past four quarters, and seen a 50% appreciation in its stock since this time last year. Despite paying a relatively small dividend, the stock still trades at a PE of 44, suggesting it is fairly valued compared to its competitors. We are confident in Visa’s ability to drive earnings growth through the new year. This $280 billion market cap company is a long term hold.

---------------------------------------------------------------------

Amazon (AMZN: $1,420)

Bull Market Report Target Price: $1,500

Bull Market Report Sell Price: $1,225

Earnings Date: Thursday, 5:30 PM ET

Consensus: 4Q17

Revenues: $60 billion

EPS: $1.84

Year Ago Quarter Results

Revenues: $44 billion

EPS: $1.54

Key Things to Watch For in the Quarter

Analysts expect Amazon to report a 36% increase in revenues and a 19% increase in earnings per share for 4Q17. Despite having only beaten estimates in three of the past four quarters, the stock currently trades 70% higher than its levels this time last year. Amazon continues to lead the charge in the online retail space, and we firmly believe in the longevity of the firm. Although the company trades at a very high PE of 350, we believe this is explained by the company’s inherent ability dominate and revolutionize the Retail industry.

---------------------------------------------------------------------

AstraZeneca (AZN: $36)

Bull Market Report Target Price: $42

Bull Market Report Sell Price: $32

Earnings Date: Friday, exact time not available

Consensus: 4Q17

Revenues: $5.4 billion

EPS: $0.45

Year Ago Quarter Results

Revenues: $5.6 billion

EPS: $0.61

Key Things to Watch For in the Quarter

AstraZeneca is expected to report a 4% decrease in revenues and a 26% decrease in earnings per share for 4Q17. Despite the lack of top line growth, the stock has still managed to beat analyst estimates in each of the past four quarters, and has shown 30% year-over-year appreciation as a result. The stock currently trades at a PE of 26, which is relatively cheap compared to other firms in healthcare which average around 40. The stock pays a 4% dividend, and has room to grow in 2018.

We’re not liking this new development with a slowdown in revenues and earnings and are re-evaluating our take on this stock. More to come this weekend. In the meantime, we are moving our Sell Price to $34.

January 14, 2018

by Todd Shaver | Jan 14, 2018 | Weekly Newsletter 7pm Sunday

The Weekly Summary

Everybody has an opinion. Go search the internet and you’ll hear one fellow say the market is going to crumble, the next person say new highs are on the horizon, and the third individual tell you something that doesn’t make sense because they don’t even know what they are talking about. Accordingly, we feel the need to break it all down this week. No fluff. No spin. No wild opinions. Just a little ‘telling it like it is’ as a reminder that this The Bull Market Report. We aren’t like what you see on TV. And we aren’t like what you read elsewhere. We are just like you. Looking for the cold hard honest facts.

US equities ended the week higher in a quiet Friday of trading. Cyclical and value plays were among the better performers. The equity market is already up over 3% this year with some of our stocks like Amazon and Nutanix up more. Bonds are down this year and Treasuries were mostly weaker as investors realize the Fed is serious about raising rates. We saw more flattening of the yield curve indicating caution. In fact, the two-year T-note rose and hit 2.0% for the first time since 2008. Gold was higher for fifth straight week. Crude ended higher for the fourth straight week.

No matter what is happening out there, there is always a bull market here at The Bull Market Report! This week we highlight: Cloudera, Blackstone, Amazon, Google, Eli Lilly, and Home Depot.

BMR Companies & Commentary

Cloudera (CLDR: $18.14, up 5%)

Cloudera met with investors this week at Citi’s Global TMT West Conference. The CEO discussed all that they are doing in terms of new technology. Let’s recap. Remember, understanding the big picture of what the company is doing is how you build real confidence in your investments.

First it is important to understand the backdrop of why Cloudera is such an exciting company. Everything right now is going through a major technological revolution. Look what is happening in cars, health, and virtual reality. Everything is getting connected. This newly-created connected world is creating a backdrop for data that is unprecedented. And in this area of the economy is where the world’s most valuable companies reside—Apple, Google, Facebook, and Amazon. They are all data driven. Economists say the world’s most valuable resource is now no longer oil, but data.

So where does Cloudera fit it? Cloudera helps enterprises enter this new world of machine learnings and artificial intelligence. Cloudera gives them access to this data to transform their business to become data dependent. The old days of just working with a database storage provider and some simple analytics are gone. Today, companies turn to Cloudera to build best-in-class artificial intelligence solutions that optimize all the available data out there, not just their own.

BMR Take: Machine learning and artificial intelligence are megatrends for the next 5 years. Get involved. Cloudera is a great opportunity. Revenue will explode from $360 million this year to $570 million in 2 years. We see Cloudera breaking the $1 billion revenue mark possibly as early as 2020. We added the stock at $22 in June so it has certainly been an underperformer for us. But we are very confident in the success of this company and continue to have a $28 price target on the stock. Sometimes one has to be patient to see the big gains that we expect. Cloudera is still tiny with a market cap of $2.5 billion. But they are growing 40% a year. We would expect to see this little gem grow to the $10 billion level at some point and then get plucked up by one of the big boys. And this might even happen sooner than you think.

------------------------------------------------------------------------------

Blackstone (BX: $35, up 7%)

Blackstone is on a roll and caught an upgrade from JP Morgan. We love it when the professionals come around to our side of the table!

The reason to be excited at this point is that there is going to be a major fundraising cycle for Blackstone over the next two years. The company is expected to raise over $200 billion. The way the company makes money is through these massive fundraisings, then deploying the capital, and then getting a share in the profits from the investments.

The fundraising will happen in two funds. The first is Flagship Real Estate BREP-IX in 2018. The second is Flagship Private Equity BCP-VII in 2019.

BMR Take: Blackstone has been an underperformer relative to its peer group. And the peer group of these private equity companies hasn’t done too well. The entire space is relatively new to the public equity markets. Retail investors just don’t have the comfort level they have with other financials like AIG or JP Morgan. But we think that will all change. These companies print money. Blackstone will do over $3.00 of EPS in 2018. The stock is very inexpensive right now.

We’re up 30% on the stock since we added it in early 2016. Good but not great. The dividend has helped though, as that 5% a year adds up. But we expect more from this great company. Our Target was just reached this week, so we are going to go out on a limb and raise the Target to $42. If things go right, we would expect to see this by year end, but perhaps sooner.

------------------------------------------------------------------------------

Amazon (AMZN: $1,305, up 6%)

Amazon Fresh prices are up to 20% cheaper than major UK supermarkets.

Look out! We are going to see Amazon really shake-up the grocery market this year. Amazon's online grocery service Amazon Fresh is selling some products up to 19% cheaper than major supermarkets, new research suggests.

Amazon Fresh is a subsidiary of the Amazon.com. It is a grocery delivery service currently available in some U.S. states, London, Tokyo, Berlin, Hamburg and Munich. It will also launch in Australia soon.

The cost of a shopping cart from Amazon Fresh turned out to be 11% cheaper than the same online shopping from Tesco, and up to 19% cheaper than other competitors. The study was done by the consulting firm Oliver Wyman. The geography was in London.

Amazon Fresh is still relatively small but the internet giant has very serious ambitions in the grocery sector, suggesting that it may be looking at more acquisitions.

BMR Take: Amazon is a never-ending innovation machine; essentially a massive start-up. Look, the company will do $177 billion of revenue this year and we could rant and rave about the revenue growth outlook. But nobody knows what businesses Amazon will even be in over the next 3 years. They are knocking down doors and running through walls into new markets. Grocery will be tens of billions of dollars for Amazon in a market that the firm has been in for less than a year.

The stock had a banner week and hit our $1300 Target, setting a new all-time high. We believe we will see $2,000 someday in the future, but obviously not right away. But we can see $1,500 in the not-too-distant future, so we hereby raise our target to that level. The Sell Price is raised from $1,030 to $ 1,225.

------------------------------------------------------------------------------

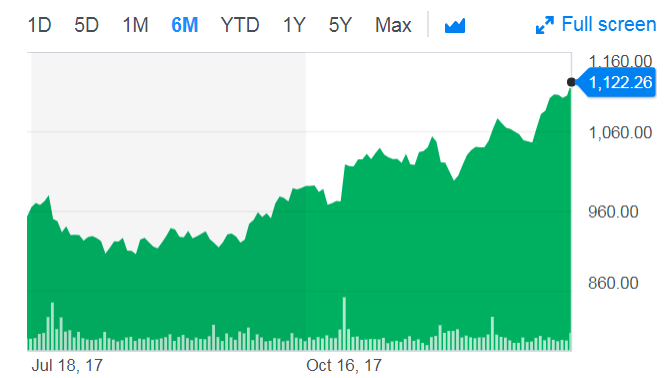

Google (GOOG: $1,122, up 2%)

Apple came under massive scrutiny this week. Parental oversight organizations said Apple should take more responsibility over how children use their devices in particular addition to the technology. We think Apple, Google, and Facebook in particular are making so much money they are likely to be the target of increased scrutiny by governmental authorities. In fact, we saw this week similar outcries against Google. We keep an eye on this risk but would not let it shake us out of any of these holdings.

Google has been profiting from a practice in the United Kingdom but banned in the US, in which brokers secretly reap millions of pounds from addicts seeking treatment in the UK. An undercover investigation by the Sunday Times has discovered a large fraud in this area. As a result of an in-house investigation, Google pulled all addiction-industry-related advertisements from its UK platforms.

BMR Take: Without question, Google and its peers will have to invest more in meeting social responsibilities and being a good corporate citizen. That said, Google can manage through this. We are looking at EPS going from $32 this year to nearly $60 by 2020. We can live without $1 or $2 of EPS if the company addresses these social issues and spends money to prevent thing like this advertising scheme being run through the platform in the UK. In fact, we encourage it, as it could result in a premium valuation.

Google set a new all-time high this week and is now worth $780 billion, closing in on Apple at $900 billion. (Of course, Apple set a new all-time high this week as well, so it’s certainly a good race!) Our Target has been $11,00 which was hit this week, and we expect a continued strong stock market which should proper Google higher. Thus, we hereby raise our Target to $1,450 and our Sell Price to $1,010.

Don’t like high-priced stocks? GET OVER IT. Buy some Google. Buy some Amazon. Buy 7 shares. Buy 23 shares. Just own these fabulous companies!

------------------------------------------------------------------------------

Eli Lilly (LLY: $87, flat)

Eli Lilly caught a big upgrade from Argus Research. Again, we love it when the professionals come around to liking our holdings!

What’s the excitement? Tax reform is a major positive for the company. Additionally, the company is working to sell its Animal Health business. The combination of these two events will create a cash windfall. Now the CEO is talking about doing a large acquisition.

Previously, big time M&A was just a distraction for the company as Lilly could not be competitive due to its balance sheet. However, now there is some real interest to move bigger into immune-oncology. Could we see them try to buy Bristol-Myers? (BMY: $63) Maybe; but that’s a big bite to chew off – around $120 billion.

BMR Take: Lilly is going to do $4.65 of EPS in 2018. They have $4.5 billion of cash. They have more cash than debt. They could do a mega-deal and this could get really exciting. We see why Argus upgraded the stock with a $115 price target.

We at The Bull Market Report have a Price Target of $88 on the stock at the moment, but we expect mid-90s by summer, so we hereby raise our Target to $96. Our Sell Price moves higher too, from $76 to $82.

------------------------------------------------------------------------------

Home Depot (HD: $196, up 2%)

To be honest, we are frankly a bit upset at Home Depot right now. We expect a lot from our companies - we wouldn’t recommend them to you otherwise. Home Depot put out this official statement on tax reform back in November, “The Home Depot is very supportive of tax reform that would fuel the economy by putting more money in the majority of Americans' pockets while improving the competitive position of companies so they can create more jobs. We applaud Congress for its efforts in moving tax reform forward.”

What is it missing?

Where is the minimum wage hike? Where is the $1,000+ bonus to employees. Walmart, some big banks, and many other companies took additional actions. All Home Depot did was issue a press release of encouragement.

We will get over it. But Home Depot missed an opportunity to demonstrate its corporate leadership in this country.

BMR Take: Home Depot is going to do nearly $9 of EPS in 2019. EPS should grow at least mid-single digits. The housing market is doing great and we expect ongoing favorable tailwinds for Home Depot. The stock is still going to go higher, but it could go much higher if they would not miss opportunities to build goodwill with the market as an exceptional corporate citizen.

Our Price Target is $205 which we will leave here for the time being. The Sell Price of $178 is hereby increased to $186.

------------------------------------------------------------------------------

------------------------------------------------------------------------------

Economic Calendar

Capacity Utilization

Wednesday, January 17th, 9:15 AM

Period: December

Consensus: 77.3%

Prior: 77.1%

Housing Starts

Thursday, January 18th, 8:30 AM

Period: December

Consensus: 1,278,000

Prior: 1,297,000

Michigan Sentiment

Friday, January 19th, 10:00 AM

Period: January

Consensus: 97.0

Prior: 95.9

------------------------------------------------------------------------------

------------------------------------------------------------------------------

Time to Take Our Profits in Tesla?

Tesla (TSLA: $336, up 6%) had a great week, but the more we think about it, the more worried we become. They have orders for 400,000 Model S cars and said last year that they would be delivering 5,000 a week starting in October, 2017. Well, guess what, this 5,000 number has slipped a number of times so that now they are talking about the 2nd quarter of this year. That’s a big slip. Maybe there is something seriously wrong here. No one seems to know and the company certainly isn’t helping us with solid information.

The company is going to need massive amounts of cash this year. They are bleeding money each day, each week, each month, so we expect more secondaries this year, diluting existing stockholders. And more bond sales as well.

Can the company survive and thrive? That’s the question that we are wrestling with.

We love the company; the world loves the cars. We love Elon Musk, but he is a promoter for sure. A loveable genius with a $56 billion market cap company.

The more we think about it and the more we write about it, we just have to book our profits. We are up 69% since we added the company two years ago at $199. OK, wait a minute. We’ll let the market tell us when to sell: If the stock goes to $320, we are OUT.

It’s tough to invest in a visionary. The vision always takes longer than the genius or the masses of followers expect.

------------------------------------------------------------------------------

Apple's App Store Broke Records this Holiday Season

Apple’s App Store started off 2018 by breaking app purchasing records on New Year's Day. Consumers spent $300 million in app purchases on January 1, 2018, marking the highest sales day for the App Store since its launch in 2008.

This outstrips last year’s record-breaking figure of $240 million in purchases on New Year’s Day. Customers spent $890 million on apps from December 24th-31st. Insights into app spending during the holiday season are indicative of the strength of the iOS platform for the year to come, as many consumers receive smartphone devices and purchase new apps, games, and subscriptions over the holiday period.

Apple’s App Store revenue gets bigger each quarter and each year. Developers received $26.5 billion for the year, up 30% year-over-year, and is now over $86 billion since 2008. For 2017 the $11.4 billion in revenue was almost 5% of the company’s projected $237 billion in total revenue.

------------------------------------------------------------------------------

------------------------------------------------------------------------------

A Word from Gary Jefferson

Jefferson Financial Group

First Vice-President, Investments

UBS Financial Services, Inc.

Earnings season officially kicked off last week with the big banks leading the way. We expect decent to good numbers, but the big thing to watch for will be forward guidance, particularly on how much tax cuts will impact the bottom lines. Some sectors like Energy will likely benefit more than others which traditionally have been able to pay lower effective rates such astech.

Last week, Bank of America analysts raised their earnings forecast for the S&P 500 by $14 to $153 per share, as a result of the new lower 21% tax rate. (Source: Merrill Lynch). In market-speak, that means that if corporate earnings for 2018 reach $153, and the market's trailing PE is 18, the S&P 500 will be trading at 2754. Today it is trading at 2786…………………….oops, that doesn't sound very promising. For the market to reach 3029 (a 9% gain), the S&P 500 would need to trade around 20X trailing earnings. That is of course doable, and not outside the realm of just being a high-priced market rather than a bubble, but it would be a lot better from a fundamental standpoint if the market could see fit to earn a higher number this year. We should have a better grasp on a projected year-end earnings target after earnings and guidance are announced over the next several weeks.

Meanwhile, what a week the market enjoyed two weeks ago. It was one of the best first weeks of any new year in history. There are plenty of historical stats which show that if the market has a good January, most of the time the year will end up with positive numbers as well.

Even though the jobs report missed expectations for 191,000 new jobs being created last month by coming in at 148,000 instead, the great big story was that this number had 146,000 private sector jobs versus only 2,000 public sector ones. Always remember that government doesn't create jobs – it only takes away from the private sector when it grows, and because it is the private sector that creates jobs, a growing government is the worst case scenario for a growing economy. So "hip, hip hooray" for this ratio of jobs because it is just what the doctor could order for a healthy and robust economy.

The biggest winners for job creation were in Healthcare with 31,000 new jobs (300,000 for 2017), Construction with 30,000 new jobs (210,000 for all of last year), and Manufacturing with 25,000 new jobs (196,000). We also saw gains in Food Services & Drinking Places (government-speak for restaurants and bars), and Professional & Business Services. Thus, these are not part time or low paying jobs for the most part, which is equally important for a growing economy.

Again, we have to keep everything in perspective. The following stats are from Pension Partners:

"From August 18th to November 29th, the Dow went 72 straight trading days without an intraday move greater than 1%, by far the longest stretch in history.

“The S&P has now risen for 14 consecutive months, the longest run in history.

“The Dow closed at an all-time high 71 times during the year, the most in history.

“There was a sharp flattening in the yield curve throughout 2017. At 0.51%, the spread between 10-year and 2-year yields on the last day of trading was the flattest level of the expansion. (This is a "flag" we are watching).

“In spite of this backdrop, the Fed only hiked rates 3 times in 2017, to a year-end range of 1.25 to 1.50%. After subtracting inflation (core CPI of 1.7%), this leaves the Real Effective Fed Funds Rate in negative territory for the 9th year in a row – another longest stretch in history.

“On the flip side:

Unemployment rate (4.1%) – lowest since 2000

Jobless Claims – lowest since 1973

Consumer Confidence – highest since 2004

ISM Manufacturing Index – highest since 2004"

Our take is that we should expect a correction along the way this year to keep this market from reaching the dreaded "bubble status", but we should also not be scared out of the market due to the length of this bull market. All good things eventually come to an end, but all records are also made to be broken. We have no idea when this earnings growth cycle will come to an end, but we simply do not see earnings growth stuttering or falling at this time - just the opposite, in fact, as corporations become ever so more competitive with the reduction of what had been among the world's highest and most onerous tax rates. (35% now cut to 21%). In this environment, we believe earnings will be the game changer – i.e., we are in the proverbial market of stocks, not a stock market. Companies with outstanding earnings growth will continue to provide outstanding returns.

------------------------------------------------------------------------------

PayPal Holdings (PYPL: $80.50) was upgraded by analysts at Cowen from a "market perform" rating to an "outperform" rating. They now have a $88 price target on the stock, up previously from $79. They must be reading The Bull Market Report. Interesting: Our price Target is $87, because that’s the price at which the company will be worth $100 billion. The stock set a new all-time high on Friday.

------------------------------------------------------------------------------

------------------------------------------------------------------------------

The High Yield Corner

By Michael Foster

Vice President, High Yield

Let’s start with a stock that fell below an important number and then quickly recovered.

Omega Healthcare Investors, Inc (OHI: $26, down 3%) has been The Bull Market Report’s big contrarian call for a while now. If you’re a regular reader, you know that we’ve frequently discussed the issues regarding Omega’s tenant insolvency and current negotiations. This has spooked a lot of investors and turned a once 8% yielding stock into a 9% yielding one. At the start of last week, the stock dipped below $27 for the first time since 2014 - a significant development.

There’s no news to drive this. No insider selling announcements, no updates on the ongoing negotiations with Orianna, which could result in a small decline in income or a protracted dispute in bankruptcy court. In either case, Omega is very likely to get paid out something. In both cases, though, Omega’s cash flow is going to suffer.

And what of that cash flow? Again, it’s helpful to look at the numbers. FFO for the last 12 months is $3.40, while annualized dividends are $2.60. In other words, the dividend coverage ratio is 131% - just above the important 130% level that we demarcate as the start of the safest REIT distributions. At its current level, Omega will maintain its payouts with ease.

But what about the haircuts? Orianna provides 5% of Omega’s FFO, so if Omega lost all of that money (a virtual impossibility), the FFO would fall to $3.23, leaving Omega with a 124% coverage ratio. That’s lower than we like, but it’s still over 100%, meaning we aren’t anywhere near a cut.

Let’s project into the future to see exactly when the dividend would get risky. If Omega lost 5% of its portfolio every year, 2019’s FFO would fall to $3.07. The next year’s would be $2.92…and in fact, it would take until 2023 (i.e., 5 years from now) before Omega’s FFO would fall to less than its current payouts. Then, it would hit $2.50.

Keep in mind that we’re playing with the worst possible case here - but let’s play with the math and see what happens to our income stream.

If the future was as bleak as this, 2023 would result in a 3.8% dividend cut to make payouts sustainable. At current prices, that would make Omega Healthcare yield 9.2% (instead of its current 9.6%).

If this is our worst case scenario, it looks pretty rosy. Getting a near 10% dividend over 5 years before a dividend cut that then brings your yield to a still impressive 9% - that’s not much downside.

There is one other consideration. Omega increases its dividend by a penny per quarter. We’ve have written in the past about this; it’s good for investors in the short term, but it will expedite the schedule for when Omega will have to cut its distributions. For that reason, we think it would be best for Omega to stop its quarterly hikes and telegraph to the market its plans to do so many, many months in advance.

We are disappointed that Omega hasn’t done that yet, but we also wouldn’t be surprised if they did this sometime this year. The recent price action demonstrates that the market is expecting the dividend hikes to stop relatively soon. That gives Omega a nice window to make the move without hitting the stock too much further - but we are not sure they will actually make this move at all.

And the reason is simple. We on the outside see a very slow demise of the dividend - management does not. In the last earnings call, CEO Taylor Pickett addressed the issue with some promising numbers:

"We are hopeful, we can develop an out-of-court plan, which if successful, would likely result in cash rents of $32 million to $38 million per year, as compared to the current annual contractual rent of $46 million.”

If successful, that would lower FFO by 1.5% - in other words, hardly anything at all.

Additionally, Omega continues to expand. The company invested over $300 million in the third quarter of 2016, which on its own more than covers the lost FFO from the Orianna issue. By how much? Pickett noted that Omega targets a 9% capitalization rate for investments, meaning that $300 million investment will be almost twice that of the lost cash rents from Orianna.

What about the properties currently occupied by Orianna? Omega is currently working to sell or rent to new operators who are in a better financial position. If successful, this could cause FFO to grow significantly in the next 2 years - and that will make Omega shares skyrocket.

We have faith that Omega’s managers can navigate this admittedly complicated and tricky transition, and that’s why we remain constructive on the stock.

Finally, let’s quickly turn to some other high yield assets: Municipal bonds and closed-end funds. Nuveen AMT-Free Municipal Credit (NVG: $15.65, down 2%) and Invesco Municipal Trust (VKQ: $12.65, down 1%) had a decent showing for the week, in no small part thanks to a seasonal and rather predictable trend. Retail investors sell municipal bonds at the end of the year and buy again in January. This is classic tax loss harvesting at work, and any year where losses in munis are to be found, this trend is noticeable. So far, 2018 has been good to munis - and that is likely to continue. Thanks to the investors looking for their tax-free income streams, both the Nuveen and Invesco funds are seeing positive inflows - something that we are also seeing across the municipal bond market.

Good Investing,

Todd Shaver, CEO and Founder

The Bull Market Report

Since 1998