July 30, 2019

by Scott Martin | Jul 30, 2019 | 7am News Flash

Netflix (NFLX: $362, down 3% earlier this week) disappointed last night and the stock's precipitous overnight decline provides us with a different kind of wake-up call. Whether you're in Netflix or not, you're going to want to read this flash.

On the surface, Netflix delivered a quarter almost entirely in line with what investors told themselves they wanted to see. Revenue of $4.92 billion was only 0.1% below guidance and reflects healthy 26% year-over-year improvement. Even quarter-to-quarter, the company squeezed 9% more cash out of its subscribers than it did three months ago.

Furthermore, despite profit being a lower priority while management invests vast amounts in original content, it was nice to see that Netflix carried $0.60 per share across the bottom line, $0.04 better than we expected.

But the market found fault as Netflix missed its subscriber growth target, losing 126,000 paid U.S. accounts and only adding 2.83 million new viewers overseas. Management told us to expect the audience to grow by an even 5 million accounts, so it's a clear disappointment.

There are some compensating factors like the way revenue hit guidance. Netflix raised prices in many markets and this is apparently where the pain point is. We know that now. Furthermore, management has doubled down on its aggressive growth forecasts and now expects subscriber adds to accelerate again in the current quarter.

We've had it with Netflix. We've warned throughout that it's going to be a volatile ride. The stock is now down 20% since we started covering it this time around, after making 65% back in 2016-17. We're worried about competitors like Disney and Apple starting to crowd into the space. With a negative $3.5 billion of free cash flow this year and next, we'd rather be invested in a company that actually makes money. We hereby remove Netflix from our High Tech portfolio. We added them on July 16th last year. We're gone now on July 18th, 2019.

However, even for a volatile stock, the reaction to so-so numbers was so extreme that we now suspect that the market as a whole is getting overheated. It's not Netflix. It's Wall Street. And an overheated market can lurch lower as fast as it soars. Even counting the stocks that fizzled and left our list under a cloud, the BMR universe is up a dramatic 33% YTD. This is a great time to lock in some of that profit before a moody market can take it away.

Is It Time to Take Some Profits?

Why are we asking this question?We can’t predict the future. You may think we can, but we can’t. And we want YOU to think about where YOU are and where you are going with your investments. We have made some amazing stock picks and we’ve made you a lot of money in many of these. (We’ve had a few losers too.) Roku is now a triple since we added it last year. Shopify is up 350% in two years. Square is another quadruple play. PayPal, Twilio, Paycom, Microsoft, Apple, Visa: all strong performers.

Is it time to take some of that off the table? There are a lot of things to worry about in the world today: Trump, Chinese tariffs, Iran, immigrants, global slowdown, flat earnings for the past quarter and next; negative interest rates in Europe and Japan . . . can they happen here? If so, will the Fed run out of ammunition if short rates go to zero? What about the attacks on Big Tech by Congress and the European Union? Can Facebook, Amazon and Google survive this onslaught? Of course they will, but why sit around with someone hitting you on the head with a hammer. Maybe it’s better to step a little away from the scene.

Lots of questions. No solid answers. Irrational exuberance was proclaimed by Alan Greenspan on December 5, 1996 after an amazing bull run in the preceding few years. But the bull market continued to skyrocket until the Spring of 2000. That’s almost 3½ years after Greenspan’s call. So is it too early to start taking profits now?

Again, we don’t know, but we do know that there are things you can do. You can sell some calls against your stocks. This brings in cash and cushions you on the downside a bit. But if Roku, which was at $32 at the start of the year goes from $110 now to $90 or even lower, it’s not going to cushion you much with $5 of call option income. So perhaps you can take some profits off the table. Maybe you should put some stops in place. Sell some at $104. Sell some shares if it hits $96. Sell some more if it hits $90. Then if it goes to $70, which is a distinct possibility in a nasty bear market, you’ve protected your profits and have cash in the bank.

And don't forget, we’ve got 17 stocks in our High Yield and REIT portfolios that are paying from 3% to 11% dividends. (Be wary of Annaly and New Residential, though.) These stocks are just waiting for you to place some cash in them so that you can sleep better at night.

This content is for our beloved subscribers and anything you see on this page is just an excerpt!

Please note BullMarket.com access is available to paid subscribers only. Our Members Areas include archives of past Newsletters, News Flashes, our eight portfolios including STOCKS FOR SUCCESS, Healthcare, High Yield, High Technology, Aggressive, Real Estate Investment Trusts, Long Term Growth, and Special Opportunities. Also, all of our in-depth research is available, and more.

Already a subscriber?

Login Here

Ready to join?

Subscribe Now!

February 11, 2018

by Todd Shaver | Feb 11, 2018 | Weekly Newsletter 7pm Sunday

The Weekly Summary

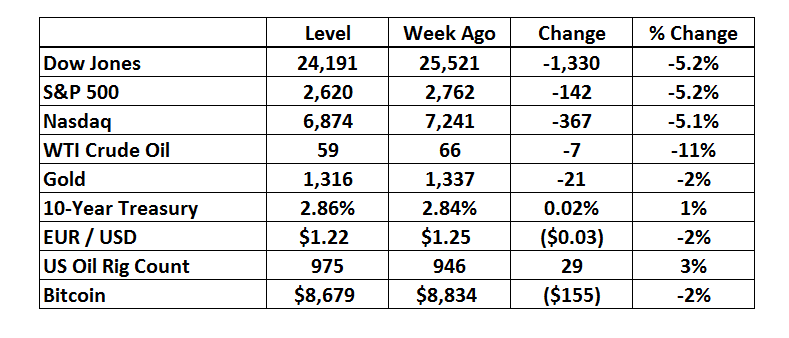

Volatility is back and in an uproar. We’ll run through what is happening in the markets below, but don’t lose sight that although the backdrop warrants caution, the bull market is alive and well. US equities ended their worst week in two years on a positive note with the Dow up 330 points on Friday, but rate-hike fears that pushed markets down remain in place as investors await inflation figures on Wednesday. The S&P 500 tumbled 5.2% in the week, its steepest slide since early 2016, jolting equity markets from an unprecedented stretch of calm. At one point, stocks were 12% below the highs set just two 11 days ago, before a strong rally Friday left the equity benchmark 1.5% higher on the day.

Still, the selloff has wiped out gains for the year. Signs are mounting that jitters spread to other assets, with measures of market unrest pushing higher junk bonds, emerging-market equities and treasuries. The CBOE Volatility Index ended at 29, almost 3x higher than its level January 26th. We at The Bull Market Report are staying calm. We believe stocks are on sale so we would suggest picking out one or two of your favorites and slowly buying more shares.

No matter what is happening out there, there is always a bull market here at The Bull Market Report! This week we highlight: Blackrock, The Carlyle Group, Synaptics, Tesla, CBRE Group, and Ventas.

Key Market Measures (Friday’s Close)

BMR Companies & Commentary

Blackrock (BLK: $522, down 5%)

BlackRock is trusted to manage more money than any other investment firm. Its business is investing on behalf of clients from large institutions, to parents and grandparents, teachers, nurses, doctors and people from all walks of life who entrust their savings to the firm. Well, the company is getting even bigger.

BlackRock is seeking to raise $10 billion for "BlackRock Long-Term Private Capital" to buy and hold $500 million to $2 billion minority stakes in companies for periods of up to more than a decade. The move establishes BlackRock as a potential competitor to Wall Street private-equity giants like Carlyle Group and Apollo Global Management. It is the first-ever attempt by the world's largest asset manager to make such direct investments.

BlackRock has praised Berkshire Hathaway as the best-known example of the strategy. Well, of course. No one has ever done it better. We all know this. BlackRock Long-Term Private Capital will operate differently from most private equity funds, taking full commitments up front and reinvesting as it exits investments. As compared with most investments that return capital to investors after one deal. This is great for Blackrock shareholders because there is no need for ongoing fundraising.

BMR Take: The rock of the investment management industry right now is Blackrock. The company is going to generate nearly $14 billion of revenue this year and produce about $28.60 of EPS. With revenue and EPS growing to over $15 billion and $32.00 next year, respectively, the stock is far from expensive leaving a lot of room for upside.

---------------------------------------------------------------------------------------

The Carlyle Group (CG: $23, down 10%)

Carlyle delivered a solid quarter. Revenue was $1.0 billion versus just $435 million a year ago. EPS hit $1.01 versus just $0.02 a year ago.

Management discussed how the business concluded 2017 with great momentum across all businesses. Carlyle had record activity deploying $22 billion into new investments and raising $43 billion of capital across the platform. Investment performance was exceptional with 20% appreciation across carry funds enabling realizations of $26 billion that went to investors as proceeds for their investments.

The company declared a quarterly distribution of $0.33 per share on February 21st. For full year 2017, they paid out $1.41. That is nearly a 6% yield at the current price.

BMR Take: In private equity The Carlyle Group is a top-notch franchise, known everywhere, the who’s who of business, doing deals in the top floor offices of every major city. The business is raising money like weeds and generating big returns. It is a very compelling opportunity. EPS should hit $3.00 next year leaving this stock dirt cheap.

---------------------------------------------------------------------------------------

Synaptics (SYNA: $44, up 7% - yes really!)

Synaptics reported revenue of $430 million versus $461 million last year. EPS was $1.11 versus $1.49 a year ago. Not terribly pretty, but Synaptics is starting to benefit from the transition encompassing a more diversified product portfolio and customer base, and expects to see strong momentum from investments in infinity displays and consumer IoT in the second half of this calendar year. They continue to make meaningful strides across core growth priorities within chip-on-film, OLED (organic light-emitting diode*), in-display fingerprint technology, and consumer IoT. This includes retail availability of flagship smartphone products, such as new fingerprint, display, and voice-enabled technologies.

* OLED panels are made from organic (carbon based) materials that emit light when electricity is applied through them. Since OLEDs do not require a backlight and filters (unlike LCD displays), they are more efficient, simpler to make, and much thinner - and in fact can be made flexible and even rollable.

BMR Take: With all of the growth investments happening, and the lucrative opportunity emerging for consumer IoT, the quarter’s results were less important than the outlook for attacking this major opportunity. And the outlook is bright. EPS is expected to ramp from around $4 this year to $5 next year and substantially more in the years ahead. We added the stock at $41 in December and our Price Target is $54 and we are hopeful of seeing this during the current year. It would be helpful in achieving this goal if the market calms down and resumes its bull run.

---------------------------------------------------------------------------------------

Tesla (TSLA: $310, down 9%)

Tesla reported revenue of $3.3 billion this quarter versus $2.3 billion last year. For the full year Tesla did $12 billion versus $7 billion a year ago. EPS this quarter was a loss of $3.04.

However, the big ramp in profitability is on the horizon. Revenue is expected to jump to $20 billion this year and $27 billion next year. EPS is expected to swing from a loss to a positive $3.25 in 24 months.

The stock traded about flat after the earnings release that included a fractional revenue miss, and narrower-than-consensus EPS loss. Gross margins came in 190 basis points below consensus, with the Model 3 production ramp weighing on the overall margin profile. But that didn’t really matter as management reiterated its target of 5,000 Model 3 production units per week by the end of Q2.

BMR Take: Most continue to see many moving parts to the Tesla story, with the guidance for sustainable positive operating profits sometime in 2018 garnering more of a show-me attitude, especially given the checkered track record of not hitting guidance milestones or production targets. However, most agree the healthy demand for the Model 3 continues to be a good problem to have, and are spectators on the pace of production execution.

We put a Sell Price of $335 on the stock a few weeks ago so we don’t lose the tremendous profits we have on the stock, but the market this week smashed most stocks down including Tesla. Our Sell Prices are for YOU to decide what to do.

--- We love the concept of the company.

--- We love Elon Musk (Space X with its new successful launch this week has had positive ramifications on Tesla).

--- We love the cars they make.

--- But the debt is crushing.

--- But they have been able to weather the storm through debt and equity sales.

As we’ve said before, this stock could go to $200 or $500. And we’re not sure which will come first? It is very speculative. Should you be in this stock for the wild ride ahead? Only you can decide.

Here’s a 5-year chart. Pretty impressive:

---------------------------------------------------------------------------------------

CBRE Group (CBG: $42, down 5%)

CBRE is crushing it. The company reported revenue of $4.4 billion versus $3.8 billion last year. EPS was $0.99 up from $0.93 a year ago. The consensus expects this year’s revenue to grow from $14.2 billion to $16.5 billion in 2019. EPS is similarly expected to grow from $2.70 this year to $3.20 in 2019.

Fourth-quarter results capped another excellent year for CBRE. Performance significantly exceeded the expectations discussed on the third-quarter earnings call as some concerns surfaced about occupier outsourcing and leasing fee revenue growth. But all that went to the wayside as revenue and earnings for 2017 ended up reaching all-time highs. 2017 marked the 8th consecutive year of double-digit EPS growth for CBRE.

BMR Take: The macro environment is a supportive backdrop for this business, and management continues to operate within an industry poised for long-term growth. This is due to the growing acceptance of outsourced commercial real estate services, the increasing capital allocation to commercial real estate as an institutional asset class, and the continuing consolidation of activity within the industry to the highest-quality, globally diversified market leaders. CBRE Group is a must-own holding in your portfolio in the real estate sector.

We’re up over 60% in two years on this wonderful firm. No dividend yet, but we can see that coming. Our target is $54 and there’s an outside chance it can hit that this year. We know what this company does first hand – they save big multi-national companies money. Big money as in millions and millions of dollars. And the firm gets rewarded in brokerage fees, fixed fees and more. And so few people know about this great firm.

This chart shows the value this stock offers here, after this rough week:

---------------------------------------------------------------------------------------

Ventas (VTR: $52, down 5%)

Ventas reported revenue for the quarter of $895 million versus $875 million a year ago. Revenue for 2017 ended at $3.6 billion versus $3.4 billion in 2016. EPS was $0.50 versus $0.58 a year ago. EPS for 2017 ended at $1.78 versus $1.86 in 2016. Consensus expects revenue to drift upward toward $3.7 billion over the next 2 years. EPS is expected remain stable around $1.75 although we see several sources of EPS upside that are likely to drive revisions closer to the highest Street forecast of $2.15.

All in all, 2017 was another excellent year for Ventas, as the business generated record cash flow from operations and delivered same-store property cash net operating income growth at the high end of internal expectations. To further enhance their diverse portfolio, the company made nearly $2 billion in value-creating investments, including significant expansion of their university-based life science business. And they profitably disposed of almost $1 billion in assets and completed innovative deals with leading operating partners.

BMR Take: Ventas has proven resilient through cycles for two decades. They remain one of the world's best REITs with a specialty in healthcare among other areas.

This success is founded on solid strategic vision, superior foresight and innovation, intelligent and timely capital allocation decisions, rigorous execution and a cohesive, expert team. As they enter 2018 – the company’s 20th anniversary year – management is confident that they can continue the long track record of superior consistent performance as the industry leader.

We added Ventas at $60 in last 2016, a little over a year ago. Until the last two weeks, it was hovering around $56, down a bit, but still paying a nice 6% dividend. It’s worth $18 billion, and has over 1200 properties across the US, Canada and the UK. And as you know, they are in the senior living business along with medical facilities as well. Yes, the stock is down, but this company is strong, and we can only see good things happening from here. If you bought at $60 now is the time to add to your position to bring your cost down. Two years from now we wouldn’t be surprised to see the stock in the 70s, as remember, 10,000 people a day turn 65 in the US. They have to live somewhere!

---------------------------------------------------------------------------------------

We got a letter from one of our readers about Ventas

From: Richard Reed [mailto:reed995@]

Sent: Wednesday, February 07, 2018 10:21 AM

To: The Bull Market Report <Info@bullmarket.com>

Subject: Re: EARNINGS PREVIEW FOR THE WEEK AHEAD

Hi Todd,

Ventas (VTR) is below your Sell Price. Are you lowering the sell price? Thanks.

Richard

Our answer:

Hi Richard –

Look – they own 1200 assets in the United States, Canada and the UK. The properties are senior living properties and more. Are they all going down the tubes? NO WAY. A $19 billion asset paying 6%. We would buy more.

Furthermore, our Sell Price on Ventas is $58. But at $52, we have to say that we like it even more. Nothing has changed for the company in the past two weeks. Yes, interest rates are a shade higher, but nothing out of the ordinary. When the economy is good, rates go out. This is just normal. So to answer your question above, yes, we are lowering our Sell Price to $48. Of course, YOU can make up your own mind on this one, as always, but we would take this opportunity to buy an amazing company at an even lower price.

---------------------------------------------------------------------------------------

---------------------------------------------------------------------------------------

Economic Calendar

CPI Ex-Food & Energy

Wednesday, February 14th, 8:30 AM

Period: January

Consensus: 1.7%

Prior: 1.8%

CPI

Wednesday, February 14th, 8:30 AM

Period: January

Consensus: 1.9%

Prior: 2.1%

PPI

Thursday, February 15th, 8:30 AM

Period: January

Consensus: 2.5%

Prior: 2.6%

Housing Starts

Friday, February 16th, 8:30 AM

Period: January

Consensus: 3.7%

Prior: -8.2%

---------------------------------------------------------------------------------------

---------------------------------------------------------------------------------------

Apple has $285 Billion in Cash

Can you believe this? Again – a record high for any company in history. Apple (AAPL: $156, flat for the week) has $285 billion in cash, or $56 a share. With the stock at $156, that’s 36% of each share of stock in cash. We’re not sure of the Wall St. record, but we are guessing this is twice as much than any other company in history. With the stock flat for the week (amazing) this just screams out at us to add more to the portfolio.

---------------------------------------------------------------------------------------

If the Market Heads Back Up

No one knows where the market is heading. Will it calm down and move higher this coming week and month? Or will it be heading for 23,000 and lower? Again, we don’t know. But if things simmer down and the volatility abates – AND IT WILL – there are a few stocks that we would want to add to our positions in. Here are just a few:

Microsoft

PayPal

Google

Facebook

Apple

Eli Lilly

Yes, many of these are the super Tech stocks that have been leading the market. But guess what? These stocks will continue to lead the market for many years to come.

And one more note. Did you see Annaly Capital Mortgage (NLY: $10.21, down 1%) this week? Solid as a rock. So if you are super worried about things, we believe Annaly can be a store of value for a month or two or 12, and you can enjoy the 11% dividend in this $12 billion market cap company.

---------------------------------------------------------------------------------------

---------------------------------------------------------------------------------------

A Word from Gary Jefferson

Jefferson Financial Group

First Vice-President, Investments

UBS Financial Services, Inc.

There was no comment Monday or Tuesday because everything I wrote was outdated and the numbers were obsolete within minutes of writing, rewriting and re-rewriting them. The dust may or may not have settled, but a few things are much clearer today.

In short, the seismic swings over the past few days have been based on three primary factors that we believe now form a consensus:

1. The threat of higher inflation (Rising bond yields)

2. The possibility of more Fed hikes

3. The long streak without a normal and healthy market shakeout.

How does that stack up against the best economy we've seen in over a decade? In other words, is it good news or bad news that economic growth is so strong the Fed may have to raise rates sooner than expected? Or, is it good news or bad news that nearly half the companies in the S&P 500 have reported fourth quarter results and more than 80% of them have beaten Wall Street's revenue expectations, the highest percentage since the third quarter of 2008? And, is it good news or bad news that the tax law will boost those profits further in the quarters ahead?

Let's put all this in perspective:

First, the market isn’t overbought anymore. We now know that. There was a "10% correction." Let’s get over it.

Second, earnings are robust.

Third, the rise in bond yields has been a headwind, but it’s not signaling a looming recession. Importantly, the 10-year vs. 2-year Treasury yield spread has widened out as yields have risen, implying the bond market is now discounting higher inflation and better economic growth, which over the medium term has almost always been positive for stocks.

While volatility has returned with a vengeance, the market fundamentals are now better and earnings growth prospects haven't looked better in years. Basically, all of the reasons why investors have been bullish on the market last week, last month and last year are still here.

---------------------------------------------------------------------------------------

The High Yield Report

by Michael Foster

VP High Yield

It should always be emphasized that much of a stock's action is not caused by only the underlying company, but also by the industry and the overall market. In a volatile environment, this emphasis is especially important. While our High Yield and REIT portfolios have shown lackluster performance over the past two weeks, the fundamental aspects of the companies that make up the portfolios have not changed.

The S&P 500 decreased 5.1% over the past week, leading to stocks officially being in correction territory. Much of the decline is being attributed to interest rate and liquidity fears, which is why much of the analysis on the portfolio below will focus on those aspects. It takes just one week to rattle bullish sentiment. As an investor, you should not put too much weight on what the general financial media is discussing. What should take priority is thinking about whether the fundamental aspects of the economy and market have changed. When this is the priority, our fear diminishes as we realize that earnings are still strong, nonfarm payrolls on February 2nd were above expectations, and a deregulatory environment is still present.

One metric, the yield curve, is worth looking at though. The spread between the 10-year Treasury yield and the 2-year Treasury yield has been constantly decreasing as a result of the Federal Reserve tightening policies and the lack of inflation. On a basic level, you can note that the presence of an inverted yield curve, if it were to happen, has been a common predictor of past recessions. Going deeper, the economic repercussions of the inversion are much more important. Consumers and banks are directly impacted. For consumers, the cost of credit increases, which leads to a larger portion of expendable income being dedicated to servicing debt. For banks, the spread between long-dated loans and deposits decreases, which leads to worse financial performance. We’re sharing this information so that you can keep the yield curve on your radar, but there’s no need to worry as of now. When the curve inverted in the past, it still took between 7 to 24 months to reach any sort of recessionary state.

AllianzGI Equity & Convertible Income Fund (NIE: $20.59, down 4%) fared slightly better than the S&P’s drop of over 5%. It moved from the weekly low of $19.50 to its current level after recovering about 2.5% in the last hour of trading on Friday. The performance of individual equities which it holds, including Microsoft, Alphabet, and Amazon, led to the recovery in the last hour. Given that the fund invests little in the bonds and the scenario of the inverted yield curve, we can expect the funds to be shifted from Equity to Bonds.

We still see Apollo Commercial RE Finance (ARI: $17.70, down 3%) as a cyclical play on the U.S. commercial real estate sector. Given that commercial real estate in the U.S. remains solid, with Apollo’s loan originations hitting $1.5 billion YTD and the economy of the US continuing to get stronger and stronger, Apollo is not a position to be worried about.

Digital Realty Trust (DLR: $102, down 5%) dropped almost by the same amount as the S&P. This was the opposite of the week prior, where the company maintained strength in the midst of widespread declines. While we noted the continued demand for data centers in the last summary, there are some other metrics to note. Digital Realty, owning many data centers in US and internationally, is affected by rising interest rates as the cost of borrowing rises. The company has a massive debt level of $5.8 billion with a Debt/EBITDA ratio of 22. Rising interest rates could cripple the company’s dividend payout and future prospects.

Invesco Municipal Trust (VKQ: $11.83, flat) ended up at the same level as the beginning of the week. With its investments primarily in investment grade U.S. municipal bond obligations (85%), the fund can expect to yield better returns amidst the current rising interest rates scenario. Also, a Fitch report stating that plans to cut federal funds to them won't impact the revenues of the municipal bond funds and ETFs, played a large part in keeping the fund’s price level stable. Nuveen Municipal (NVG: $14.43, flat), another high yield fund with major investments in U.S. investment grade municipal bonds, also maintained its price level.

Pimco Dynamic Fund (PDI: $30, down 1%) was less volatile. The firm, investing primarily in a range of debt securities, including mortgage-backed securities, high yield corporates, and emerging market bonds, could witness further issues with rising interest rates, changes in tax structure, and better yields.

The REIT sector has been partially impacted by the recent economic data, heightening fears of higher interest rates. Primarily, the sector is engaged in massive borrowings, and rising interest rates could increase the cost of the borrowings. With that said, rising interest rates often occur in a booming economy, which indicates higher demand by consumers.

Market corrections generally provide prudent investors with great buying opportunities. One way of going about this is finding relative strength in strong industries. Applying this analysis to REITs, the overall REIT sector was down only 3%. Within out portfolio, three of the five positions outperformed the sector. Annaly Capital Management (NLY: $10.21, down 1%), Government Properties (GOV: $16.37, down 1%), and Omega Healthcare Investors (OHI: $26, flat) composed that group.

As a company that primarily engages in buying mortgages and mortgage-backed securities (as well as other assets), Annaly could fare very well as interest rates go up and correspondingly coupon rates do as well. While this is not necessarily the reason for the less-than-average drop this week, going forward it is something we will keep in mind. Both Government Properties and Omega should not feel a significantly negative impact by rising rates either. The former gets offered attractive rates by the government as a result of its leases and the latter’s healthcare-related real estate is, for the most part, unaffected by the business cycles.

The other two positions, Ventas (VTR: $52, down 5%) and Welltower (HCN: $55, down 5%), ended up having declines that were in-line with the S&P 500 but larger than the move in the REIT sector.

Ventas reported positive 4th quarter earnings on Friday, which provided a minor boost to the stock. The reported income from continuing operations for 2017, $640,000, was a record for the company. In turn, the EPS and FFO per share numbers were also records. In a rising rate environment, this is a positive sign. With the earnings report occurring during a stock market decline, any overall S&P bounce should result in outperformance by Ventas.

The other relatively weak company, Welltower, did not have any news this week to explain the larger than average decline in the stock. As it is focused on owning senior living properties and funding real estate infrastructure, the large amount of debt maintained could pose an issue within the rising rate environment. Currently, though, the extensive track record of stock appreciation over the past 25 years leaves us unworried. Welltower is also at the lower end of its range for the past four years, so it is a good area to pick up more shares.

Good Investing,

Todd Shaver, Founder and CEO

The Bull Market Report

Since 1998

February 7, 2018

by Todd Shaver | Feb 7, 2018 | Earnings Preview 6 AM

Carlyle Group (CG: $24)

Bull Market Report Target Price: $28

Bull Market Report Sell Price: $24

Earnings Date: Wednesday, 8:30 AM ET

Consensus: 4Q17

Revenues: $780 million

EPS: $0.62

Year Ago Quarter Results

Revenues: $435 million

EPS: $0.02

Key Things to Watch For in the Quarter

Analysts expect The Carlyle Group to report a 79% increase in revenues with a huge increase in earnings per share for 4Q17. The stock has beaten analyst estimates in three of the past four quarters, and is up 43% since this time last year. The Carlyle Group is an investment firm specializing in direct investments in the Fintech Sector. We do not expect the recent selloff to have a grave effect on the stock because of the firm’s concentrated line of business.

--------------------------------------------------------------------------------------------------

Synaptics (SYNA: $41)

Bull Market Report Target Price: $54

Bull Market Report Sell Price: $35

Earnings Date: Wednesday, after market close

Consensus: 4Q17

Revenues: $430 million

EPS: $1.09

Year Ago Quarter Results

Revenues: $460 million

EPS: $1.49

Key Things to Watch For in the Quarter

Synaptics is expected to report a 7% decrease in revenues and a 27% decrease in earnings per share for 4Q17. Despite having beaten estimates in the past four quarters, the stock is down almost 30% since this time last year. We expect the firm’s underlying technology and management team to spur growth over the long-term horizon. Our Target is $54 and our Sell Price is $35.

--------------------------------------------------------------------------------------------------

Tesla (TSLA: $334)

Bull Market Report Target Price: $375

Bull Market Report Sell Price: $335

Earnings Date: Wednesday, 5:30 PM ET

Consensus: 4Q17

Revenues: $3.3 billion

EPS: -$3.10

Year Ago Quarter Results

Revenues: $2.3 billion

EPS: -$0.69

Key Things to Watch For in the Quarter

Analysts expect Tesla to report a 43% increase in revenues and an increase in the earnings deficit for 4Q17. Despite beating estimates in only one of the past four quarters, the stock is still up 27% this year, and that includes the recent sell-off. We expect Elon Musk to continue to drive top line growth as the economy continues to strengthen and electric cars continue to penetrate our roads.

But as we have mentioned we are worried about the capital that Tesla will need to sustain its growth. So we have a Sell Price in place of $335. With the latest market fall-off, the stock dropped from $354 to $333 on Monday, quite a bit below our Sell Price. The Sell Price is there for YOU to decide what to do. Sell? Hold? Buy more? We love this company but with the production delays and thus little money coming in, we're a bit concerned. We may have an update about the firm in the next few days.

--------------------------------------------------------------------------------------------------

CBRE (CBG: $42.50)

Bull Market Report Target Price: $52

Bull Market Report Sell Price: $40

Earnings Date: Thursday, 7:00 AM ET

Consensus: 4Q17

Revenues: $4.0 billion

EPS: $0.92

Year Ago Quarter Results

Revenues: $3.8 billion

EPS: $0.93

Key Things to Watch For in the Quarter

CBRE is expected to report a 6% increase in its revenues and a 1% decrease in its earnings per share for 4Q17. The stock is up 33% on the year, and has been at the forefront of its peers in the real estate industry. CBRE has beaten estimates in each of the past four quarters which helps explain the firm’s bull run. The stock took a pretty heavy hit early this week when investors shaved 10% off the market cap. We believe it has been oversold, especially given the strong economic growth and investor’s natural fear of real estate when markets turn south. We are big believers in CBRE and would accumulate shares here.

--------------------------------------------------------------------------------------------------

Ventas (VTR: $53)

Bull Market Report Target Price: $72

Bull Market Report Sell Price: $58

Earnings Date: Friday, 10:00 AM ET

Consensus: 4Q17Revenues: $875 million

EPS: $0.63

Year Ago Quarter Results

Revenues: $875 million

EPS: $0.58

Key Things to Watch For in the Quarter

Ventas is expected to report no growth in revenues and an 8% increase in earnings for 4Q17. Despite Ventas’s ability to beat estimates in each of the past four quarters, the stock is down 15% since this time last year. The stock currently yields a 6% dividend, and has developed a trend for earnings growth. While some investors are selling the stock due to a lack of revenue growth, we are confident in the ability of management to cut costs and produce growth their bottom line.

January 28, 2018

by Todd Shaver | Jan 28, 2018 | Weekly Newsletter 7pm Sunday

The Weekly Summary

The big news this week was Davos. Davos is an annual event hosted by the World Economic Forum that’s mission is to improve the state of the world by engaging business, political, academic, and other leaders of society to share global, regional and industry agendas. Davos is a mountain resort in the Alps of Switzerland. All of the top brass from companies and countries attend. Trump rocked the party with his message of America first. He said America first does not mean America alone, and that America is open for business. He promoted our 3% GDP growth, our massive tax reform, and our historic reduction in regulation. We put a billionaire in office exactly to do this. The S&P 500 is already up 6% so far this year and Trump’s deals in Davos could drive gains higher.

No matter what is happening out there, there is always a bull market here at The Bull Market Report! This week we highlight: Gilead, Shopify, Bristol Myers, Nutanix, Google, and Tesla.

Key Market Measures

BMR Companies & Commentary

Gilead (GILD: $86, up 6%)

Gilead has had a tough time since 2015; however, its fortunes may finally be changing. The big event is that Celgene is buying Juno Therapeutics for a 50% premium. One of Juno’s most promising drugs directly competes with Gilead. Clearly, Gilead is playing in the right sandbox. The Wall Street research firm Jefferies poured some gas on the fire of excitement now burning for Gilead. They upgraded the stock this week and said to look for good things to happen soon. The company is looking at a February approval and launch of a drug for HIV, and highlighted some key Phase 3 data on another drug to be released by 2019.

BMR Take: The stock appears to be inexpensive at this level, as it trades at just 8x this year’s EPS of $8.70. But we know that earnings are set to decline to $6.50-$7.25 over the next few years as Gilead’s top two drugs face declining sales. These two drugs were among the top three best sellers of all time – but nothing lasts forever. Could Gilead fetch 15-20x EPS when the dust settles and new drugs re-invigorate some excitement? Possibly, but it’s going to take quite some time.

As you may remember, we had the stock in our portfolio and removed it a year ago as we were tired of waiting. It took a year to come back, but from here we think the run is over for at least the next few years. We will remain on the sidelines.

=========================================================

Shopify (SHOP: $129, up 12%)

Somebody stopped by Shopify this week to work on collaboration for the future of augmented reality. Tim Cook. CEO of Apple. No big deal. (HA!) He praised the companies “profound” emerging technology. No further explanation needed. Apple + Shopify = $1.8 billion added to Shopfy’s market cap, now at $13 billion. Wow.

BMR Take: Tim Cook met with developers and coders and listened to demonstrations. Augmented and virtual reality is a major part of Apple’s future plans. These markets are likely to balloon to $215 billion by just 2021. Maybe Apple works with Shopify. Maybe Apple buys Shopify. Either way we see this all leading to good things ahead for Shopify. Their sales are expected to grow from $660 million this year to $1.6 billion by 2020, without factoring in anything from the possibilities with Apple.

Andrew Left of Citron is crying in his beer. (He’s the guy who shorted the stock at $119 and made a big deal about it in the press. He drove it down to $92, and now is losing money big-time. YES!!! We don't like the way this guy operates.) Remember, if you hear that a stock is heavily shorted, that’s a BULLISH signal. Why? Because after you short a stock the only thing you can do from that point on is to BUY THE STOCK BACK. Very bullish.

Look at this chart:

=========================================================

Bristol-Myers Squibb (BMY: $64, up 3%)

Bristol-Myers received a big regulatory approval in Europe this week. The European Commission (EC) expanded the indication of Yervoy to include treatment of advanced melanoma in pediatric patients. The EC approval marks Bristol-Myers’ first pediatric indication for an Immuno-Oncology medicine in the European Union and allows for the marketing of Yervoy for this indication in all 28 Member States of the EU. This is just a key development for geographic market expansion and ultimately sales. Hip hip hooray!

BMR Take: Bristol-Myers is a leader in Immuno-Oncology. This space is red hot. Bristol’s EPS is expected to grow from $3.00 this year to $4.00 in 24 months. This Healthcare bellwether is overdue for a breakout in the stock. Remember, activist Carl Icahn is making some noise here and pushing for good things for all shareholders.

Looking at the 1-year chart, you can see that it is a slow mover, but steadily up. We’ll take that any day. The company is no small firm. The market cap is $105 billion and the stock is moving towards its all-time high of $74 set two years ago.

=========================================================

Nutanix (NTNX: $33, down 8%)

Nutanix caught some heat this week from a downgrade at JP Morgan. The report said nothing specific. They said: The market rally has gone on for eight long years. Valuations aren’t cheap. Nutanix is up a lot lately.

We say: Ignore this report – it appears to be just one person’s opinion. We believe there is more money to be made here. In fact, just this week Nutanix spoke to investors about how hosting providers like Amazon Web Services are taking steps to work with customers more broadly to support bare services, expanding the market opportunity for Nutanix.

BMR Take: Nutanix is a must-own stock. “The opportunity of a decade,” says Goldman Sachs. The customer base has doubled in 18 months. The average annual sales per customer is expanding from $1 million to $5 million, fueling greater than 30% top line growth. And we could see this $5 billion market cap company get bought by the likes of an IBM or Oracle any day. The stock is down this week to where it was in December. But in October, just three months ago, it was $22. Stay on this train!

More on Nutanix below.

=========================================================

Google (GOOG: $1,176, up 3%)

The future of the Smart Home is a big deal. Whoever wins this market is going to make some big bucks. Google Home is now installed in 14 million homes and is well on its way to cementing itself as a key player in the space. The Smart Home of the future will allow you to use voice to control your thermostat, your TV, your lights, your locks, your security cameras, your car ignition, your coffee machine, and on and on. The hardware sales and the multi-year services contracts make for a lucrative revenue opportunity. Google is positioning itself to get in on the action.

BMR Take: One thing we really like about Google is its valuation. When you look elsewhere in Tech – like Facebook, Amazon, Netflix, or Adobe – the price to earnings ratios are way up there. Look, we understand growth and innovation can’t be valued just on a price to earnings ratio alone. But that subjectivity in the analysis leaves room for the high flyers to be in for a rougher valuation reversal in a correction. In contrast, Google is set to generate about $42 of EPS in 2018, which is 29% growth from 2017, and the price to earnings ratio is exactly 29. When the price to earnings ratio is equal to or is less than the earnings growth rate you know as an investor you are paying a reasonable price for growth. Again, that is why we like Google’s valuation.

And again, please have no fear of the high stock price. It’s just a number. Pretend that it has a 20-1 split tomorrow. The price would drop to $59. Would you buy more then? It’s all psychological. Google HAS split their stock 2-1 – once – in 2014. They just might be thinking of doing that again. And we would suggest the stock would shoot higher.

=========================================================

Tesla (TSLA: $343, down 2%)

Tesla’s Gigafactory is exciting! Tesla’s mission is to accelerate the world’s transition to sustainable energy through increasingly affordable electric vehicles and energy products. To achieve its planned production rate of 500,000 cars per year by 2018, Tesla alone will require today’s entire worldwide supply of lithium-ion batteries. The Tesla Gigafactory was born out of necessity and will supply enough batteries to support Tesla’s projected vehicle demand.

Tesla broke ground on the Gigafactory in 2014 in Nevada. The name Gigafactory comes from the word “Giga,” the unit of measurement representing “billions.” The factory’s planned annual battery production capacity is 35 gigawatt-hours (GWh), with one GWh being the equivalent of 1 billion watts for one hour. This is nearly as much as the entire world’s current battery production combined. With the Gigafactory ramping up production, Tesla’s cost of battery cells will decline significantly through economies of scale, innovative manufacturing, reduction of waste, and the simple optimization of locating most manufacturing processes under one roof. By reducing the cost of batteries, Tesla can make products available to more and more people, allowing them to make the biggest possible impact on transitioning the world to sustainable energy.

BMR Take: Seriously. Who builds a Gigafactory in Nevada because their business is using up all of the world’s lithium-ion batteries? Only Elon Musk. So innovative. So groundbreaking. World changing. If Tesla is right about the future of vehicles and takes over the crown of the auto industry from the old guards in Detroit, you don’t want to miss out on the future earnings potential of the company and what this stock could do in your portfolio.

As noted last week, we do have a $335 Sell Price on the stock because of our concern about how much capital they will have to raise this year. It would upset us to have to sell this wonderful company run by a genius, but we have to protect our gains. Watch closely this week.

Note on Musk’s New Pay Package:

Tesla announced a huge pay package this week for Elon Musk that again ties his compensation to key performance benchmarks. This time the goals include taking the electric-car maker to $650 billion in market value

Tesla outlined a massive compensation plan for its unorthodox CEO on Tuesday, setting a series of ambitious growth targets that, if various conditions are met, could net Musk as much as $55 billion over the next decade The package is based entirely on performance, guaranteeing no salary and no bonus, and requires Musk to reach aggressive market capitalization and financial goals in order to be paid. He would also have to hold onto his shares for five years after he receives them before selling. Musk would only receive the full payout if the company reaches a market capitalization of $650 billion, a more than 11-fold increase over its current $57 billion market cap.

=========================================================

=========================================================

Economic Calendar

Consumer Confidence

Tuesday, January 30th, 10:00 AM

Period: January

Consensus: 122.1

Prior: 122.1

Pending Home Sales

Wednesday, January 31st, 10:00 AM

Period: December

Consensus: 109.5

Prior: 109.5

Nonfarm Payrolls

Friday, February 2nd, 8:30 AM

Period: January

Consensus: 172.5K

Prior: 148.0K

=========================================================

=========================================================

We got a letter about Nutanix from Stanley Makovsky, of Stan Lee Marketing, one of our subscribers. He said:

"Todd,

Any opinion on the below report?

Nutanix Stock Falls After J.P. Morgan Warns That Software Shift Could Prove Disruptive"

Stanley Makovsky

Stan Lee Marketing

Hi Stanley – I many times take these things with a grain of salt. Yes, the stock is down 8%, but will it stay down here? Maybe. It might go to $30. But that just might be an amazing buying opportunity.

JP Morgan wrote this opinion based on this:

“on concerns that shares could lag those of peers in the near future following a recent rally.”

Lagging peers? What does that really mean? Who cares about their peers.

This is what matters to us:

The last four quarters of revenue:

$275 million

$226 million

$192 million

$160 million.

I call that growth.

Todd Shaver

=========================================================

The Carlyle Group (CG: $25.60, up 5%)

We've been pounding the table on this stock for months. On December 19th the stock was $21.50. It's now at $26, up 21%. We are pounding the table on this one NOW. We expect $30 in a few months. Do the math. That's another 17%. We have it on good authority that one of the major stockholders is not selling a share until it hits $30. Our Target is $28, but we sure will be happy to raise it to $33 when it hits $28. The Sell Price is hereby raised from $20 to $24. We're up 54% on this one in less than a year; it's paying a 5% dividend. How can you go wrong.

Look at this chart:

=========================================================

CBRE (CBG: $46) Hits All-Time High

Friday saw another all-time high. Earnings are coming out soon and we understand that they will be announcing another solid quarter. Some say it might be called a blowout. We've passed our Target of $40 so we hereby raise it to $52. Our Sell Price is at $35, so we are raising that to $40. The company is in business to save corporations money with their real estate. And that they are doing with relish. This one is a sleeper.

=========================================================

=========================================================

The High Yield Corner

By Michel Foster

VP High Yield, The Bull Market Report

We wish to do a bit of a deep dive into what’s happening in stocks, the economy, and society at large - and what this tells us about high yield.

The reason we want to do this now is that there is a trend that looks very alarming on the surface that is actually not a problem at all. We’re referring to the incessant bull market of 2018.

January is ending in a few days, yet the S&P 500 is up over 6% already this year. Remember that this index goes up about 8% on average every year, so that a 6% gain in a month is very intense. So intense, in fact, that the market has already hit and surpassed the price target that a lot of big bank analysts had on the market for the entire year.

At the same time volatility is down, the financial mass media is getting more bullish, and the general anxieties in society seem to be drifting further and further away from economic issues and towards other domains of human life - politics, religion, identity. This is usually a cyclical trend.

To explain what we mean, think back to 2005 and 2011. Very different years with very different social concerns and economies. 2005 was the height of the housing bubble - a time when exotic dancers in Las Vegas were buying multiple homes to flip (as brilliantly documented in Michael Lewis’s The Big Short.) But Americans are a contentious bunch, so there was plenty of angst and debate going around - a lot of it about gender equality, the war in Iraq, Guantanamo Bay, race relations, and other things. Little talk about income inequality, wage growth, or other economic issues.

Now think about 2011. This was the time of the short-lived Occupy Wall Street movement. The Iraq War, still going on, wasn’t an issue; Guantanamo Bay didn’t come up unless you brought it up to the protestors. Race relations, gender issues were given brief lip service. But the real concern? Income inequality. “We are the 99%” was a rally cry of socio-economically disaffected people.

Whether or not you agreed with their message, their means or their complaints, doesn’t really matter - not for rational investors like us who want to grow our wealth by understanding what’s happening in the world. What matters much more is acknowledging what was going on and why it was going on. Namely, 2011 was a time when political and social unrest hinged on economic issues - because the 99% weren’t getting richer and weren’t even getting the illusion of getting richer that the debt-fueled housing bubble gave so many Americans.

Fast forward to 2018. What are the hot topics of the day? Donald Trump is the obvious one. And, again, whether you support Trump or do not, what does matter is acknowledging that the cultural fixation of the moment is on an issue that has relatively little to do with the economy.

From this perspective, 2018 feels a lot like 2005. The economy is, at least on the surface, showing enough strength to keep people from focusing on economic and financial issues. Corporate profits are rising and look to rise even further. Stocks are going up, as are housing prices and U.S. incomes. A weaker U.S. dollar is hurting imports, but it’s also helping exports and encouraging more tourism to the U.S. - another big boost.

What does all this have to do with the stock market and high yield investments? Two things. First, we seem to be at that stage in the business cycle where hope has already turned into optimism. But we aren’t at the point where optimism turns into euphoria, although it’s getting closer and closer on the horizon. In other words, a lot like 2005.

This tells us that the best thing to do is to buy and hold stocks. Stay in the market. Despite the monstrous gains in the market for 2018, the S&P 500 P/E ratio is down from where it was in the middle of 2016, and if earnings growth meets expectations (13% growth for the year), that P/E ratio isn’t going to go up much further.

It also tells us that high yield remains an option, but investors may become choosier when it comes to high yield as we go further into the greedy stage of the business cycle and away from the fearful stage. That could mean municipal bond prices will remain lower while junk bonds remain higher. That may mean little capital gains from Invesco Municipal Trust (VKQ: $12.30, flat) and Nuveen AMT-Free Municipal Credit (NVG: $15.09, down 2%) despite the fundamental strength in both funds’ incomes. Income may begin to rise if municipal bond yields rise alongside Treasuries. It does not mean a big crash in either fund, however - so don’t rush to sell. Just recognize that these funds’ income streams will remain intact, with some possible upside.

AllianzGI Equity & Convertible (NIE: $22.55, up 2%) and Pimco Dynamic Income Fund (PDI: $30, up 1%) are interesting options for investors. Since these funds have exposure to junk bonds and convertible bonds, the continued increase in profitability and financial strength among America’s companies could drive demand for these funds in excess of what we’ve seen in the past. Both have provided strong total returns since The Bull Market Report first recommended them. More good returns are becoming more likely, thanks to America’s increasingly complacent and euphoric economic mood.

Where does that leave us investors, concerned about volatility, wishing to preserve capital, and hoping for a reliable high income stream? It is too early to worry about a euphoric market, but it is time to recognize that worrisome euphoria and the bubbles they produce could come. That could take a couple of years, perhaps even longer. What matters is that we remain keenly aware of what’s happening in our economy and our society in an impartial and calm way, investing accordingly, and constantly looking, listening, and watching.

Good investing,

Todd Shaver

The Bull Market Report

Since 1998

January 7, 2018

by Todd Shaver | Jan 7, 2018 | Weekly Newsletter 7pm Sunday

The Weekly Summary

Welcome to the New Year! As we begin 2018 we want to first say the capital markets will not always be this friendly to us. We are up against too many horses and mysterious dark forces. So let’s all make sure we enjoy these times. The recent and current times will be remembered as the good old days of the greatest bull market ever recorded in human history.

You have probably noticed that we at The Bull Market Report don’t make prognostications very often. People ask us all the time where the market is going and whether this bull market will come crashing down, and whether this is the time to sell, sell, sell. The problem is that we are in the “no one knows” camp. Anyone who predicts future stock price moves is just guessing. Now, we look at the numbers and base our research and comments on how we see things economically, for the country, the world and for the individual company we are writing about. But if you think we can predict the day the bull market ends, you are mistaken. No one can.

So, what does one do? Well, we have said many times this past year, if you are nervous, then take some profits off the table. Put them in the high yield sector. We have two fabulous portfolios of companies that are stable and are paying strong dividends, to the tune of 6-8% and higher. We, personally like equities and we like the economic numbers that this country is producing, so we wish to stay invested in the companies that are thriving from this strong economy. If and when things turn down, we’ll give you our opinion and you can make those important decisions as they apply to your own personal portfolio, and the financial health of you and your family.

Now to the investing. We read and review countless expert stock market outlooks for you on the topic of what will happen in 2018. While views differ on various things, and nobody has a crystal ball, there is one prevalent belief that institutional investors are positioning for. Essentially everybody is saying that international stocks are the place to be when analyzing the valuations of the marketplace. Now look we are not going to recommend purchase of China Construction Bank or anything of the sort. We instead favor the plenty of great US companies with international revenues. This year keep an eye out in particular for multi-national stocks. Fundamentally, they are positioned to outperform.

No matter what is happening out there, there is always a bull market here at The Bull Market Report! This week we highlight: Microsoft, Google, Amazon, Facebook, Carlyle Group, and Mazor Robotics.

BMR Companies & Commentary

Microsoft (MSFT: $88, up 3%)

One of the biggest things happening right now is US tax reform. Microsoft is sitting front and center. While a lower cash repatriation tax rate in the GOP's tax-reform bill may encourage large tech companies to bring home large amounts of cash currently held abroad, it is unclear how they may deploy those assets. Many worry it will not be used for new investments or higher wages, but simply returned to shareholders. We’re not worrying one bit. We expect the majority of it to indeed go to shareholders, that’s us!

While there has also been a sense that the surge in repatriated assets could spark an M&A boom, these tech companies have hardly been shy about using low interest rates and strong cash flows to fund acquisitions. Some $630 billion is held by the nine tech companies with the largest overseas holdings. Accordingly, we think the freed-up cash is likely to flow toward stock buybacks, paying down debt, and dividends.

For Microsoft, they have over $130 billion of cash parked internationally. After paying the 15.5% tax or $20 billion tax bill, we believe Microsoft will proceed to steadily hike the current dividend rather than pay a one-time special dividend that could be as much as $3. Either way, this is good news for income-oriented equity investors.

BMR Take: Microsoft is currently paying a $1.67 dividend. The consensus outlook calls for $1.81 in 2019 and $1.95 in 2020. This dividend action alone is likely to keep pushing the stock upward. Microsoft remains a core holding for us.

Microsoft was given a new $100 price target on by analysts at Royal Bank of Canada and by Oppenheimer Holdings last week. We have a Target of $92 on the stock and can’t WAIT to raise the Target to $101 when it hits $92.

Not a bad 6-months chart, don’t you think?

Where do you think Microsoft is heading in the next six?

---------------------------------------------------------------------------

Google (GOOG: $1,102, up 5%)

China is the largest consumer market of any country in the world: With 1.4 billion citizens and counting, it has 19% of the global population. This has drawn the attention of some of the world's largest companies seeking to capitalize on its rich opportunities. Even more enticing are its 750 million internet users, many of whom are part of the country's emerging middle class.

A number of U.S. technology companies have been effectively shut out of China's growing internet market, including Google. Chinese regulators took to the podium at the Internet Governance Forum in Geneva recently and said Google would now be welcome. This is fabulous news for the company.

After four years there, Google announced in 2010 that it would no longer censor its Chinese search site, effectively banning itself from the country. This self-imposed exile followed what the company called a "highly sophisticated" hack, which resulted in the theft of intellectual property and attempts to gain access to gmail accounts belonging to human-rights activists.

The changing outlook for growth in China could be huge for Google.

BMR Take: Google’s EPS outlook is $32 for 2017 heading to $41.50 in 2018 and $48 in 2019. This is 29% and 17% EPS growth, respectively, without any material surge in business in China. If we get the upside from China, look out. The runway for earnings growth could be longer than the Great Wall of China.

---------------------------------------------------------------------------

Amazon (AMZN: $1,229, up 5%)

At this week's Consumer Electronics Show, we're going to see the battle between Amazon Alexa and Google Assistant kick in to high gear.

Last year, Alexa was the clear winner of CES, with companies like Ford, Huawei, and LG agreeing to integrate their products with Amazon's virtual assistant. Since then, Alexa has only gotten bigger — over the holiday season, Amazon says that it sold "tens of millions" of Alexa-enabled products, led by its own Amazon Echo Dot.

This year, Google is striking back. While the search giant's Google Home speakers still lag the Amazon Echo in terms of market share, it's picking up momentum: Google claims that it sold over 6.7 million Home and Home Mini speakers over the holiday shopping season.

You can expect both companies to make announcements about new partners, new products, and new ways to use their respective voice agents. LG has already announced that it will be showing off new TVs with Google Assistant built in; a company called Vuzix will be debuting a pair of Alexa-powered smart glasses.

Amazon got in on the smart speaker market early, and has moved quickly to ensure its stays out in front. By most measures, the Amazon Echo is dominating the smart speaker market. This could be a great driver of future earnings growth so we are watching closely.

BMR Take: This week we wanted to present a bit of a different perspective on Amazon. The view is Mark Cuban’s. He says you can’t even value Amazon on revenue or earnings like other publicly traded stocks. Essentially Amazon is one massive start-up with scale. You know when they bought Whole Foods the market cap of Amazon went up so much that day the increased value covered the purchase price of Whole Foods. They literally bought Whole Foods with no capital. So you see this innovation machine can’t even be analyzed like other businesses out there. You just have to own it. It’s the innovation machine that will lead the way wherever technology and the world go. The Amazon Dot is just the latest example of innovation.

---------------------------------------------------------------------------

Facebook (FB: $187, up 6%)

The company's founder and CEO Mark Zuckerberg posted his annual personal memo on Thursday — mostly about being a better CEO — but one throwaway reference to cryptocurrency technology captured everyone’s attention.

Writing about how the last year saw many people lose trust in social media and tech companies, Zuckerberg noted the growing importance of de-centralizing forces, like the rise of cryptocurrency. He said, "There are important counter-trends to this — like encryption and cryptocurrency — that take power from centralized systems and put it back into people's hands. But they come with the risk of being harder to control. I'm interested to go deeper and study the positive and negative aspects of these technologies, and how best to use them in our services."

Zuckerberg was referring to bitcoin. It is telling that Zuckerberg specifically called out cryptocurrency in his annual new year's resolution post. When you look at the broader landscape of social media companies and messaging platforms, it makes perfect sense that Facebook would be paying very close attention to such technology.

First, consider that nearly 100% of Facebook's revenue comes from online advertising. This figure shouldn't be all that surprising — the social network has long been one of the single most dominant players in digital advertising. Still, the company would be foolish not to pursue other meaningful revenue sources long-term. Adopting some kind of cryptocurrency plan could be one way to do that. But rather than buying into one that's already established, like bitcoin, what might be more likely is Facebook creating its own. Who better to pull off a legit crypto currency than Facebook?

BMR Take: Facebook is going to generate about $6 of EPS this year. We are looking at EPS growing to $10 by 2020. Layer into this the possibilities of a proprietary Facebook coin and look out, this could be a stock set to surge even more than it already has on bitcoin mania.

---------------------------------------------------------------------------

The Carlyle Group (CG: $24, up 5%)

Carlyle Group has brought on a new leader of its U.S. capital markets division. Matthew Savino was named managing director and head of U.S. capital markets. It is a new position. Mr. Savino works with Carlyle's U.S.-based corporate private equity executives on publicly syndicated and privately placed loan, bond and equity offerings for portfolio companies. Mr. Savino was a managing director and global head of alternatives sourcing at BlackRock.

Why does this matter? Private equity is all about sourcing deals. That is the business model. Exclusive deal sourcing is the key to the fabulous earnings we see. And getting this done is all about good people. Let’s review a few of the heavy hitters on the board. This company is stacked with talent.

Mr. D’Aniello is a founder and Chairman Emeritus. Prior to forming Carlyle in 1987, Mr. D'Aniello was a Vice President for Finance and Development at Marriott Corporation where he was responsible for valuation of all major mergers, acquisition, divestitures, debt and equity offerings, and project financings.

Mr. Conway is a founder and Co-Executive Chairman and is also the firm’s Co-Chief Investment Officer. Prior to co-founding Carlyle in 1987, Mr. Conway worked at MCI Communications from 1981 to 1987, serving as Chief Financial Officer.

Kewsong Lee is a Co-Chief Executive Officer. Mr. Lee also serves as the Head of the Global Credit segment and is Chairman of the Executive Group. Prior to joining Carlyle in 2013, Mr. Lee was a partner at Warburg Pincus and a member of the firm’s Executive Management Group.

Ms. Lawton Fitt is a member of the Board of Directors. Ms. Fitt is currently a director of Ciena Corporation and The Progressive Corporation. She was an investment banker with Goldman Sachs, where she was a partner and a managing director. She retired from Goldman Sachs in 2002. Ms. Fitt is a former director of ARM Holdings and Thomson Reuters

Tony Welters is a member of the Board of Directors. Mr. Welters is Executive Chairman of the Black Ivy Group. He recently retired as Senior Adviser to the Office of the CEO of UnitedHealth Group having served in such position since 2014.

BMR Take: With the S&P 500 index trading at 20x earnings, we just can't explain why Carlyle trades at 8x earnings. There is no reason for such a massive discount. This stock needs to be a lot higher. Others overlooking the stock creates your opportunity. If we had a category for stock of the year (2018), this one would be at the top of the list. The consensus calls for nearly $3.00 of EPS this year! This company is way undervalued. Repeat – WAY UNDERVALUED.

---------------------------------------------------------------------------

Mazor Robotics (MZOR: $56, up 10%)

Mazor Robotics is a pioneer and a leader in the field of surgical robotic systems. In September the company announced CE Mark approval for its Mazor X Surgical Assurance Platform. The CE Mark allows Mazor and its commercial partner, Medtronic, to market the Mazor X in the European Union, as well as other countries that recognize the CE Mark.

This is big stuff and we saw the benefits last quarter when Medtronic essentially sold almost all of the company’s new orders.

Receipt of the CE Mark is an important step in the plan to expand the patient, surgeon and hospital benefits of the Mazor X Surgical Assurance Platform to the European market. The commercial partner for the Mazor X, Medtronic, will be responsible for marketing and selling the system in Europe and they have a great footprint and brand to do so.

BMR Take: Mazor shares increased 150% in 2017 and we think the momentum is going to continue. The company is coming off of a record 3Q17 earnings where it was announced that orders were received for 22 systems comprised of 19 Mazor X and 3 Renaissance. Medtronic was responsible for 11 of the 19 Mazor X purchase orders, which is only the second phase of the commercial agreement, where additional orders are in the pipeline to occur. There is just clear surgeon interest in everything Mazor is doing. Why? When you step back and think of it, this is the start of artificial intelligence and robots beginning to increase productivity. Mazor is at the center of the action in the medical technology sector where the advancement will change lives, and the economic opportunity for investors will be lucrative.

---------------------------------------------------------------------------

---------------------------------------------------------------------------

Economic Calendar

Consumer Credit

Monday, January 8th, 3:00 PM

Period: November

Consensus: $18.5 billion

Prior: $20.5 billion

JOLTS Job Openings

Tuesday, January 9th, 10:00 AM

Period: November

Consensus: 6,025,000

Prior: 5,996,000

Wholesale Inventories SA M/M

Wednesday, January 10th, 10:00 AM

Period: NOV

Consensus: 0.70%

Prior: 0.70%

PPI ex-Food & Energy

Thursday, January 11th, 8:30 AM

Period: December

Consensus: 2.5%

Prior: 2.4%

CPI ex-Food & Energy

Friday, January 12th, 8:30 AM

Period: December

Consensus: 1.7%

Prior: 1.7%

---------------------------------------------------------------------------

---------------------------------------------------------------------------

Oil Holds Near Two-Year High. US Shatters Production Record

The Permian Basin* has shattered its 1973 record to produce 815 million barrels of oil during 2017, or more than 2.25 million barrels a day. The previous peak of 790 million barrels was set 44 years ago. The huge oil field is projected to push total U.S. oil output to a new all-time high by the end of this year. Some analysts see total US production exceeding 10.5 million barrels per day by the end of 2018.

*The Permian Basin is located in the western part of Texas and the southeastern part of New Mexico. It reaches from just south of Lubbock, to just south of Midland and Odessa, extending westward into the southeastern part of New Mexico.

Oil prices are expected to keep rising in 2018 on the back of OPEC-led production cuts and a growing global economy. Most analysts see oil trading in the high 50s for 2018.

The U.S. total rig count will reach above 1,000 rigs in 2018, for the first time since 2015, according to one oil analyst. Rig counts ranged from 660 to 960 in 2017. The current level is 925.

BMR Take: The best way to take advantage of the robust Energy market is with our portfolio item, iShares US Energy ETF (IYE: $41, up 4%). We’ve had this stock in our portfolio since September and it is up 11%, but we feel it has a long way to go higher. It’s a small fund, with just $1 billion in assets, paying a 2.7% dividend, and it is diversified nicely among many strong Energy companies. Exxon is #1, with 23% of the portfolio invested in this global leader. Chevron is #2 at 15%, Schlumberger is at 6%, ConocoPhillips is at 4%, and other companies, like Valero and Kinder Morgan are held as well. Our Target is $44, but we can see this one hitting $50 in 2018 if crude holds or goes higher than its current level of $60.

---------------------------------------------------------------------------

---------------------------------------------------------------------------

Some Target Updates

Visa (V: $119, up 4%) had its price target raised by analysts at Susquehanna Bancshares from $126to $148 last week. Our Target is $123, and we can’t wait to raise our Target into the $130s. The way the market is going, it might just hit our Target this week.

Apple (AAPL: $175, up 4%) was given a new $180.00 price target on by analysts at Rosenblatt Securities. We think this firm has its head in the sand. Our Target is $194 which is when the stock will hit $1 trillion in market cap.

Omega Healthcare Investors (OHI: $27, down 2%) Director Bernard J. Korman bought 100,000 shares stock just before Christmas. The shares were bought at an average cost of $26.90 per share, for a total transaction of $2,700,000. Following the transaction, the director now owns 900,000 shares, valued at $24 million.

We always like to see these types of transactions – management buying stock with their own money. The stock is paying a 9.7% dividend. It is below our Sell Price by $1, but we aren’t going to remove the stock just yet. With their more than 900 nursing facilities and assisted living facilities in the US and UK, we believe the firm to be solid as a rock. Worried about the bull market ending? (we aren’t….), then lighten up some of your portfolio and buy some Omega. You’ll be glad you did.

---------------------------------------------------------------------------

---------------------------------------------------------------------------

The High Yield Corner

By Michael Foster

We saw some significant macroeconomic news stories over the last couple of weeks that are very important for high yield. They’re important because they’re easily misunderstood, but not because they’ll have a huge impact on high yield assets.

Quite the opposite, in fact. What is happening right now is a blip that means little for the high yield world, although it may be a bigger deal for some pockets (most notably Energy and Utilities). Beyond that, however, what’s happening right now really doesn’t matter for high yield.

What are we talking about?

The first is the polar vortex. If you’re on the east coast or in the midwest, you know what we’re talking about. We were working in New York City for the 2013-2014 polar vortex, and we must admit we are still a little traumatized by the experience. The biting wind, the endless cold, the layers of snow covering more layers of snow was enough to make us leave NYC. We still feel bad for friends who were stuck at banks and hedge funds, unable to leave the Big Frozen Apple.

Beyond this malaise with the cold, the broader economy was suffering. The American economy saw a 0.1% GDP growth rate, and the S&P 500 barely ended the quarter in the green (January of that year saw a 3.6% decline in the stock market). The polar vortex put a freezing chill on the 30% S&P 500 return that 2013 enjoyed.

It seems like history is repeating itself. After the S&P 500 rose 22% in 2017, we’re suddenly hit with a cold snap to start 2018. The stock market hasn’t responded to this yet, and we doubt it will. Enough people remember 2014 to know that a sudden freeze isn’t enough to hit stocks.

However, the high yield market is a lot more volatile and easily scared. We’ve already seen at the retail level, fund outflows at several major high yield ETFs in the first few days of January. And many popular high yield assets are starting 2018 in the red.

For instance, look at REITs. Omega Healthcare Investors (OHI: $27, down 2%), Government Properties Income Trust (GOV: $17.86, down 4%), Digital Realty Trust (DLR: $112, down 1%), and Apollo Commercial Real Estate (ARI: $18.30, down 1%) are all weak in the first week of January. We may see more declines in the future as retail investors remember 2014 and pull out—while also forgetting that markets adapt and counterbalance recent tendencies. Trends last only until they don’t.

So much for the first big trend hitting high yield—it’s definitely worth ignoring, or going against. As these REITs slip on cold weather panic, buying opportunities become bigger as yields go higher.

The second big news story for high yield is much, much more obscure, but is arguably more important. Morgan Stanley quietly recommended to clients that investors avoid junk bonds. Here’s what he wrote:

"While the tax cuts just enacted in the U.S. may lead to better growth in the short term, they may also bring forth the excesses we typically see before a recession—which is something credit markets figure out before equities. We recently took our remaining high yield positions to zero as we prepare for deterioration in lower-quality earnings in the U.S. led by lower operating margins.”