by Scott Martin | Sep 3, 2019 | Free Newsletter (Sent Weekly Monday at 12pm)

The Weekly Summary

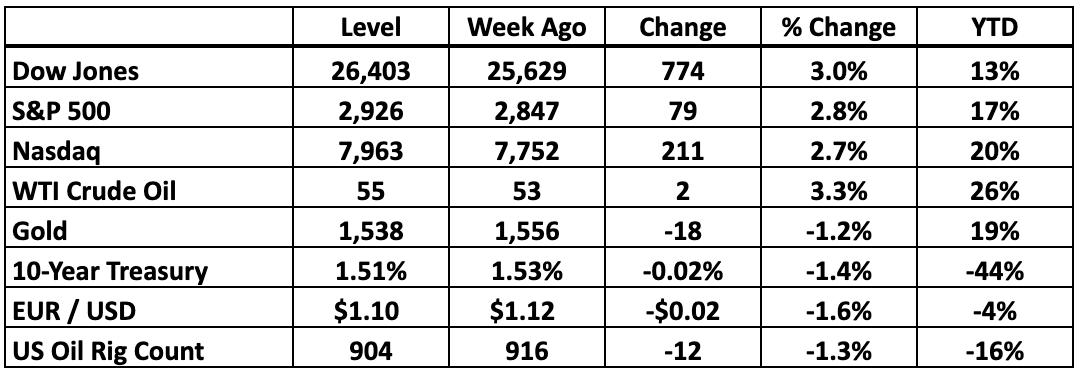

Last week brought a volatile month to a relatively quiet close, with stocks recovering a lot of lost ground in an almost-uninterrupted surge. Evidently concerns about the Treasury yield curve inverting were only a smoke screen for investors who were simply bored with the diplomatic dithering around the trade war and looking for a reason to park their assets. Now that summer is over, Wall Street is ready to get back to work.

Admittedly, the yield curve is still inverted, earnings for S&P 500 companies have gone nowhere for three quarters in a row and the trade war casts as long a shadow over the global economy as ever. However, that's nothing new. The curve flattened out a year ago and tariffs have been in force for roughly the same period of time. Anyone who bought the market then and sold last month has to reckon with the fact that the fundamentals didn't change in the meantime.

The only thing that changed was sentiment. That's why we suspect last month was more a matter of exhaustion than actual dread. After all, the Fed has already relaxed interest rates once and is now only two weeks from what most of us suspect will be another rate cut. The environment is more aggressively weighted to the upside than it has been all year.

We suspect the S&P 500 will recover the 1.6% it is down from July soon. From there, the clock starts ticking before a fresh earnings season gives the market its next real shot at year-over-year traction, earnings growth and ultimately sustainable upside. As far as we're concerned, the party never stopped for our stocks, at least from a fundamental perspective. When the market as a whole gets back in the groove, we're looking forward to what will follow.

There’s always a bull market here at The Bull Market Report! Want a free trial? Let us know!

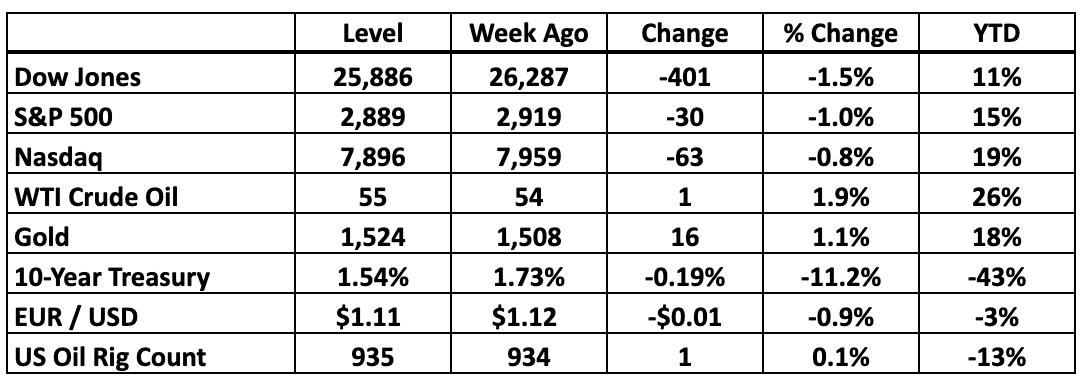

Key Market Indicators

-----------------------------------------------------------------------------

BMR Companies and Commentary

The Big Picture: No Earnings Recession Here

While we’re still eagerly awaiting one more report to wrap up our 2Q19 scorecard, for all practical purposes it’s time to start looking ahead to the cycle that starts six weeks from now. Once again, our outlook is strong even though the broad market has nothing to get excited about lately.

Given the headwinds blowing against Technology and Energy and the broader drag of unsettled trade policy, the S&P 500 is going to have a hard time avoiding a third quarter of year-over-year earnings decline. It’s not about a deteriorating economy. Revenue remains robust. Demand isn’t softening. Only the margins are under pressure.

However, a little pressure on the margins is enough to eliminate any immediate urgency around buying the market as a whole. Those stocks aren’t likely to race ahead of the fundamentals before the companies actually start raising the bottom line. The first realistic window for that happening opens in January, which in market terms is a long time away.

And then there are the stocks we recommend. Compared to what could easily become 3% lower earnings for the S&P 500, the BMR universe is currently tracking 13% growth in the current quarter. That’s more than enough to justify a rally season and even a little urgency to grab the most dynamic companies.

We admit that all of these numbers are just averages. A lot of our companies are coming off big growth spurts so the 3Q19 cycle will reflect some year-over-year declines. Amazon, Twitter and Twilio are currently in that category. They need a rest and have strong enough long-term profiles that we can afford to give it to them.

Others like Apple, Blackstone and Dropbox have already weathered a few quarters of margin pressure but as management pivots the comparisons are getting better. They’re on the edge of getting their growth grooves back. When they do, we’ll be here. Until then, however, the stocks are going to stay in a lower gear.

As usual, Technology is where the extremes are. We see the fastest overall growth in the High Technology portfolio, with its concentration of companies that are following dynamic business models at a much earlier stage than today’s Silicon Valley giants. Their glory years are still ahead, and they’re moving at high speed to make it happen.

Those giants dominate our Stocks For Success list, where we’re expecting only slightly better 3Q19 results than the market as a whole . . . good enough to outperform but not a recipe for a huge rally in the next few months. And then there’s the Aggressive list, where management continues to sacrifice immediate profit in order to capture massive revenue gains while they can.

Then there are the REITs, which are all over the map because of the way Real Estate accounting works to write down property values while passing most of the tangible income back to shareholders. Our recommendations here are tracking up to 340% earnings growth and down to 60% earnings deterioration, along with the full range of results in between. Even if we factor them out as too erratic on a quarter-by-quarter basis, we’re still looking for significant growth throughout our universe.

That’s what it takes to keep BMR stocks moving in the bullish direction even if the market as a whole stalls. All in all, 13% more profit than what these companies delivered last year logically translates into 13% upside for the stocks once investors are back in a buying mood.

The stocks we’ve had throughout the last year still need to gain 10% before hitting their collective peak. Some have soared while others have a lot of ground left to make up, but on a growth-adjusted basis multiples in our universe are much more attractive than ever.

The market as a whole, on the other hand, is clinging to a 4% year-over-year gain even though earnings have declined. That’s almost entirely a factor of more relaxed rate policy. If not for the Fed, there’d be no reason for the S&P 500 to make any headway at all.

Remember, the Fed is our friend as well. Lower interest rates help BMR companies as much as they help everyone else. And the math is clear. Everything else being equal, would you rather be in stocks with historical headroom and positive growth, or those that justify near-record levels with fundamentals that look stagnant at best?

Quarter after quarter, the companies we recommend keep moving forward. We’ve seen that translate into a lot of upside already, but as the fundamentals move up, the stocks inevitably follow. The rest is simply a matter of riding out the market’s mood swings.

NOTE: In our weekly paid subscription Newsletter, we do between 5 and 7 SnapShots and also support regular Research Reports. The last three stocks we recommended are already up 5% apiece. Plus, we have the Weekly High Yield Investor, whereby we discuss the 17 stocks in our High Yield and REIT Portfolios.

And to top it all off, we send News Flashes each day during the week. Got a question about any stock on the market? We'll answer. So if your favorite stock reports earnings or there is significant news, you will hear about it here first. If you want the whole picture, join the thousands of Bull Market Report readers who are making money in the stock market and subscribe here:

www.BullMarket.com/subscription

It’s only $249 a year, and later this year we will be raising it to $499 or even $999 a year, it is just THAT valuable. But we will lock you in for life at this lower price.

Good Investing,

Todd Shaver, Founder and CEO

The Bull Market Report

Since 1998

Subscribe HERE:

www.BullMarket.com/subscription

Just $249 a year, soon to go up to $499. But you are guaranteed the SAME PRICE forever.

by Scott Martin | Aug 26, 2019 | Free Newsletter (Sent Weekly Monday at 12pm)

The Weekly Summary

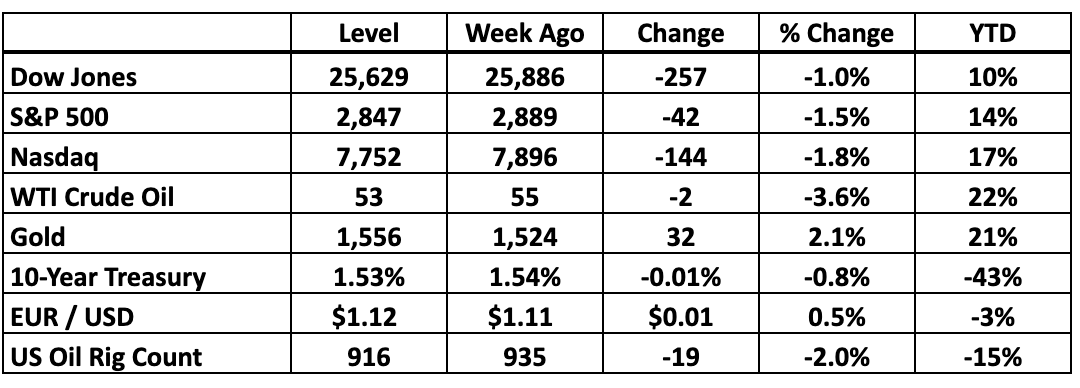

The market recovery that started when calmer heads prevailed on Monday evaporated on Friday as comforting words from the Federal Reserve were unable to cut through new tariffs from China and tough talk from the White House. As we write this, it's looking like tomorrow will be another down day.

We've seen a lot worse. Admittedly, it's not fun to see what looked like a promising week slip away, leaving the S&P 500 and our recommendations down around 1.5%, with another 1% decline brewing overnight. However, as long as the economy remains relatively robust and corporate earnings hold up, there's no reason to get nervous.

The Fed is still our friend. The next interest rate cut may be only three weeks away. We also doubt that the market has had time to fully appreciate last month's rate cut just three weeks ago. Until that happens, the situation looks no worse than what we faced when summer 2018 came to an end.

Stocks are fairly valued relative to future growth prospects. Taxes are low. Expectations are realistic. And yes, the trade war continues. None of this is new. None of it has changed. The only thing that's changed is that investors and corporate executives alike are getting frustrated with a lack of clear guidance from Washington. Until we get clarity, stocks are stalled at least until the next earnings cycle starts in mid-October. We're willing to wait through a few stormy weeks to reap the rewards ahead.

There’s always a bull market here at The Bull Market Report! This week we're providing two separate "Big Picture" views, one tactical and one that's more strategic. The High Yield Investor reviews two of our most defensive recommendations if you're looking to pivot to the sidelines, but that's for subscribers only. Likewise, updates on our Stocks For Success (up an average of 103% since we started coverage, beating the S&P YTD by 10%) are behind the paywall. Want a free trial? Let us know!

Key Market Indicators

-----------------------------------------------------------------------------

BMR Companies and Commentary

The Big Picture: Splunk's Acquisition Agitation

While most investors would be happy to see their chosen stocks keep making money forever, others get caught in a mindset where every consideration vanishes but the exit. These are the people who routinely sell Splunk (SPLK: $119, down 5% last week) every time a quarter goes by with no acquisition announcement. As far as they’re concerned, the company only exists to attract a lucrative offer from somebody bigger.

We question that logic because we know how the corporate consolidators actually think. When someone like Microsoft, PayPal or Salesforce.com pays a premium to absorb a smaller rival, valuation usually takes a back seat to strength. Dynamic companies with solid balance sheets, aggressive business plans and the growth trajectories to back them up are naturally more attractive than those facing resistance creating new markets or competing in established ones.

Good companies get taken out at a high price. Every day their management teams negotiate with potential suitors makes them more valuable and sweetens the ultimate offer. In the meantime, shareholders see the progress, giving the stock room to climb on its own. That’s what success looks like. Succeed long enough on your own and you find yourself in the consolidator’s role, buying small companies to bolt their capabilities onto what you already have.

That’s how the buyers keep growing. Splunk is at that stage now, which is in the background of its post-earnings swoon last week. Some people were really hoping that Salesforce.com would take it out. Maybe one of these days management will get an offer they truly can’t refuse.

In the meantime, we like our companies as going concerns. They’re attractive on their own and have a compelling business plan and the resources to achieve their potential. If someone wants to accelerate that glide path by paying a premium above the present value, we won’t complain . . . but if anything, it’s a little disappointing because it takes a great stock off the market. We’d rather have them stick around and keep making money year over year.

Splunk has made BMR subscribers about 45% a year for the last 3.5 years. Accepting a takeout offer, even if it’s in the $150 zone, ends that journey with one last exclamation point.

That said, deal activity is getting more intense and the price tag on each major acquisition is rising. People in the Technology sector in particular see bigger deals ahead. We might not see Splunk get bought out any time soon, but any of our Aggressive positions and most of our smaller High Technology stocks would make some consolidator a tempting prize.

Just look at Roku (ROKU: $138, up 5%). It’s come a long way for us in the last 14 months, but it’s still “only” a $16 billion company. Someone like Apple could pay cash once they get serious enough about controlling the burgeoning Streaming Video market. That day is coming. For now, we’re happy to let the stocks evolve on their own.

-----------------------------------------------------------------------------

The Bigger Picture: Far From The End Of The World

Wall Street has been an extremely bumpy ride this month, with the S&P 500 down 4% and the BMR universe dropping 3% since the trade war stole the spotlight from the most supportive Federal Reserve meeting in ages. And indications as we write this Sunday evening are for a big drop at the opening Monday. A little shell shock is natural. After all, it isn’t the end-to-end decline that hurts as much as the emotional impact of weeks of reversals and accumulated uncertainty.

We did the math and August is indeed shaping up as 25% more volatile than average, based on the way stocks have been swinging in the hours between the market open and the close. Normally we’d expect to see a 1.3% range from intraday low to the high. This month is tracking above 1.6%, which puts it on the edge of the top quartile in terms of volatility.

In other words, we should expect to see 3-4 months this wild every single year we’re in the market. Last year saw ambient volatility surpass what we’re seeing now in February, October and December. None of them were great months for investors, but they were all survivable. The world did not end.

Of course an uptick in volatility often takes stocks down, but the math at this point is far from apocalyptic. Normally the S&P 500 goes up seven months of the year and drops in the remaining five. The only suspense is which seasons will be the bullish ones and how large the moves will be in both directions.

However, when stocks are moving this fast during a typical day, the odds of a “good” month drop to about 50-50. Again, that’s far from an automatic loss, much less any kind of sell signal. It’s simply an expression of the statistical facts. When stocks are moving fast, volatility spikes. Any sudden lurch to the downside will generate wild intraday swings.

The open question is how long this choppy season lasts and how bad it gets. As a worst-case scenario, we went back to 2007-9, just in case you’re still wondering whether a similar recession is on the immediate horizon. Intraday volatility hit 1.8% in October 2007 when the market was in the earliest stages of deterioration, drifted in slightly elevated territory as the pressure built and then spiked with the Lehman Brothers collapse in September.

After that, it took another eight months for the wild swings to recede to normal levels. All in all, investors needed to hang on for a year and a half. If you’re concerned about a repeat of that cycle, we suggest making sure a combination of dividends and cash reserves will take you through that length of time while waiting for the market to recover from an especially nasty downswing. Bear markets of that scale only happen a few times per century of course and we’re only a decade out from the last one. But for those looking to cover themselves from the worst likely scenario, these are the numbers.

We’re a long way from a repeat of 2008. While it only took 60 days for the S&P 500 to slip into 10% correction territory, the 20% bear market threshold didn’t come for another six months. In most down cycles, that would be close to the end. That time around, volatility got extreme before the healing began.

Corrections happen. Even recessions are a natural part of every long-term investor’s life. But based on the last one, people who stayed liquid and resisted the urge to liquidate doubled their money in the decade that followed.

That’s a decent long-term return for a few months of patience. And of course all of this is purely to quantify the worst downswing in generations. We see no sign of the current shudder turning into anything like that storm.

After all, we expect at least 2-3 months like this in every 12-month period. Wall Street was probably overdue a little rain. Once the clouds clear, stocks still look like the best investments around. The fundamentals aren’t deteriorating precipitously the way they did in 2007. Until they do, it’s just a little sprinkle.

-----------------------------------------------------------------------------

Amazon (AMZN: $1,750, down 2% -- all returns are for the week)

Amazon may be up only 16% YTD, but it's been a wild ride. The stock is positioned to pop back into the $1,900-$2,000 range where it traded for most of the summer.

The 2Q19 numbers were mixed, with revenue jumping 20% YoY and 17% from 1Q19 to $63 billion, but EPS of $5.22 fell short of analyst estimates (consensus was $5.57). Management also lowered 3Q19 income to $2.1-$3.1 billion, lower than the $4.4 billion the market had been expecting. The company also posted the lowest quarterly net income in a year, with just $2.6 billion.

However, all of this is being driven by the $800 million the company is spending to upgrade its facilities in an effort to speed up delivery times. Faster delivery means more revenue and net income in the long run, so Amazon is willing to trade some short term pain for long term gain. (What else is new for this company!)

Jeff Bezos pointed out that free one-day delivery is now available to Prime Members on over 10 million items, and “we’re just getting started.” Plus, the company’s high margin Amazon Web Services grew 37% YoY to $8.4 billion. Yes, Microsoft is picking up steam in cloud computing (which we’ll get to in a moment), and that’s why AWS slipped from 41% YoY growth during 1Q19. But 37% is still astounding, and this is still by far the dominant market leader, so it’s worth focusing on the big picture here. Amazon may have lightly stumbled in this earnings call, but that’s only because its eyes are on the long-term prize. Don’t expect this gentle stumble to send the company reeling any time soon.

BMR Take: Amazon just opened its largest-ever campus in India, where the company is committing $5 billion to grow into that burgeoning market. The company is also growing out its Portland Tech hub, not to mention building its famous ‘HQ2’ in Virginia outside of Washington, DC. Plus, AmazonFresh – the company’s grocery delivery business – is expanding into secondary markets at the moment like Houston, Phoenix and Minneapolis. This plays into the faster delivery times initiative that Bezos and company have been laser-focused on. In short, Amazon isn’t done disrupting the world, in fact – to quote Bezos again: “We’re just getting started.”

NOTE: In our weekly paid subscription Newsletter, we do between 5 and 7 SnapShots and also support regular Research Reports. The last three stocks we recommended are already up 5% apiece. Plus, we have the Weekly High Yield Investor, whereby we discuss the 17 stocks in our High Yield and REIT Portfolios.

And to top it all off, we send News Flashes each day during the week. Got a question about any stock on the market? We'll answer. So if your favorite stock reports earnings or there is significant news, you will hear about it here first. If you want the whole picture, join the thousands of Bull Market Report readers who are making money in the stock market and subscribe here:

www.BullMarket.com/subscription

It’s only $249 a year, and later this year we will be raising it to $499 or even $999 a year, it is just THAT valuable. But we will lock you in for life at this lower price.

Good Investing,

Todd Shaver, Founder and CEO

The Bull Market Report

Since 1998

Subscribe HERE:

www.BullMarket.com/subscription

Just $249 a year, soon to go up to $499. But you are guaranteed the SAME PRICE forever.

by Scott Martin | Aug 19, 2019 | Free Newsletter (Sent Weekly Monday at 12pm)

The Weekly Summary

If it isn’t the Fed, it’s trade. And if it’s not trade, it’s the yield curve, which really amounts to the Fed not moving fast enough to give edgy investors a smooth enough ride. As far as we’re concerned, the market isn’t about comfort, so we’re more interested in the fundamentals, which remain constructive.

This week, the S&P 500 dropped another 1%. The elite Dow industrials gave back a little more and the Nasdaq held up a little better. BMR stocks charted a similar course. Since the July peak, the market has swung in what we can call a “mini correction” pattern, with losses adding up to 3% to 7% on any given day. Our universe is down 4% over the same period.

People are selling just to get away from whatever fear factor they care to fixate on. Good stocks are falling roughly as far as bad ones, regardless of whether they’re rate-sensitive, recession-resistant, vulnerable to a backlash from China or not. A full 70% of the S&P 500 dropped last week and we suspect the mood will remain fragile until investors receive substantive good news (and not simply a pause in the dread-driven headline cycle) and get off the sidelines.

That good news can take the form of action from the Fed at the Jackson Hole central bank summit this week, although we find it hard to believe that Jay Powell and company will cut rates so soon after the last policy meeting. That’s an admission of desperation. We don’t actually want that. However, the Fed has other tools at its disposal, including the ability to manage interest rates through selective intervention in the bond market. That wouldn’t be bad.

And of course we could see a breakthrough on trade, but that’s unlikely ahead of the G-7 summit in France over the weekend. The head of the European Union might not make it to the meetings due to gallbladder surgery and besides, China isn’t actually invited. Normally we’d look to the earnings calendar, but the main 2Q19 season is over now. (We only have two companies reporting this week. You’ll get our view on them Tuesday morning.)

But if the market as a whole is losing its nerve, we see this as an opportunity. As we mentioned in Thursday’s exclusive News Flash, U.S. stocks look no less attractive now than they did a year ago, the last time the S&P 500 peaked and needed a few months to rest.

While trailing earnings growth hasn’t been great, expectations for the coming year are a little better than they were at the end of last summer. The economy as a whole is expanding at roughly the same rate. And valuations haven’t run any higher ahead of the fundamentals than they were a year ago.

Trade tension is nothing new. Last August, companies like Apple had a pretty good sense of how icy relationships with Chinese partners were getting. Sales to Chinese customers were soft or, in some cases, completely interrupted by government bans. Tariffs on Chinese products were already in the air, forcing alert executives to shift their supply chains to countries like Thailand and Vietnam in order to avoid taking even a temporary hit to their profit margins.

A year ago, all these factors triggered a lot of warnings and ultimately fed into the 4Q18 market decline. Now, however, we’ve lived in that shadow long enough that the reduced outlook is old news. In a few months, the year-over-year comparisons get a whole lot easier. Historically that’s all Wall Street needs to get the wheels turning again.

What’s different is that while short-term interest rates are where they were last September, we now expect them to go down as the absence of inflation gives the Fed more room to relax. A year ago we were looking for higher interest rates and we got them. From here on out, the rate environment gets easier.

In theory, that means corporations find it easier to buy back stock and fund lavish dividends. They can even borrow more cheaply to keep shareholders happy or reinvest in strategic acquisitions or other investments. And if a relaxed rate environment weakens the too-strong dollar, executives will cheer.

If you were in the market a year ago, we see little reason to get out now unless your psychology has shifted. Maybe you’re tired of risk and want an easier ride for a little while. We get that. Otherwise, with Treasury yields falling, stocks remain the best allocation around.

There’s always a bull market here at The Bull Market Report! We’ve de-risked our defensive recommendations for the new environment to cut out as much potential downside as we can on that side. The High Yield Investor has all the details, but that's for subscribers only. Here, The Big Picture takes a frank look at the recession calendar in light of the latest developments in the bond market.

Key Market Indicators

-----------------------------------------------------------------------------

BMR Companies and Commentary

The Big Picture: Ticks On The Recession Clock

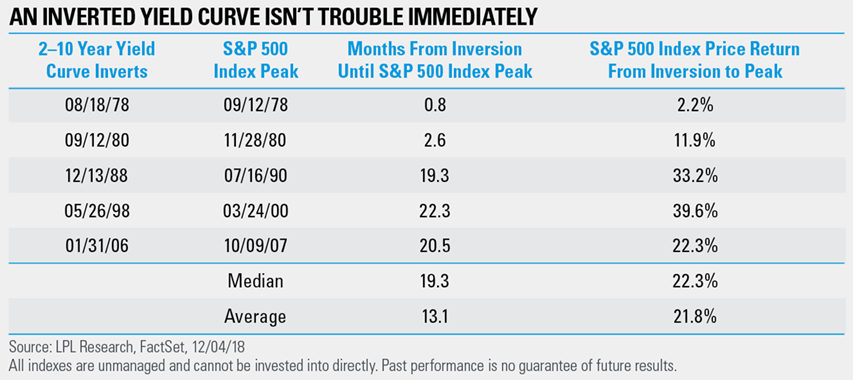

We’ve been weighing each incremental wobble in the Treasury yield curve for months now, keeping you in the loop as signs of stress in the bond market add up. Last week, the rest of the world caught on and suddenly everyone is talking like there’s a recession at the door.

Granted, while most of the curve inverted a long time ago, the closely watched spread between 2-year and 10-year yields took until Wednesday to flip, with debt maturing in 2021 briefly paying more interest than bonds that come due in 2029. Since this is the relationship economists have focused on for decades, a lot of people who thought they could ignore the bond market are having to concede the tough truth.

By the strictest conventional standard, we’re now in an inverted world. You can try to move the goal posts and redefine the terms, but for most of us, the bell has now rung. While interest rates can drift in and out of inversion territory from here, Wednesday’s final break is now a matter of historical record. And that means cutting through the noise to determine what this signal really reveals and how investors need to position ourselves for the future.

First, because the 2-to-10-year spread is so closely watched, we know a lot about where markets go from here. The curve generally inverts when an economic expansion is entering its final stage before a contraction resets the cycle. Sometimes, of course, the Fed and other factors delay that recession for so long that there’s practically no connection, but in general we’ve now got about 22 months before government economists call the top.

That’s a practically luxurious amount of time in the stock market, so there’s no urgency to liquidate vulnerable positions ahead of the storm. A typical economic expansion only runs 60 months anyway, which means investors who tap out 22 months before the end evade all the recession periods but cheat themselves out of 35% of the good times as well. Follow that strategy and you’re going to spend almost half your life on the sidelines, locked out of opportunities as well as the cyclical threat.

And while stocks generally track the economic cycle, there’s usually a three-month lag at the end where the S&P 500 keeps going after the recession starts. We saw this in 2008 and the statistics say that it’s played out the same way after other yield curve inversions. In general, the S&P 500 keeps moving up in the year after the 2-to-10-year spread flips. It’s only when you look two and three years out that the market tends to hit a wall.

We admit that a recession can be gruesome, especially if you’re still nursing psychological bruises from the last one a decade ago. But dwelling on historical trauma is a sure way to cheat yourself out of the benefits of investing across the cycle. The goal is to hang in there as long as you can while the market is moving up, whether that rate of wealth creation is fast or slow. Then, when it’s clear that the economy has stalled, you can cash out well before the downswing takes you to the bottom.

Statistically, the S&P 500 has a pretty good chance of earning investors another 13% over the next year. That’s not so bad . . . in fact it’s a little better than average. And as dynamic as BMR stocks are, we’re fairly confident you’ll do at least that well, even in an inverted world. After all, since the first whiff of trouble on the yield curve about a year ago, our universe is up 11% counting stocks we’ve cut along the way. The market as a whole hasn’t gone anywhere.

So if our stocks keep outperforming at this rate, it’s going to take a lot of pain on Wall Street to make it worth retreating to the sidelines. More likely, subscribers have the chance to attract significant wealth before the party finally shifts into reverse.

Timing is always uncertain, which is why we don’t spend a lot of effort trying to second-guess the market twists. But unless we’re looking at the shortest delay in history between inversion and recession, the rally has about 11 months left to go. More likely, the bulls will keep running well into 2021.

Either way, the last time this part of the curve inverted was in 2005, which gave investors 21 months to squeeze what they could out of growth stocks and shift into more defensive positions. Think about how far some of our recommendations have come in a fraction of that time. If you’re more concerned about risk than missing out on that level of return, it’s time to start making that defensive shift. We’d rather you feel confident now than push you beyond your emotional comfort zone.

-----------------------------------------------------------------------------

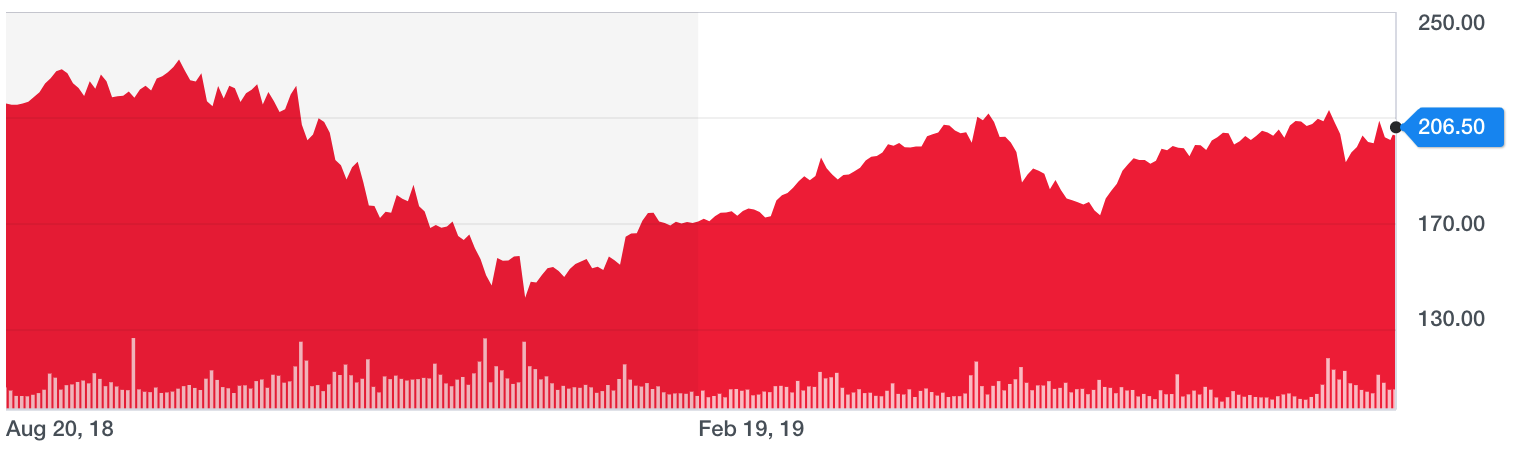

Apple (AAPL: $206.50, up 3%)

Like most companies (deserving or not), Apple was dinged during the recent tough talk that took place between the Trump administration and the Chinese government. Even though things have cooled off a bit, the market is still roiling given the inverted yield curve situation. That’s less of an issue for Apple, which is why the stock has held up very well (up 28% YTD).

Apple does have exposure to China via the iPhone, but the company is rapidly diversifying away from its core product. 3Q19 was the first time since 2012 that the iPhone made up less than 50% of revenue (48%). The quarter also produced a 1% YoY revenue bump to $54 billion, even though iPhone sales were down 12% YoY. That comes by way of a growing Services segment (up 13% YoY), as well as resurgent sales of both Macs and iPads. Macs were up 10% YoY, and iPads up 8%. 3Q18 saw both products produce 5% YoY losses. So that’s a big swing in just 12-months time.

Apple’s Wearables segment is also growing. 3Q19 Wearables grew an astounding 48%, and this is rapidly becoming a core feature of the underlying business. All of this diversification is coming at just the right time, because China revenue is down 20% YoY, which makes sense given the trade war implications. It seems 4Q18’s poor iPhone performance was a blessing in disguise, as it spurred management to accelerate the diversification strategy, which is now paying dividends.

BMR Take: Even though Apple has exposure to China, that exposure is rapidly being mitigated by the diversifying product base. Also the growth of high-margin Services (which is location-independent) is a strong plus. The concern at the moment isn’t just China, it’s the yield curve, and Apple isn’t vulnerable there. We expect the stock to hold up nicely throughout the rest of the year, and the long-term is looking even rosier given the multiple revenue streams.

NOTE: In our weekly paid subscription Newsletter, we do between 5 and 7 SnapShots and also support regular Research Reports. The last three stocks we recommended are already up 5% apiece. Plus, we have the Weekly High Yield Investor, whereby we discuss the 17 stocks in our High Yield and REIT Portfolios.

And to top it all off, we send News Flashes each day during the week. Got a question about any stock on the market? We'll answer. So if your favorite stock reports earnings or there is significant news, you will hear about it here first. If you want the whole picture, join the thousands of Bull Market Report readers who are making money in the stock market and subscribe here:

www.BullMarket.com/subscription

It’s only $249 a year, and later this year we will be raising it to $499 or even $999 a year, it is just THAT valuable. But we will lock you in for life at this lower price.

Good Investing,

Todd Shaver, Founder and CEO

The Bull Market Report

Since 1998

Subscribe HERE:

www.BullMarket.com/subscription

Just $249 a year, soon to go up to $499. But you are guaranteed the SAME PRICE forever.

by Scott Martin | Aug 12, 2019 | Free Newsletter (Sent Weekly Monday at 12pm)

The Weekly Summary

While the week got occasionally tense, volatility has evidently peaked for the time being. Wall Street now accepts that the trade war has escalated and that sweeping tariffs are more likely to take effect before we see signs of a breakthrough on negotiations. Progress simply looks grudging at this point, while the clock keeps ticking to the moment when imports will become more expensive and exports to China will freeze.

Nonetheless, we're satisfied to see the market mood firm up. Even though major indices declined again a bit last week, breadth is no longer overwhelmingly negative. On Monday, 97% of the S&P 500 declined in unnatural unison. A few days later, 45% of the market gained ground for the week as a whole. This is part of the process of recovering from shocking news. We've seen it again and again. Investors who initially panic at the headlines ultimately return to buy back the positions they liquidated, often at a higher price.

It's also nice to see our stocks hold up relatively well. The BMR universe retreated only 0.45% last week, beating all major indices. We had a few natural advantages here. First, our REITs and Healthcare recommendations fared well as safe havens, as well as bond replacements for investors fleeing declining Treasury yields. Our High Yield portfolio was flat. However, while most Technology-driven strategies have been suffering, our High Tech stocks surged an aggregate 4% thanks to huge earnings from Roku and Shopify.

Look behind the market as a whole and money is rotating into Technology as well as High Yield havens. Investors aren't fleeing risk across the board. The mood is less panicked than opportunistic. And in that scenario, we suspect our opportunities will shine brighter than a lot of other stocks. Some are already surging. Others are simply riding the wave.

There’s always a bull market here at The Bull Market Report! Our subscribers got in-depth looks at Amazon, Microsoft and our top win of the year (among other stocks), but to give you a taste, we'd like to introduce you to a smaller company today. The Big Picture weighs the market as a whole to evaluate whether expectations are too high, too low or simply on track. After all, if you don't know which stocks we recommend, you're kind of stuck with whatever the broad market does.

Key Market Indicators

-----------------------------------------------------------------------------

BMR Companies and Commentary

The Big Picture: What About The Rest Of The Market?

We’ve talked a lot about the stocks we recommend over the last few weeks. After all, that’s what The Bull Market Report is all about, and since our universe has outperformed the market as a whole this season, it’s been as much a delight as a duty. When investors are back in a buying mood, BMR stocks will top the list of opportunities they just can’t resist.

Of course we’re happier when solid quarterly results are rewarded with rallies instead of retreats, but this is not one of those seasons. Too many investors are obsessing over macroeconomic headlines to digest the way specific companies are rolling with the externals and still generating the kind of cash that rewards shareholders.

As far as these companies are concerned, tariffs aren’t a concern. Many are growing fast enough to weather the policy winds and still achieve management’s long-term objectives. Others are nimble enough to adjust their operations away from trade war threats. And quite a few are insulated from the global market because they still do the bulk of their business in the United States, free from currency concerns and other external headwinds.

The rest of Wall Street isn’t so lucky, but it isn’t as awful as some people want you to think. A year ago, interest rates were exactly where they are now and moving higher as the Fed tightened. People were optimistic, thinking we’d see at least 7% earnings growth continue for the foreseeable future. There wasn’t a cloud in the economic sky.

Back then, the S&P 500 rated a 16.6X earnings multiple, which is a little rich compared to some historical cycles but reasonable in a context of significant earnings growth and low interest rates. Low rates justify higher multiples because bonds just can’t compete as well with stocks for investors’ attention. Growth reduces the amount of patience we need for valuations that may look rich today to become more reasonable as cash flow compounds.

Expectations weren’t unrealistic. People were looking for the index to rise about 10% over the next 12 months, at which point they would have been comfortable seeing stocks command levels of 18.3X next-year earnings. They came awfully close.

Now here we are. Near-term growth expectations have cratered as it becomes clear that U.S. manufacturers and commodity producers can’t fight a strong dollar and rising trade walls overseas. Look out beyond 2019, however, and the outlook is brighter than it was a year ago. These companies have weathered a lot of margin pressure. Now they’re starting to grind efficiencies out of the economic realities they see.

Six months from now, the S&P 500 has a pretty good shot at getting the growth gears moving again. In a year, the market as a whole can easily be back in rally mode. After all, interest rates are dropping, taking financing costs down with them. If the dollar retreats as well, global competition gets a whole lot easier.

And once again, expectations are relatively modest. People are looking for the index to rise about 10% over the next 12 months, buoyed by a little growth on the horizon accelerating into 2020 as the Fed’s relaxed posture takes hold. In that scenario, the market would command a next-year multiple of 18.7X 2020 earnings, which is no steeper than what investors cheerfully accepted last summer and, factoring in likely growth, even a little more attractive.

We know that it can get hard to hear the signal through the day-to-day headlines. But tariffs just aren’t a huge factor in corporate guidance right now. More companies talked about trade threats a year ago than we’ve heard from in the last few weeks. The only difference is the distribution. Manufacturers and Commodity Producers will always feel the heat in a tense global environment, but now Big Tech is worried about losing access to foreign markets as well. As always, we’ll keep you posted when we see tangible impacts.

-----------------------------------------------------------------------------

Paycom (PAYC: $241, up 2%)

Paycom can do no wrong, even in a market downswing. The stock had another phenomenal quarter, and the global growth strategy is playing out exactly as management hoped it would (organically, with very little leverage).

2Q19 revenue rose 31% YoY to $170 million, and EBITDA came in at $70 million, well-ahead of the $64 million consensus expectations. No matter how high the consensus, Paycom always outperforms. Management raised its 2019 EBITDA estimate to $307 million, up from previous guidance of $297 million. That sent the stock soaring, which of course we love.

Some other notable metrics are recurring revenue, which came in at $166 million, or 3% above consensus, and gross margin which topped 85% (consensus was below 84%). These numbers prove Paycom is monetizing its current user base to a greater extent than the market expected, and that they are doing so in a more efficient manner (that gross margin beat is terrific).

BMR Take: Paycom has over 13,000 customers and growing. Continued income growth means management can expand its global footprint without a reliance on debt. How many $15 billion growth-companies can say that? The company has $95 million in cash and only $60 million in debt. If those numbers were reversed, we’d still be comfortable with the liquidity given the margin and income growth. But as is, management has a ton of flexibility should it wish to pursue acquisitions or expand the sales force. We love Paycom’s position as the industry leader in human capital management, and predict continued upside for this shining star of a stock.

NOTE: In our weekly paid subscription Newsletter, we do between 5 and 7 SnapShots and also support regular Research Reports. The last three stocks we recommended are already up 5% apiece. Plus, we have the Weekly High Yield Investor, whereby we discuss the 17 stocks in our High Yield and REIT Portfolios.

And to top it all off, we send News Flashes each day during the week. Got a question about any stock on the market? We'll answer. So if your favorite stock reports earnings or there is significant news, you will hear about it here first. If you want the whole picture, join the thousands of Bull Market Report readers who are making money in the stock market and subscribe here:

www.BullMarket.com/subscription

It’s only $249 a year, and later this year we will be raising it to $499 or even $999 a year, it is just THAT valuable. But we will lock you in for life at this lower price.

Good Investing,

Todd Shaver, Founder and CEO

The Bull Market Report

Since 1998

Subscribe HERE:

www.BullMarket.com/subscription

Just $249 a year, soon to go up to $499. But you are guaranteed the SAME PRICE forever.

by Scott Martin | Aug 9, 2019 | 7am News Flash

Netflix (NFLX: $362, down 3% earlier this week) disappointed last night and the stock's precipitous overnight decline provides us with a different kind of wake-up call. Whether you're in Netflix or not, you're going to want to read this flash.

On the surface, Netflix delivered a quarter almost entirely in line with what investors told themselves they wanted to see. Revenue of $4.92 billion was only 0.1% below guidance and reflects healthy 26% year-over-year improvement. Even quarter-to-quarter, the company squeezed 9% more cash out of its subscribers than it did three months ago.

Furthermore, despite profit being a lower priority while management invests vast amounts in original content, it was nice to see that Netflix carried $0.60 per share across the bottom line, $0.04 better than we expected.

But the market found fault as Netflix missed its subscriber growth target, losing 126,000 paid U.S. accounts and only adding 2.83 million new viewers overseas. Management told us to expect the audience to grow by an even 5 million accounts, so it's a clear disappointment.

There are some compensating factors like the way revenue hit guidance. Netflix raised prices in many markets and this is apparently where the pain point is. We know that now. Furthermore, management has doubled down on its aggressive growth forecasts and now expects subscriber adds to accelerate again in the current quarter.

We've had it with Netflix. We've warned throughout that it's going to be a volatile ride. The stock is now down 20% since we started covering it this time around, after making 65% back in 2016-17. We're worried about competitors like Disney and Apple starting to crowd into the space. With a negative $3.5 billion of free cash flow this year and next, we'd rather be invested in a company that actually makes money. We hereby remove Netflix from our High Tech portfolio. We added them on July 16th last year. We're gone now on July 18th, 2019.

However, even for a volatile stock, the reaction to so-so numbers was so extreme that we now suspect that the market as a whole is getting overheated. It's not Netflix. It's Wall Street. And an overheated market can lurch lower as fast as it soars. Even counting the stocks that fizzled and left our list under a cloud, the BMR universe is up a dramatic 33% YTD. This is a great time to lock in some of that profit before a moody market can take it away.

Is It Time to Take Some Profits?

Why are we asking this question?We can’t predict the future. You may think we can, but we can’t. And we want YOU to think about where YOU are and where you are going with your investments. We have made some amazing stock picks and we’ve made you a lot of money in many of these. (We’ve had a few losers too.) Roku is now a triple since we added it last year. Shopify is up 350% in two years. Square is another quadruple play. PayPal, Twilio, Paycom, Microsoft, Apple, Visa: all strong performers.

Is it time to take some of that off the table? There are a lot of things to worry about in the world today: Trump, Chinese tariffs, Iran, immigrants, global slowdown, flat earnings for the past quarter and next; negative interest rates in Europe and Japan . . . can they happen here? If so, will the Fed run out of ammunition if short rates go to zero? What about the attacks on Big Tech by Congress and the European Union? Can Facebook, Amazon and Google survive this onslaught? Of course they will, but why sit around with someone hitting you on the head with a hammer. Maybe it’s better to step a little away from the scene.

Lots of questions. No solid answers. Irrational exuberance was proclaimed by Alan Greenspan on December 5, 1996 after an amazing bull run in the preceding few years. But the bull market continued to skyrocket until the Spring of 2000. That’s almost 3½ years after Greenspan’s call. So is it too early to start taking profits now?

Again, we don’t know, but we do know that there are things you can do. You can sell some calls against your stocks. This brings in cash and cushions you on the downside a bit. But if Roku, which was at $32 at the start of the year goes from $110 now to $90 or even lower, it’s not going to cushion you much with $5 of call option income. So perhaps you can take some profits off the table. Maybe you should put some stops in place. Sell some at $104. Sell some shares if it hits $96. Sell some more if it hits $90. Then if it goes to $70, which is a distinct possibility in a nasty bear market, you’ve protected your profits and have cash in the bank.

And don't forget, we’ve got 17 stocks in our High Yield and REIT portfolios that are paying from 3% to 11% dividends. (Be wary of Annaly and New Residential, though.) These stocks are just waiting for you to place some cash in them so that you can sleep better at night.

This content is for our beloved subscribers and anything you see on this page is just an excerpt!

Please note BullMarket.com access is available to paid subscribers only. Our Members Areas include archives of past Newsletters, News Flashes, our eight portfolios including STOCKS FOR SUCCESS, Healthcare, High Yield, High Technology, Aggressive, Real Estate Investment Trusts, Long Term Growth, and Special Opportunities. Also, all of our in-depth research is available, and more.

Already a subscriber?

Login Here

Ready to join?

Subscribe Now!