The Weekly Summary

Last week brought a volatile month to a relatively quiet close, with stocks recovering a lot of lost ground in an almost-uninterrupted surge. Evidently concerns about the Treasury yield curve inverting were only a smoke screen for investors who were simply bored with the diplomatic dithering around the trade war and looking for a reason to park their assets. Now that summer is over, Wall Street is ready to get back to work.

Admittedly, the yield curve is still inverted, earnings for S&P 500 companies have gone nowhere for three quarters in a row and the trade war casts as long a shadow over the global economy as ever. However, that's nothing new. The curve flattened out a year ago and tariffs have been in force for roughly the same period of time. Anyone who bought the market then and sold last month has to reckon with the fact that the fundamentals didn't change in the meantime.

The only thing that changed was sentiment. That's why we suspect last month was more a matter of exhaustion than actual dread. After all, the Fed has already relaxed interest rates once and is now only two weeks from what most of us suspect will be another rate cut. The environment is more aggressively weighted to the upside than it has been all year.

We suspect the S&P 500 will recover the 1.6% it is down from July soon. From there, the clock starts ticking before a fresh earnings season gives the market its next real shot at year-over-year traction, earnings growth and ultimately sustainable upside. As far as we're concerned, the party never stopped for our stocks, at least from a fundamental perspective. When the market as a whole gets back in the groove, we're looking forward to what will follow.

There’s always a bull market here at The Bull Market Report! Want a free trial? Let us know!

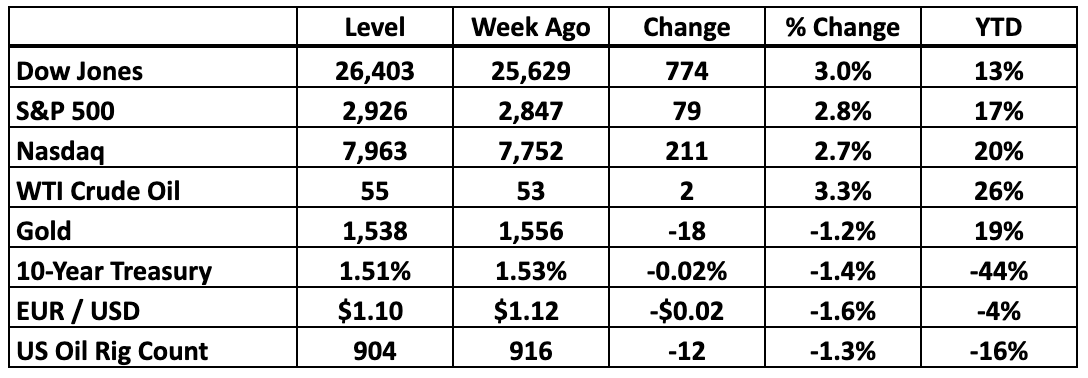

Key Market Indicators

-----------------------------------------------------------------------------

BMR Companies and Commentary

The Big Picture: No Earnings Recession Here

While we’re still eagerly awaiting one more report to wrap up our 2Q19 scorecard, for all practical purposes it’s time to start looking ahead to the cycle that starts six weeks from now. Once again, our outlook is strong even though the broad market has nothing to get excited about lately.

Given the headwinds blowing against Technology and Energy and the broader drag of unsettled trade policy, the S&P 500 is going to have a hard time avoiding a third quarter of year-over-year earnings decline. It’s not about a deteriorating economy. Revenue remains robust. Demand isn’t softening. Only the margins are under pressure.

However, a little pressure on the margins is enough to eliminate any immediate urgency around buying the market as a whole. Those stocks aren’t likely to race ahead of the fundamentals before the companies actually start raising the bottom line. The first realistic window for that happening opens in January, which in market terms is a long time away.

And then there are the stocks we recommend. Compared to what could easily become 3% lower earnings for the S&P 500, the BMR universe is currently tracking 13% growth in the current quarter. That’s more than enough to justify a rally season and even a little urgency to grab the most dynamic companies.

We admit that all of these numbers are just averages. A lot of our companies are coming off big growth spurts so the 3Q19 cycle will reflect some year-over-year declines. Amazon, Twitter and Twilio are currently in that category. They need a rest and have strong enough long-term profiles that we can afford to give it to them.

Others like Apple, Blackstone and Dropbox have already weathered a few quarters of margin pressure but as management pivots the comparisons are getting better. They’re on the edge of getting their growth grooves back. When they do, we’ll be here. Until then, however, the stocks are going to stay in a lower gear.

As usual, Technology is where the extremes are. We see the fastest overall growth in the High Technology portfolio, with its concentration of companies that are following dynamic business models at a much earlier stage than today’s Silicon Valley giants. Their glory years are still ahead, and they’re moving at high speed to make it happen.

Those giants dominate our Stocks For Success list, where we’re expecting only slightly better 3Q19 results than the market as a whole . . . good enough to outperform but not a recipe for a huge rally in the next few months. And then there’s the Aggressive list, where management continues to sacrifice immediate profit in order to capture massive revenue gains while they can.

Then there are the REITs, which are all over the map because of the way Real Estate accounting works to write down property values while passing most of the tangible income back to shareholders. Our recommendations here are tracking up to 340% earnings growth and down to 60% earnings deterioration, along with the full range of results in between. Even if we factor them out as too erratic on a quarter-by-quarter basis, we’re still looking for significant growth throughout our universe.

That’s what it takes to keep BMR stocks moving in the bullish direction even if the market as a whole stalls. All in all, 13% more profit than what these companies delivered last year logically translates into 13% upside for the stocks once investors are back in a buying mood.

The stocks we’ve had throughout the last year still need to gain 10% before hitting their collective peak. Some have soared while others have a lot of ground left to make up, but on a growth-adjusted basis multiples in our universe are much more attractive than ever.

The market as a whole, on the other hand, is clinging to a 4% year-over-year gain even though earnings have declined. That’s almost entirely a factor of more relaxed rate policy. If not for the Fed, there’d be no reason for the S&P 500 to make any headway at all.

Remember, the Fed is our friend as well. Lower interest rates help BMR companies as much as they help everyone else. And the math is clear. Everything else being equal, would you rather be in stocks with historical headroom and positive growth, or those that justify near-record levels with fundamentals that look stagnant at best?

Quarter after quarter, the companies we recommend keep moving forward. We’ve seen that translate into a lot of upside already, but as the fundamentals move up, the stocks inevitably follow. The rest is simply a matter of riding out the market’s mood swings.

NOTE: In our weekly paid subscription Newsletter, we do between 5 and 7 SnapShots and also support regular Research Reports. The last three stocks we recommended are already up 5% apiece. Plus, we have the Weekly High Yield Investor, whereby we discuss the 17 stocks in our High Yield and REIT Portfolios.

And to top it all off, we send News Flashes each day during the week. Got a question about any stock on the market? We'll answer. So if your favorite stock reports earnings or there is significant news, you will hear about it here first. If you want the whole picture, join the thousands of Bull Market Report readers who are making money in the stock market and subscribe here:

www.BullMarket.com/subscription

It’s only $249 a year, and later this year we will be raising it to $499 or even $999 a year, it is just THAT valuable. But we will lock you in for life at this lower price.

Good Investing,

Todd Shaver, Founder and CEO

The Bull Market Report

Since 1998

Subscribe HERE:

www.BullMarket.com/subscription

Just $249 a year, soon to go up to $499. But you are guaranteed the SAME PRICE forever.