The Weekly Summary

The week after a market holiday is usually frenetic and this one was no exception, packing at least five days of volatility into an abbreviated calendar. Relief was the strongest note driving the S&P 500 and our stocks up close to 2%, with news that China has agreed to participate in trade negotiations in October cutting through the global clouds.

Closer to home, August job creation numbers were decent . . . a little lower than some hoped, but well within the range that usually reflects an ongoing economic expansion. We're a long way from recession territory even though corporate hiring plans remain on hold while the world waits for the trade war to resolve. In the meantime, any slippage in the job market will strengthen the Federal Reserve's argument to keep lowering interest rates in the absence of inflation.

We're less than 10 days from the next Fed meeting now. If we get the 0.25% cut most investors expect, it probably translates into roughly a 3.5% bump up for the S&P 500. Catch the market mood in the right place and that's going to take stocks back to record levels. It's hard to complain about that.

There’s always a bull market here at The Bull Market Report! Want a free trial? Let us know!

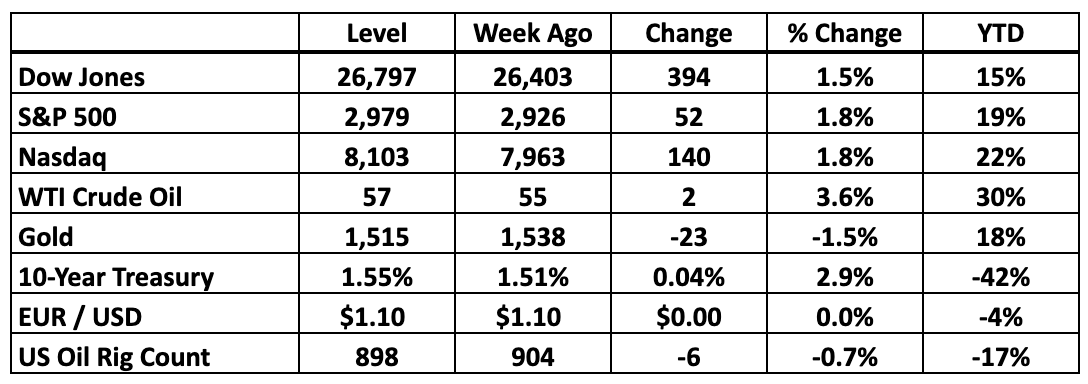

Key Market Indicators

-----------------------------------------------------------------------------

BMR Companies and Commentary

The Big Picture: The Sector Map Spins

With earnings stalled across the S&P 500 as a whole for the past nine months, most of the market activity this year is best interpreted as Wall Street’s effort to pivot to match changing investment priorities. Popular growth sectors are currently out of favor as their expansion hits a wall. And with defensive themes already looking rich, there isn’t a lot of “value” around in the traditional sense.

However, a month from now the pendulum can easily swing again, pulling cash away from today’s hot spots and pushing it back into areas of the market that don’t look attractive at all. We’ve seen it play out again and again over the year so far and will undoubtedly see the cycle continue until clear leadership emerges.

Cut through the cycle and one thing is clear. Investors fleeing declining yields in the bond market are hunting replacements for lost income, parking money in dividend-paying stocks instead of rolling it into newly issued Treasury debt. They don’t want to take on a lot of additional risk in the process, so only the safest economic havens have benefited.

Over the last 12 months, the Utilities are up 15%, which is a staggering rally for a sector that rarely moves at all. We haven’t bothered with these stocks for two reasons. First, our more growth-oriented recommendations have done much better. Second, the Utilities don’t actually pay much. Dividends across the sector only added up to 4% a year ago and now that the stocks have rallied they don’t even pay 3% a year. That’s not worth locking in.

Similar logic carries to the Consumer Staples and Real Estate sectors, both of which have rallied 13% over the last 12 months. We love Real Estate because the yields tend to be much higher and a year ago the stocks were deeply depressed. Where are the REIT bears now? We don’t hear them.

Otherwise, it’s been a dull year for the market. Technology has gained ground because that’s where the long-term growth is. Consumer Discretionary stocks have also done well because that’s where Amazon is. And Communications is all about Social Media stocks recovering from a terrible 1H18. Healthcare, Materials, Industrials, Financials and especially Energy have all suffered.

Again, this isn’t about relative growth or value. Healthcare, for example, had a huge 2Q19, with the sector as a whole reporting 9% stronger earnings than what we saw the previous year. That’s usually a catalyst to push the stocks into a rally. This time around, the group went nowhere. The Financials told a similar story.

For the long term, the Financials are also extremely attractive on a pure earnings basis. The big Banks and Insurance carriers are still growing at a healthy 5% rate, but as long as the yield curve is unsettled few investors want to go near the stocks. The sector barely commands a 13X earnings multiple now, half what we see in most other areas of the market. Energy doesn’t look much stronger. They’ll recover, but until they do, we see little point in widening our sector-weight Special Opportunities exposure to either group, no matter how “cheap” they look today. (We’re not fond of that word.)

So what does this mean? If you tried to capture growth this year on a sector level, you’ve been disappointed. Our strategy of selecting the right stocks regardless of sector has paid off a lot better. BMR recommendations have climbed 20% over the past 12 months. And while we're heavy on Technology, that sector as a whole has been no prize. Going all over the market map has given us the freedom to outperform. We're looking forward to more, even if the market as a whole keeps grinding its gears.

There’s always a bull market here at The Bull Market Report! Want a free trial? Let us know!

NOTE: In our weekly paid subscription Newsletter, we do between 5 and 7 SnapShots and also support regular Research Reports. The last three stocks we recommended are already up 5% apiece. Plus, we have the Weekly High Yield Investor, whereby we discuss the 17 stocks in our High Yield and REIT Portfolios.

And to top it all off, we send News Flashes each day during the week. Got a question about any stock on the market? We'll answer. So if your favorite stock reports earnings or there is significant news, you will hear about it here first. If you want the whole picture, join the thousands of Bull Market Report readers who are making money in the stock market and subscribe here:

www.BullMarket.com/subscription

It’s only $249 a year, and later this year we will be raising it to $499 or even $999 a year, it is just THAT valuable. But we will lock you in for life at this lower price.

Good Investing,

Todd Shaver, Founder and CEO

The Bull Market Report

Since 1998

Subscribe HERE:

www.BullMarket.com/subscription

Just $249 a year, soon to go up to $499. But you are guaranteed the SAME PRICE forever.