The Weekly Summary

Every so often, investors benefit from a simple gut check. When our stocks are going up, it's nice to verify that the gains are truly justified and there's room for more upside when the market winds blow in the right direction. And when our stocks go down, it's even more important to make sure that it's just the wind and not something fundamentally wrong with the underlying business or our calculations.

That's the kind of week it's been for us. While the S&P 500 kept climbing, the high-growth stocks that dominate our universe took a significant step back after months of outperformance. The Aggressive group dropped 9% and our High Technology portfolio fell 5%, overcoming mild strength elsewhere. Simultaneously, the recent flight to dividend stocks unwound as hints of inflation softened the Fed rate cut outlook, taking our REIT and Healthcare recommendations with it. Caught between the frying pan and the fire, the BMR universe as a whole took a step back to regroup.

We're still up 35% YTD compared to a 21% gain for the market as a whole. The High Technology group is still up a breathtaking 75% YTD. We aren't crying. With that level of outperformance, our stocks have plenty of cushion to absorb a few percentage points worth of reversal. Nonetheless, it's prompted a lot of rechecking throughout our portfolios. You're seeing the first results of that new round of analysis here. So far, we see no reason to change course.

But it's worth reflecting a bit on the change in the market weather. Almost exactly a year ago, warnings from Big Tech companies like Apple and Amazon triggered what eventually became a full-fledged 20% market slide. It took a full 12 months for the S&P 500 to recover its record-breaking nerve and get back to the age-old job of conquering new peaks.

Of course back then interest rates were moving up instead of down. Otherwise, the only thing that's really changed is that investors have now tolerated a full year of volatility, twisted Treasury yields, trade war and flat corporate earnings. The question now is how far their patience will stretch before they need proof of better times ahead.

From what we've seen, it can stretch a long way, especially with other asset classes yielding less than what ambient inflation steals from purchasing power in a typical year. Bonds, cash and gold are safe but don't offer the upside that stocks, despite their risk, offer in the long term. And as a result, we suspect we'll see money keep coming in from the sidelines to keep the stock rally alive, even if it's on a stop-and-start basis until positive catalysts emerge.

The Fed has become one of those catalysts. The next rate policy meeting ends on Wednesday and we're expecting at least a 0.25% cut. From there, we aren't ruling anything out. Odds are good Jay Powell and his fellow central bankers are in a similar position. They're watching the economy and the market. If it looks like the mood needs a little support, they're in a place where they can provide it.

We may need that support in the coming week if Saudi oil distribution remains shut down for long. Drone attacks on a key field have taken 5.7 million barrels a day out of the global supply chain, reducing the amount of petroleum available by 5% . . . roughly what Iran and Iraq pump together. Oil futures are soaring. We're pleased that we've remained bullish on [SUBSCRIBERS ONLY] for moments like this. Whatever happens, that fund should be a ray of light until the market mood improves.

There’s always a bull market here at The Bull Market Report! Want a free trial? Let us know! Let's get to work. It's going to be an interesting week.

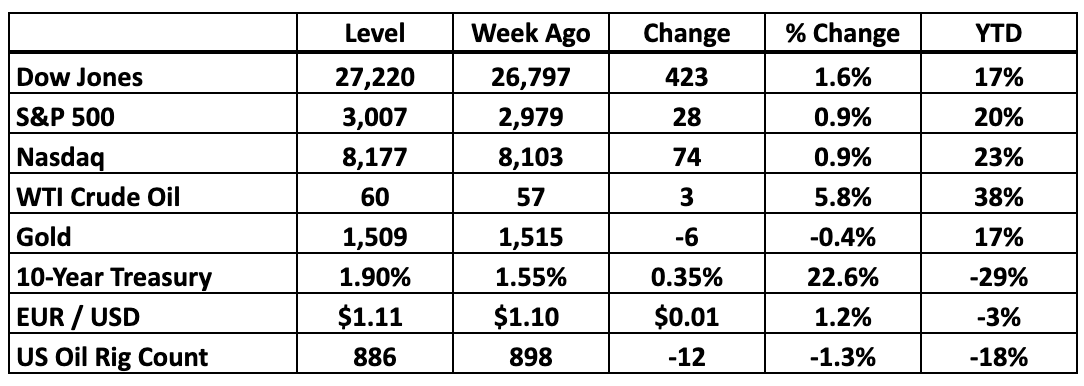

Key Market Indicators

-----------------------------------------------------------------------------

BMR Companies and Commentary

The Big Picture: Short Sellers Take Cover

We discussed the market’s strategic gyrations in recent morning News Flashes but want to highlight a few of the most specific swings in sentiment around the stocks we recommend. After all, when money reverses direction for no clear reason, investors need to look deeper to determine whether the core proposition has shifted or just the market weather.

Only five BMR companies missed our earnings target last quarter. They’re up an average of 5% since releasing their numbers, so clearly there’s no direct correlation between fundamental disappointment and the direction stocks move in response. In fact, the BMR stocks that beat our forecasts actually dropped a little this season in line with the market as a whole.

Likewise, hitting the mark on revenue made no real difference in terms of the direction our stocks have moved this season. And in most cases, guidance for the coming quarterly confession cycle has held up better than usual. Strong stocks are getting stronger, but the highest flyers spent the last month under a cloud all the same.

Part of the pressure on these companies is pure macroeconomic dread. The recession narrative exploded last month as hedge fund algorithms interpreted the inverting yield curve as an automatic contraction signal, triggering liquidation of speculative positions as portfolio managers shifted into more secure postures. Suddenly growth fell from favor, taking many BMR stocks along with it.

A look at [SUBSCRIBERS ONLY] reveals what’s going on here. The growth outlook for this company has not changed and unless you assume that the global economy is going over a cliff, management is still on track to turn what we suspect will be 35% revenue growth next year into at least 65% earnings expansion. None of the dozen big Wall Street banks that track the stock have concluded that growth profile has flattened out one bit. If anything, they still tell their clients this stock is worth at least $140.

And yet that math no longer stretches the way it did a week ago when this was indeed a $145 stock. What’s changed is investors’ comfort with paying up to 190X earnings or 19X revenue for a company growing this fast. Again, cash flow shows no sign of deterioration but after the recent selloff this and similar stocks have cooled down dramatically from the “price” end of the price-per-earnings or price-per-sales calculations.

We see this as just another turn in the market weather. When the sentimental pendulum swings back, this company can command at least $145 again and investors who buy the dip will be happy. But in the meantime, BMR subscribers have done extremely well here, so even if this correction continues for weeks or even months, there’s little reason to complain. This was a $58 stock when we added it to our Buy List back in November. It’s still up nearly 90% this year alone.

For now, however, the short sellers will remain in control until they realize they’ve run out of rope. Short interest here has climbed to 11% of the stock, which means that sooner or later those investors need to commit $735 million to cover their positions and take their money. If they can’t do it gradually, they’ll need to do it fast, which raises the prospect of a squeeze if the stock starts moving up this week.

Quite a few of our recommendations are in a similar situation right now. We’d point to aggressive growth stories that have faced fierce headwinds after reporting perfectly reasonable 2Q19 numbers. It’s no coincidence that short sellers have committed to buy 9-11% of each stock, so there’s no reason for us to liquidate our positions here and make their victory any easier.

And then there’s [SUBSCRIBERS ONLY], where short interest has swelled to a huge and unsustainable 15% of the overall company. Institutional investors own 15% of the stock so even small positions like ours can make a difference in whether the shorts get what they need. If we hold on, we’ll see more sudden moves to the upside to balance the pain we’ve absorbed recently . . . and then the stocks will get back to work.

After all, these six stocks are still up an average of 30% YTD, beating the S&P 500 by 10 percentage points. We're the ones in a position of strength, and judging from the wild rebound [SUBSCRIBERS ONLY] launched last week, the short sellers should be the ones who are nervous. If you've been looking for a chance to expand your holdings of any of these stocks, now is the time. Remember, if the fundamental picture changes, we'll tell you. And unless that picture changes, it's just the wind blowing against extremely constructive cash flow trends.

NOTE: In our weekly paid subscription Newsletter, we do between 5 and 7 SnapShots and also support regular Research Reports. The last three stocks we recommended are already up 5% apiece. Plus, we have the Weekly High Yield Investor, whereby we discuss the 17 stocks in our High Yield and REIT Portfolios.

And to top it all off, we send News Flashes each day during the week. Got a question about any stock on the market? We'll answer. So if your favorite stock reports earnings or there is significant news, you will hear about it here first. If you want the whole picture, join the thousands of Bull Market Report readers who are making money in the stock market and subscribe here:

www.BullMarket.com/subscription

It’s only $249 a year, and later this year we will be raising it to $499 or even $999 a year, it is just THAT valuable. But we will lock you in for life at this lower price.

Good Investing,

Todd Shaver, Founder and CEO

The Bull Market Report

Since 1998

Subscribe HERE:

www.BullMarket.com/subscription

Just $249 a year, soon to go up to $499. But you are guaranteed the SAME PRICE forever.