The Weekly Summary

Rotation worked against us early this month but now the inevitable market pendulum swings back in our favor. BMR stocks rebounded nearly 1% last week, led by a stunning 6% surge in the Aggressive portfolio. Evidently these companies weren't as "toxic" as some people on Wall Street wanted us to believe. Those who sold the dip are regretting their lack of conviction now. Those who bought, on the other hand, are already making money.

That's what it's all about. While a few of our highest-flying recommendations remain a magnet for opportunistic negativity from analysts looking to make a name for themselves, it's hard to get too worried when we've watched this game play out many times in the past. A stock that climbs 300% can afford to give up a lot of that ground in a very short period of time . . . and longer-term shareholders will barely even flinch.

With the BMR universe once again up 60% in the aggregate, we're not quite in flinch-free mode yet, but we acknowledge that volatility cuts both ways. Stocks that fly tend to fall fast. As long as they fly more than they fall, we simply keep our eyes on what ultimately matters: performance. That's part of what this week's Big Picture is about. Our recommendations aren't just up 60% in their time with us (compared to roughly a 12% time-adjusted return for the S&P 500). They're up 13% over the trailing 12 months . . . a period where the market as a whole stalled.

Right now our stocks are still in correction territory while the S&P 500 is back around record levels. When rotation finishes playing out and BMR stocks catch up to where the broad market is now, this is the kind of environment where alert subscribers can boost their lifetime scores quite a bit.

And then there's the Fed. As recent News Flashes discussed, we got that 0.25% rate cut after all. Jay Powell didn't have any surprises up his sleeve and said as much in the press conference. He's watching the same data points we are. When they stack up to a rate hike, we'll know. Otherwise, it looks like interest rates will decline as long as inflation remains below 2%. We like that a lot. It pulls money out of Treasury bonds into higher-yield investments like the ones on our portfolios. And it supports the economy, feeding growth and giving our more dynamic stocks plenty of room to move.

People can try to find a negative long-term spin there, but once again, it's hard to argue coherently that this is anything but good news in the short term. Meanwhile, the trade war seems to have calmed down for a few weeks. The Saudi oil production outage was a non-shock as far as the market was concerned. Earnings season is coming. Now is the time for investors to shake off months of dread and capture opportunities.

There’s always a bull market here at The Bull Market Report! Want a free trial? Let us know! Let's get to work. It's going to be an interesting week.

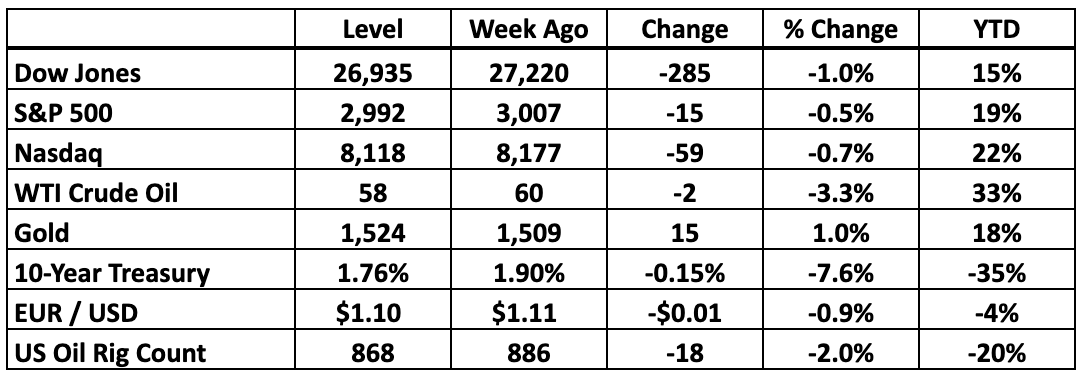

Key Market Indicators

-----------------------------------------------------------------------------

BMR Companies and Commentary

The Big Picture: Plenty Of Headroom Here

We talked a lot over the summer about the way corporate fundamentals still support further upside for the market as a whole. That math has not changed, so it’s no surprise that the S&P 500 is once again on the edge of record territory. And ironically enough, BMR stocks have even further to go before their earnings stretch logic to the limit.

The S&P 500 hit yet another record on Thursday and remains within 2% striking distance of that peak. That’s the good news. While it’s encouraging to see the market is still moving in the right direction, the gains have gotten slim when you balance the downswings against the rallies. All in all, from last year’s peak to now, index fund investors have a mediocre 3.7% to show for all the headaches along the way.

It’s not hard to understand their frustration. Money parked in one-year Treasury bills a year ago would have earned 2.6% with minimal risk, so these investors have effectively traded all those months of nerve wracking volatility for an extra 1% return on their money. Was it worth it? Another year of this will really test their patience.

However, BMR stocks have collectively rallied about 14% over the same period, so even though we’ve definitely felt the same volatility the market as a whole has had to absorb, our patience has at least earned a more significant reward. That’s the way the market is supposed to work. The secret is that the BMR universe has a lot more fundamental fire on its side.

After all, the S&P 500 has a sound reason to be roughly where it was a year ago. Back then, we were projecting forward earnings of about $173 for the index, which would have reflected close to 11% growth. Through all the angst about the yield curve and the trade war, we’re now looking at nearly $177 in S&P 500 earnings for next year, which is a little more than 10% growth.

Run all the numbers and the stocks that commanded a 17X earnings multiple then still rate the same multiple now. Almost identical fundamentals combined with an almost identical outlook justify almost identical valuations today. The only thing that’s changed is interest rates, which support another 3-4% upside for the S&P 500 every time the Fed relaxes. If that means another two rate cuts over the coming year, maybe those index fund investors will be able to look at their statements next September and cheer 12% returns over the trailing two-year period.

Our stocks will leave them in the dust. Part of what makes us so confident is the fact that while earnings for the broad market have stalled over the past year, the BMR universe kept expanding. Last quarter alone we saw 45% earnings growth across our portfolios. In the coming 3Q19 reporting cycle we’re looking for at least 10% growth to continue. That’s enough to keep stocks climbing at a healthy rate even if investors aren’t willing to embrace higher multiples.

If anything, all it takes is a shift back to historical multiples to give our stocks what they need to run a victory lap in the coming year. While the S&P 500 is now 1% below its peak, very few BMR recommendations are that close to straining their known limits. The exceptions are on the defensive side. Several of our REITs are only one good day from climbing to fresh peaks, and our High Yield portfolio is likewise within range of its best levels of the year.

But most BMR stocks are still a long way from their peaks. We estimate that even if they only revert to their recent highs our subscribers can add an easy 15% to the current score. That gives us plenty of headroom. Factoring in the Fed’s trajectory raises the ceiling from there.

Of course high multiples can always get compressed if investors lose their appetite for dramatic growth stories. That’s the case with a few of BMR stocks that dropped fast over the summer. [SUBSCRIBERS ONLY] supported an aggressive but justified 106X earnings multiple before its 2Q19 report. With revenue projections as strong as ever and the bottom line rising a little faster than expected, the company’s valuation has dropped to 76X earnings.

That’s extremely close to the 71X lower limit reached at the depths of last year’s correction. Unless the market has permanently abandoned the principle of paying more for faster growth, there’s no reason to suspect the stock will be stuck here long . . . especially with the Fed on the move. A year ago, interest rates were higher and the stock commanded a 125X multiple.

[SUBSCRIBERS ONLY] is a similar story. The people arguing so passionately that the stock is only worth $60 today think the stock is only worth 7X sales. We’ve seen that multiple swing from a 3X low back in December to as high as 18X a few weeks ago. The extreme might be too high to sustain, but it’s clearly within the realm of reason to see at least test that level again on the right turn of the market tide.

Meanwhile, every quarter beyond breakeven gives us a sense of how much the market will pay for every penny this company earns. The math naturally improves when you’re profitable. We suspect previous valuations are far from the ultimate limit here.

We could give you similar comparisons for our other high-growth recommendations, but relatively mature companies like [SUBSCRIBERS ONLY] provide the most compelling demonstration of all. When this was a $120 stock early in the summer, the market was willing to pay 40X earnings for a taste. Here at a 33X multiple, it’s like the clock wound back to February. And people who bought this stock in February are up 10% since then.

Stock after stock, the lesson is clear. As long as the fundamentals are progressing in line with expectations, any significant selling is a buy signal. Sooner or later, the market mood will swing and reflate the multiples to at least what we've seen in the past. We aren't assuming anything more aggressive than that to fuel continued outperformance.

NOTE: In our weekly paid subscription Newsletter, we do between 5 and 7 SnapShots and also support regular Research Reports. The last three stocks we recommended are already up 5% apiece. Plus, we have the Weekly High Yield Investor, whereby we discuss the 17 stocks in our High Yield and REIT Portfolios.

And to top it all off, we send News Flashes each day during the week. Got a question about any stock on the market? We'll answer. So if your favorite stock reports earnings or there is significant news, you will hear about it here first. If you want the whole picture, join the thousands of Bull Market Report readers who are making money in the stock market and subscribe here:

www.BullMarket.com/subscription

It’s only $249 a year, and later this year we will be raising it to $499 or even $999 a year, it is just THAT valuable. But we will lock you in for life at this lower price.

Good Investing,

Todd Shaver, Founder and CEO

The Bull Market Report

Since 1998

Subscribe HERE:

www.BullMarket.com/subscription

Just $249 a year, soon to go up to $499. But you are guaranteed the SAME PRICE forever.