The Weekly Summary

We talked about "rotation" throughout September. Last week the circular forces of market sentiment gave us a big win, with our Aggressive portfolio surging 5% and our High Technology recommendations adding another 4% to that score. As a result, the BMR universe as a whole made some nice progress while the S&P 500 dropped 1%. Any week where you keep making money in the face of a broad market decline is a good one.

We have a track record of outperformance to maintain. Thanks to this week, our YTD is once again close to double what the S&P 500 has produced. BMR stocks are up 33% compared to 18% in the broad market. Looking toward the final quarter of a bumpy year, we're excited to see how much farther we can extend that lead over the next three months, no matter whether Wall Street pivots up or down.

All the twists in last week's market mood played out in our daily News Flashes. If you didn't get those, you're not a subscriber. Want a free trial? Let us know!

If the bulls are back in charge, our stocks have more room to run before straining historical limits. Despite the volatility of the last few weeks, the S&P 500 is only 2% from its record peak. The BMR universe, on the other hand, has already absorbed a full correction without losing their aplomb or endangering their YTD gains, so we don't need to break any records to keep this rally going.

Either way, we have a strong defense to go with our high-scoring recommendations. As the coming earnings season evolves, the end of 2019 could play out like what we saw last year or finally give investors a reward for their long-term perseverance. A year ago, Wall Street was on the verge of a serious correction. Having already stomached a lot of that downside this time around, we see no reason our outperformance can't continue no matter where the S&P 500 twists.

That twist may go down. While Friday revealed that the job market is pensive enough to justify at least one more interest rate cut, the trade war, stalled earnings, and indifferent economic data keep many investors on edge. The Fed now has a tight needle to thread. If rates go down because a strong economy isn't generating inflation, Wall Street will cheer. However, every hint of a recession ahead will feed the negativity that is already holding some of our favorite stocks back.

We'd rather live in a boom and swallow the occasional rate hike than watch the Fed struggle to keep the economy from stalling. But until corporate earnings demonstrate that the boom is back, investors will vacillate and stocks will spin. The good news is that the next quarterly earnings cycle starts on October 15 with the big Banks. Once the season gets underway, we'll know a lot more about how the year will end.

There’s always a bull market here at The Bull Market Report! Want a free trial? Let us know! Let's get to work. It's going to be an interesting week.

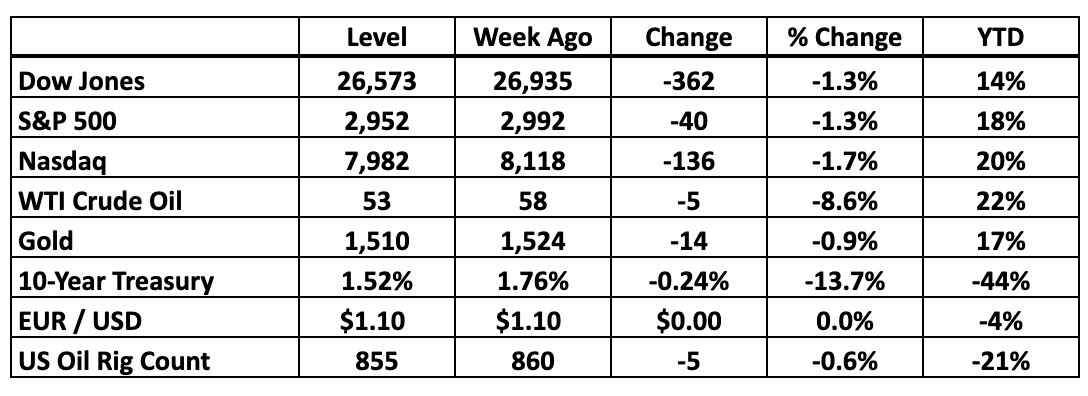

Key Market Indicators

-----------------------------------------------------------------------------

BMR Companies and Commentary

The Big Picture: The Dogs Of Fear Aren't Barking

After another week of yield-paying sectors smashing all-time records while the high-tech heart of Wall Street remains depressed, other investors are starting to hum the refrain we started singing last week. Money is flowing into Utilities, Real Estate and Consumer Staples at the fastest rate in years, stretching normal valuations and leaving more dynamic areas of the market gasping.

In our view this is less about a true flight to safety and more about investors around the world reaching for better income than what they can get in the Treasury market or in overseas bonds that pay negative interest. That’s an important distinction. No matter what you hear, we aren’t facing a lot of fear right now. We’re dealing with a species of greed.

Risk tolerances haven’t collapsed. Bond yields around the world have. And as money inches out of bonds in search of reasonable returns, yields in the stock market follow bond rates lower.

We’ve talked last week about the premium risk-averse investors are paying for relief from recession anxiety without having to accept the negative inflation-adjusted income they’d get from Treasury bonds. If prices are climbing 1.7% a year and the Fed won’t raise rates before inflation hits 2%, buying middle-term government debt will leave you with less purchasing power when those bonds mature than what you have now.

That’s only an acceptable strategy if you’ve abandoned hope for anything in the global markets doing better than breaking even. We’re naturally on the side of doing better. So are like most realistic investors who recognize that the world is a long way from the point where locking the doors against absolute disaster is the only move that makes sense.

However, some moves only make sense because every other option has a worse outcome. That’s where we think Utilities and Consumer Staples stocks are now. They’re not objectively bad as places to park cash ahead of an economic storm. But when you see better alternatives as we do, these sectors look bloated and on their way to outright bubble territory.

Utilities, for example, usually command a slight premium because their dividends are about as reliable as it gets, and people will pay extra for that kind of clarity. However, that premium has expanded a lot in the last few months. Three months ago, these stocks were available for 19.1X earnings against an 18.4X multiple for the S&P 500 as a whole. As of last week, the S&P 500 valuation hasn’t changed while Utilities are at the point where they cost 20.9X earnings to buy in.

Admittedly, Utilities still pay a 1% higher dividend yield than the S&P 500, but when you’re weighing whether to lock in 2.8% or 1.8% (before factoring in inflation) nobody is reaping huge windfalls here. That’s why we tend to skip the sector in order to focus on Real Estate, where yields remain higher, especially on the specific stocks we recommend.

But the real arbiter of value in a defensive portfolio is the amount of extra income investors can squeeze out of the stocks they pick while their money is parked. With Treasury debt, the rate you lock in is the interest you’ll receive. The odds of a default are as close to zero as it gets. Everywhere else, you’re accepting a little risk that a company will run out of cash and cut its dividend or skip a payment.

The higher the spread, the greater the perceived risk. Treasury rates have reached 1.35% so the bottom of the risk/return curve is almost as low as it gets right now. Five-year bonds bottomed out at 1.26% at the end of 2008, when it really looked like Wall Street’s world was ending and overnight lending rates were effectively zero. Back then, Utilities paid 4.2% to reflect the elevated risk that these companies would fail to meet their shareholder obligations. The spread naturally rose to roughly 3 percentage points. A lot of people were scared.

What happened, of course, is that the sector didn’t even blink. It would take a disaster greater than 2008 to interrupt the income investors receive here. And because the spread between Utilities and Treasury yields has narrowed to 1.5 percentage points (half what it was in 2008), the bond market is signaling that default risk has receded a lot over the past decade.

Likewise, we can track the spread between “defensive” yields and what investors get from the S&P 500 as a whole. Normally we expect Utilities to pay 2.4% more than the broad market. The spread is now barely 1 percentage point wide now. There just isn’t a lot of room left there for more money to crowd into the sector before the risk curve breaks. Back in 2008, for example, the yield spread between Utilities and the S&P 500 narrowed to barely 1.2 percentage point. We’re close to that historical limit now.

We’re lingering on this math to give you a better sense of how the current rush to defense is distorted in any reasonable historical context. If the world right now feels like it did at the end of 2008, then locking in these abnormally low yields and compressed risk spreads makes sense as the best way to sidestep any significant economic threat. Otherwise, the math doesn’t add up. The usual statistical indicators that accompany real fear in the market simply aren’t there.

To borrow a line from the Sherlock Holmes stories, the dog isn’t barking. Maybe there’s no dog.

And in that scenario, money will soon flow back out of overcrowded yield stocks into what are now underrated areas of the market. Our High Technology and Aggressive portfolios are already rebounding and unlike a lot of defensive stocks, have a lot of room to continue their rally. We know how high these companies can go when Wall Street is in an optimistic mood and as fast as their fundamentals are expanding, the ceiling keeps rising.

After all, the thing about locking in a yield is that you’re also locking out a lot of upside. We’re willing to do it with Real Estate and Big Pharma because those companies are dynamic enough to generate additional cash from year to year. That cash then feeds into additional dividends or gives investors a reason to buy the stocks at ever-higher levels. In our view, they’re in the sweet spot between a strong defense and enough offense to stay open to ambient economic growth.

However, locking in less than 3% elsewhere in the market right now locks out a lot of upside. How high can Utilities go, for example, when earnings in the sector are inching up 2% a year? If the stocks rally much faster than that, already-stretched valuations get even more extreme until finally there just isn’t any justification to keep buying.

The market as a whole, meanwhile, tends to beat Utilities by at least 2 percentage points a year. Our stocks do even better. The slow years aren’t great but the fast years more than make up for them, while our own high yield recommendations provide a cushion to encourage patience through the rough spots in the economic cycle.

Knowing that a portion of our universe is paying 5% (the REIT portfolio) to 7% (the High Yield recommendations) gives us that cushion and that patience.

NOTE: In our weekly paid subscription Newsletter, we do between 5 and 7 SnapShots and also support regular Research Reports. The last three stocks we recommended are already up 5% apiece. Plus, we have the Weekly High Yield Investor, whereby we discuss the 17 stocks in our High Yield and REIT Portfolios.

And to top it all off, we send News Flashes each day during the week. Got a question about any stock on the market? We'll answer. So if your favorite stock reports earnings or there is significant news, you will hear about it here first. If you want the whole picture, join the thousands of Bull Market Report readers who are making money in the stock market and subscribe here:

www.BullMarket.com/subscription

It’s only $249 a year, and later this year we will be raising it to $499 or even $999 a year, it is just THAT valuable. But we will lock you in for life at this lower price.

Good Investing,

Todd Shaver, Founder and CEO

The Bull Market Report

Since 1998

Subscribe HERE:

www.BullMarket.com/subscription

Just $249 a year, soon to go up to $499. But you are guaranteed the SAME PRICE forever.