Meta Platforms (META: $301), the company behind Facebook, WhatsApp, and Instagram, released its third quarter results last week. It posted $34.1 billion in revenues, UP 23% YOY, compared to $27.7 billion, with a profit of $11.6 billion, or $4.39 per share, up by a mammoth 164%, compared to $4.4 billion, or $1.64, with a beat on consensus estimates for the coming quarter on the top and bottom lines.

Other key figures and metrics were just as exemplary, with daily active users across its family of apps at 3.14 billion, and monthly active users nearing 4 billion, both up by 7% YoY. Ad impressions across its platforms increased by 31% YoY, making up for the 6% decline in the average price of its ad inventory. All in all, this was a BLOCKBUSTER of a quarter for the company.

The company is fighting some growing legal, regulatory, and reputational risks. To start with, attorney generals from across the country have filed lawsuits against Meta for its addictive features, and 33 US states are now suing the tech giant for collecting data from young users without parental consent. Meta has always been mired with legal issues, ranging from antitrust to Congressional Hearings pertaining to political advertising and targeting. Time and time again, it has managed to rise above it all, with often nothing more than a slap on the wrist. So, we see no reason why it would be any different this time around, making this muted reaction nothing more than a minor overreaction.

In other news, the company is going all-out in pursuit of the Metaverse, now in partnership with Ray-Ban, and more realistic visuals. This is infinitely better than the earlier version, where people in the Metaverse resembled Sims characters. The new Metaverse looks ready to take on the likes of Zoom and Microsoft Teams when it comes to communications, making it an absolute game changer.

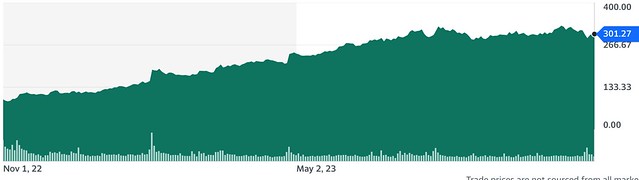

Following extensive cost-cutting measures, which involved laying off 24% of its workforce, Meta is now a lean, mean fighting machine. The stock is up by a stellar 140% YTD, and still remains off by about 22% from its all-time high of $384 set in 2021. The company is a cash machine, which helps support its generous $3.7 billion in repurchases, further aided by its $61 billion in cash reserves, $37 billion in debt, and $66 billion in cash flow. Our Target is $350 and we would never sell Meta Platforms. If revenues and earnings continue at this pace in the 4th quarter, and given a solid stock market, we can see that we might have a problem with the Target. We’d just have to raise it to $425.