The valuation of automaker Tesla (TSLA: $252) has long been an enigma for Wall Street and the company continues to astound and astonish analysts to this day. The stock was considered overvalued when it first went public in 2010, with a valuation of $2.2 billion, just as it is today with a market cap of $760 billion. And in the preceding years, many short-sellers have lost fortunes trying to bet against the company. We have a personal friend, a former Merrill Lynch VP who ran an office in Florida, who has been short for the last four years. He has lost over seven figures. We have implored him to buy back the stock, especially when it went to $102 in January of this year, down from the all-time high of close to $400 set in late 2021.

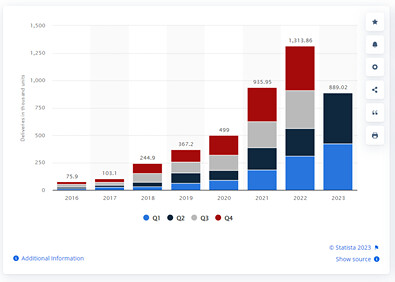

To be fair, it's hard not to question the exuberant valuations that the automaker has consistently held, which is 16 times the market cap of Ford Motors, a 120-year-old behemoth that sells twice as many cars as Tesla, and three times that of Toyota, which currently sells 10 times as many cars. Even considering Elon Musk’s ambitious goal of making 20 million cars a year by 2030, the valuations are a tough sell, particularly in the face of rising competition. The company is on track to deliver 2 million this year, up from 935,000 two years ago.

Number of Tesla vehicles delivered worldwide

Tesla has remained the most popular stock among retail investors for years. While it is also the most shorted stock as of now, with over $21 billion in short interest, the fate of these shorts looks increasingly shaky, similar to the many institutional, retail, and hedge fund bets made against the stock over the past decade. And as you know quite well by now since we have mentioned this numerous times, having a large short position is very bullish. Why? Because the only thing shorts can do is to BUY BACK their stock, which pushed the stock higher.

As discussed in our research report when we first began covering the stock two months ago, Tesla is not an automotive company, and it would be a mistake to value it as such. With its ambitious plans to flood the streets with robotaxis, its Dojo supercomputer that the Street estimates to be worth over $500 billion, the massive battery factory in Nevada, and innumerable other innovations, rather than an “automotive” company, this is a high-growth tech company through and through.

Reuters said this eight days ago: “Tesla has drawn up plans to make and sell battery storage systems in India and submitted a proposal to officials seeking incentives to build a factory, as Elon Musk continues a push to enter the country. Tesla has been in talks about setting up a new electric vehicle factory in India to build a [world] car priced around $24,000 for weeks, with discussions overseen directly by Prime Minister Narendra Modi.” We have heard that Tesla has plans for another large battery plant as well.

Another overlooked asset is the company’s extensive network of 45,000 superchargers, which it has yet to monetize. Most competitors have adopted Tesla’s North American Charging Standard. Rising competition and growing penetration of EVs on American roads only stand to benefit Tesla going forward.

Tesla is not just an automobile manufacturer; it is the future of mobility, computer vision, and sustainable technology, all rolled into one. Its vision-based AI system has applications beyond mobility, similar to its growing prowess in battery technology. With robust tailwinds across the board, and a well-capitalized balance sheet with $23 billion in cash, just $6 billion in debt, and $14 billion in cash flow, we believe that this company, with a market cap of $800 billion, run by an acknowledged genius, is poised to continue to change the world as we know it. Our Target is $325.

If you are still not convinced, get the new book called Elon Musk, by Walter Isaacson. We read all 615 pages in three days this week. He is changing the world that we live in.